All in all, the November jobs report was better than it seemed to be on the surface. While job creation came up short of expectations, that may be more a function on not enough qualified candidates rather than not enough jobs. And, wage growth was firmer than implied when looking at the data from the less-touted (but arguably more meaningful) vantage point.

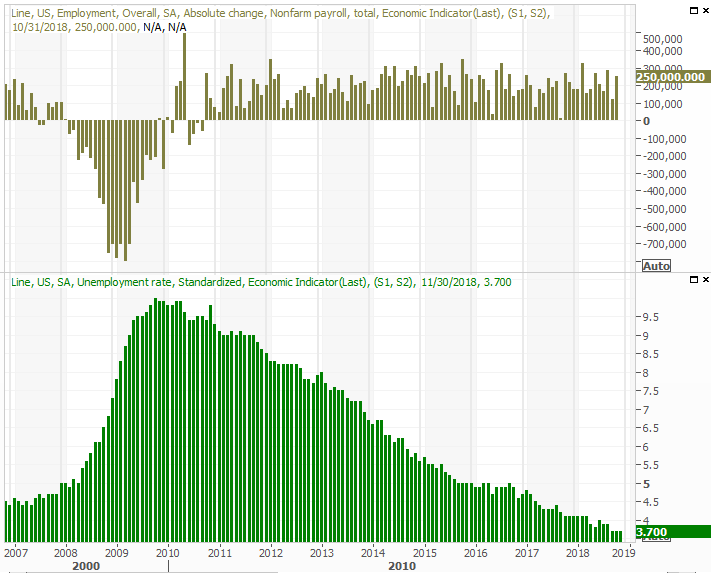

Last month, the U.S. added 155,000 new jobs versus expectations of 190,000. That's the second lowest payroll growth figure in a year, with September's 119,000 being the lowest, and certainly not enough progress to move the needle on the unemployment rate, which still stands at 3.7%. But, the United States is at or near maximum employment as-is. It's going to be difficult to make progress on these fronts. [The graphic below only shows job growth through October, which rolled in at 250,000.]

Far more telling - as has been the case for a while - is the data on other fronts, most of which shows the quality of jobs (as measured by pay) and the number of people re-joining the workforce is improving.

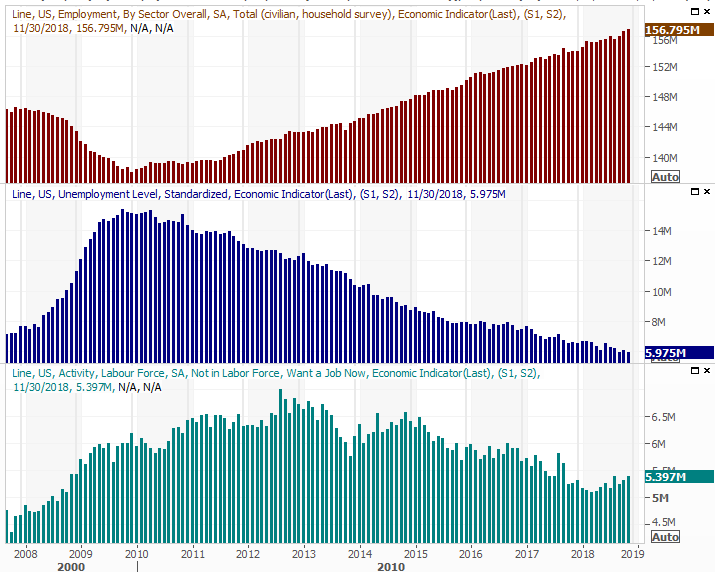

As of the end of the month, 156.8 million people in the U.S. held jobs... another record-breaking. Conversely, the number of officially unemployed people fell to a multi-year low of 6.0 million. Unemployed people without jobs but looking for a job grew again, reaching 5.4 million to extend an uptrend since early 2018. Take that last data nugget with a grain of salt, however. It's easy to say you're in search of a job, even when you truly aren't.

