Weekly Market Outlook - Stocks Start the New Year at a Disadvantage

If anything, last week was supposed to be bullish... the Santa Claus rally. Santa only left coal in traders' stockings this time around, though, sending the S&P 500 1.1% lower for the shortened trading week. Perhaps worse, in the process of doling out the pullback, the S&P 500 fell under a couple of crucial support lines, meaning stocks will start the week out at a disadvantage.

If anything, last week was supposed to be bullish... the Santa Claus rally. Santa only left coal in traders' stockings this time around, though, sending the S&P 500 1.1% lower for the shortened trading week. Perhaps worse, in the process of doling out the pullback, the S&P 500 fell under a couple of crucial support lines, meaning stocks will start the week out at a disadvantage.

Then again, with a new year representing a clean slate, there's no real certainty as to what sort of mode investors will be in as 2017 gets going.

We'll weigh the pros and cons after taking a look at last week's and this week's major economic announcements. There are some pretty big ones in the queue, with the grand finale being last month's unemployment report on Friday.

Economic Data

There wasn't a whole lot on the economic dance card for last week, but a couple of items are worth a closer look.

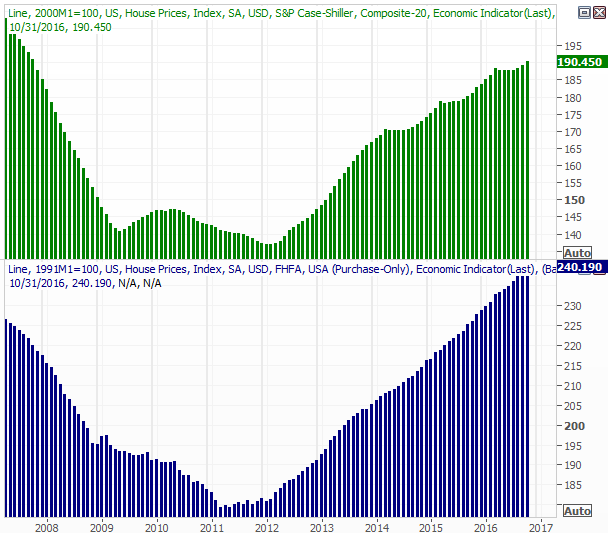

One of those items is the Case-Shiller 20-city Index (of home prices). Though the data released was only October's -- and much has happened in the meantime -- we continue to see progress on this front. The Case-Shiller Index jibes with the FHFA Housing Price Index, which also shows ongoing improvement in the housing market.

Case-Shiller 20-City Index and FHFA Home Price Index Charts

Source: Thomson Reuters

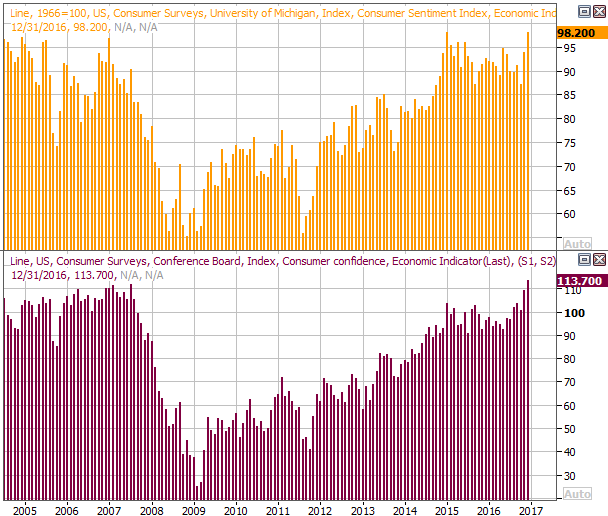

The only other data nugget from last week worth a closer look is consumer confidence. The Conference Board's key measure of consumer sentiment surged to a multi-year high of 113.7. Though a bit overstated, it's clear that consumers (and therefore investors) are more than optimistic enough to keep bullish pressure on stocks.

Consumer Sentiment Charts

Source: Thomson Reuters

Granted, consumer confidence is as much the result of bullishness as it is the cause of it, but to the extent sentiment drives the market, this is a good LONG-term indication.

Everything else is on the grid.

Economic Calendar

Source: Briefing.com

This week is going to be significantly busier.

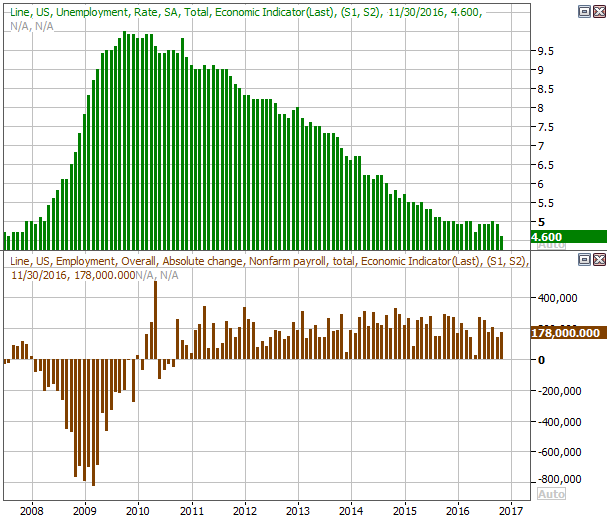

The big announcement, of course, is going to be Friday's jobs report for December. The pros are looking for 175,000 new payrolls, more or less in line with November's growth. But, with as many people who are newly joining the work force (or re-joining it), those same economists are also looking for the unemployment rate to edge back up a bit, from 4.6% to 4.7%.

Job Growth, Unemployment Rate Charts

Source: Thomson Reuters

Keep an eye on Thursday's Challenger planned job cuts report for a preview of what's apt to come in Friday's official employment report from the Department of Labor.

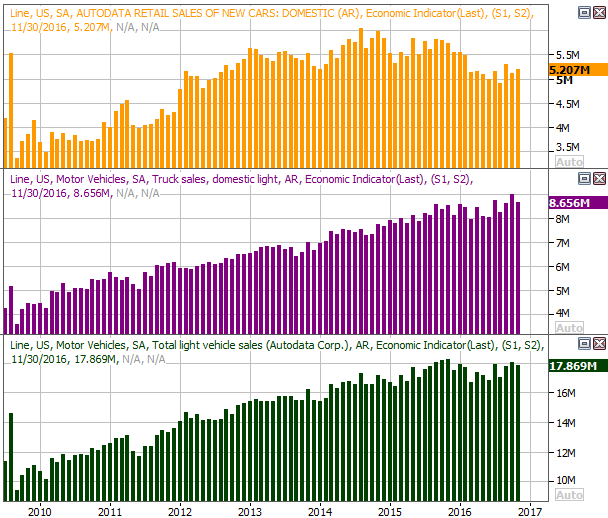

The other news that could really move the market this week is December's auto sales, due on Wednesday.

November's report was outstanding, but that's not unusual -- November's car sales are usually stronger than trend. A good report for December could go miles in quelling "peak auto" concerns, while a poor December report will renew those concerns... and potentially pose problems for automaker stocks.

Auto Sales Charts

Source: Thomson Reuters

Index Analysis

It's too soon to assume the worst. Indeed, even if this week gets started on the same bearish foot it finished last week on, there are still a handful of ways to bring a quick end to any weakness. On the flipside, considering last week was "supposed to be" bullish (and clearly wasn't), perhaps we've started the correction we know we have to face sooner or later.

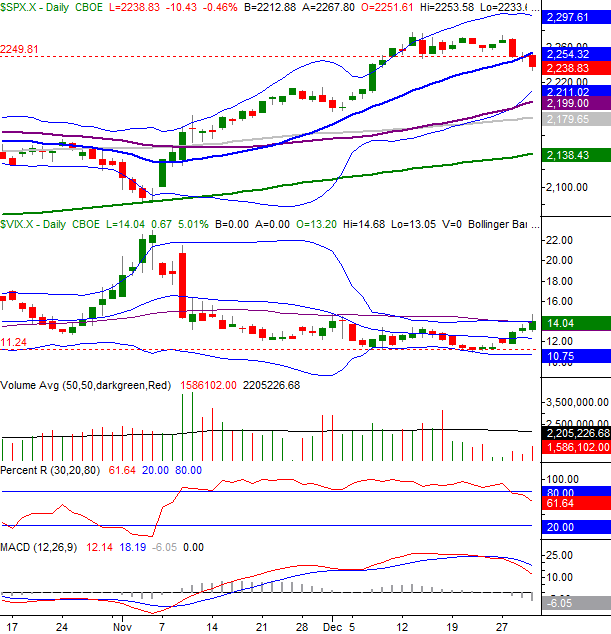

The daily chart of the S&P 500 isn't a tough one to interpret. The index not only broke under its 20-day moving average line at 2254 for the first time since early November, it broke under what was a minor (but developing) floor at 2249. The VIX is also on the move -- higher -- though it's yet to hurdle a pretty significant ceiling at the 14.0 area.

S&P 500 Daily Chart

Chart created with TradeStation

This could be little more than the market's natural ebb and flow. If it's nothing more than that, then no big deal. And, the fact that the PercentR line has finally pulled back under the 80 level confirms the tailwind is now gone. On the other hand...

The market won't be too far gone to salvage until the S&P 500 breaks below the 50-day moving average line (purple) currently at 2199 AND the PercentR line gets AND STAYS below 20. The VIX will need to be firmly moving higher at that time too. It's not happened yet, but when we zoom out to a weekly chart of the S&P 500 we can see how due -- and perhaps overdue -- for a more serious correction. Take a look.

S&P 500 Weekly Chart

Chart created with TradeStation

Four weeks ago we pointed out how the S&P 500, at the time, had just poked above its upper 26-week Bollinger band for the first time in years. It was a big deal simply because it was a clear (and rarely seen) indication that the market had traveled too far, too fast. Specifically, the S&P 500 had rallied from a low of 1811 in February of last year to a high of 2277 last month... a 25.7% rally in just eleven months, which is too much for any bull market that's as old as this one. Now we can see - visually - just how big of a move that was, and how the market has started to struggle with the sheer weight of the big move.

With all of that being said, perhaps the biggest red flag on the weekly chart is the fact that the VIX hasn't surged. Normally a stumble like last week's would prod the VIX considerably higher and set up a peak in fear... a peak that quickly sets up a market bottom. Not this time though. This time, the VIX remains very near an absolute floor, which leaves plenty of room for it to rise from here, which in turn leaves plenty of room for the S&P 500 to move lower. The S&P 500 won't hit a true bottom line until the VIX moves back to the 26 area. The S&P 500 could revisit the 200-day moving average line (green) or even the lower Bollinger band (blue) currently at 2094 before it's all said and done. Just note that both of those lines are moving fast.

Of course, the move to a new calendar year throws wrench into the "read" of any chart. We still have to be prepared for all possibilities this week, even if the path of least resistance is to the downside.