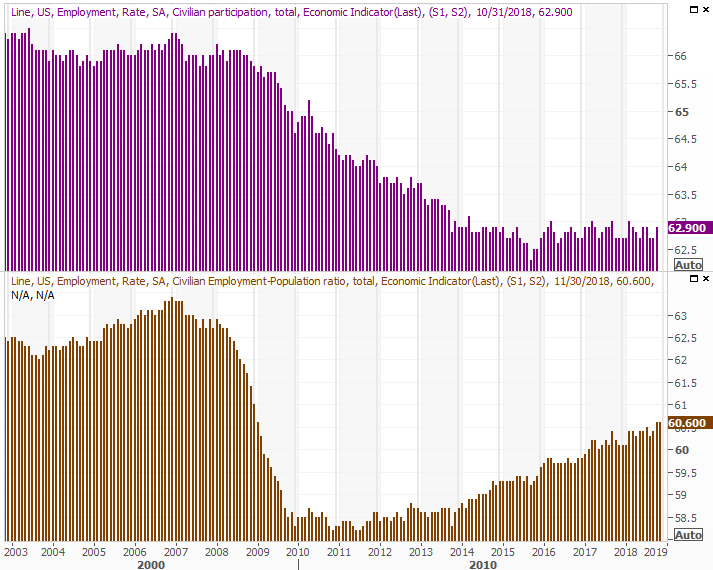

The employment/population ratio held steady at 60.6%, also extending a growth trend in place since 2012. It's still well below 2006's peak levels, but in the shadow of baby boomers' en-masse retirements, it may never reach that level again. The labor force participation rate remains just below 63%, and suspiciously isn't rising. It arguably should be. [The labor force participation rate on the graphic below is only updated through October.]

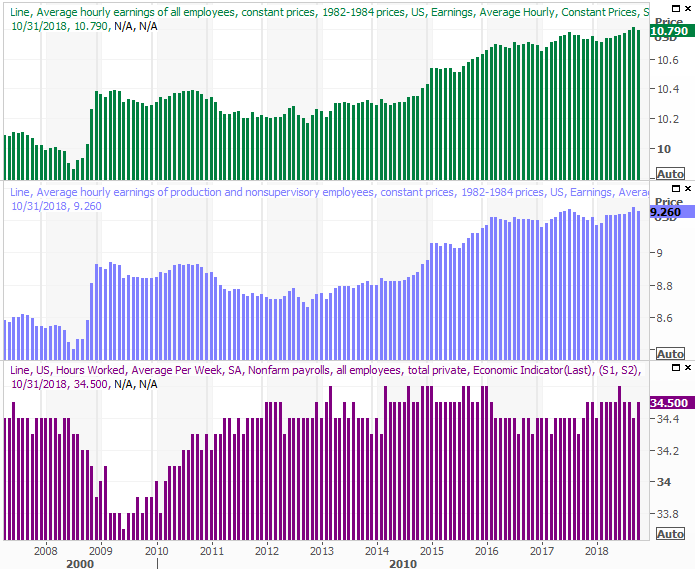

Finally, hourly wages were up 3.1%, as widely expected.

That's a year-over-year improvement, to be clear. The month-to-month improvement of only 0.2% was billed as a disappointment, but that's actually a pretty solid uptick for one month. More important, although choppy, hourly earnings have been trending higher since late-2016. [The hourly wage data plotted on the image below is only current through October.]

It could be better, though not significantly better - this is about as good as it gets. It doesn't feel good because the rates of progress aren't what they were a year earlier. A year earlier, however, the job growth data was still being compared to rather anemic numbers. The results being produced now are still historically strong, and have to be taken in their full context. Many investors aren't doing that, and that's working against stocks.

In terms of a school grade, last month's jobs data has earned a B+, and maybe even an A-. Traders are giving it a C, largely unsure if the report will postpone planned rate hikes for later this month. Then again, investors aren't even sure if rate hikes are a liability. The Fed puts higher interest rates in place to keep an overheating economy in check. Ironically, the condition to fear here is actually an FOMC that's unwilling or unable to push rates up. Investors may interpret that as bullish.