Option Trading School: Our Profitable SPY Credit Spread, Part 3

Welcome to part-three of this primer on credit spreads, which looks at one of the recent winners from our Index Options Timer to service to not just illustrate how these kinds of trades work, but why they work and when you may want to use them over straight-up buying of calls and puts.

And, congratulations! If you’ve not been overwhelmed to the point of throwing in the towel yet, you’re about to have the ‘aha’ moment. Before we get to it though…

If you’re confused and frustrated, don’t beat yourself up. Credit spreads (and all spreads for that matter) aren’t exactly intuitive trades. We’re conditioned to buy low and sell high, and we’re conditioned think directionally and one-dimensional. Credit spreads are neither of those things. You won’t get your ‘Eureka’ moment until you paper trade – pretend trade – a few of these on your own to see how and why they work.

In any case, where we last left off in part-two of this lesson was the shorting of SPY August week 4 (08/24) 279 put (SPY 180824P279), which put $53 per contract in our pockets. We were looking to take advantage of the natural time decay inherent with this holding. Each contract was losing about $6.00 worth of value every day just through the mere passage of time. Assuming the SPYders didn’t continue to sink, within a few days the SPY 279 puts would be worthless and we could sell them for (literally) nothing. That would mean that $53 ‘credit’ would be all ours to keep.

This is still a risky trade in and of itself though; all naked/short option positions are.

Solution? We buy a cheaper put to use as in insurance policy. That is, we can exercise (or sell) the put option we own to offset some of the downside that the 279 puts could have meant for us had things not gone our way. In this case, the SPY August week 4 (08/24) 278 puts (SPY 180824P278) were the best choice… not that the 278.50 puts wouldn’t have gotten the job done.

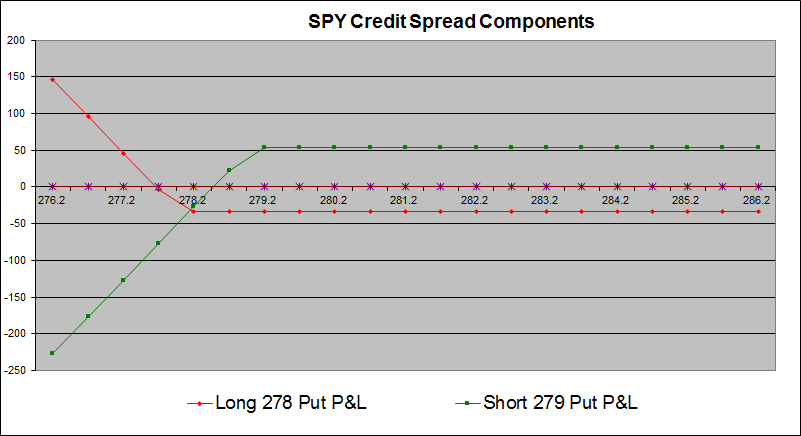

The 278 puts cost us around $34 per contract, which reduces our $53 credit we reaped by selling the 279 puts.

They were worth every penny though.

Think about it like this. If we’re only short the 279 puts and SPY stumbles to $276, we’re “on the hook” for the $3.00 difference. If we own 278 puts though, and the SPYders slide to $276, we can sell our 278 puts for at least $2.00 each. Those proceeds would offset the $3.00 loss we incurred on the 279 puts. How much? Our loss would be pared to only the $1.00 difference, but we’d still have net credit of 19 cents, or $19 per contract ($53 - $34 = $19) we reaped at the onset of the trade. Our maximum net loss on this position would have been $81 per contract (the $1.00 loss we’d take if SPY fell below 278, subtracting the 19 cent credit upfront).

The two graphics below clarify what's really going on. The first one is the profit and loss for each piece of two-legged trade. We know we're going to lose money on one of them. That's the plan. We want to lose money on the 278 puts we bought, as that leaves behind a profit via the 279 puts we sold. We might lose money on the 279 puts that we shorted, but if we did, we'd actually make a little of that money back by owning the 278 puts. It would still be a loss in that case, but a limited loss.

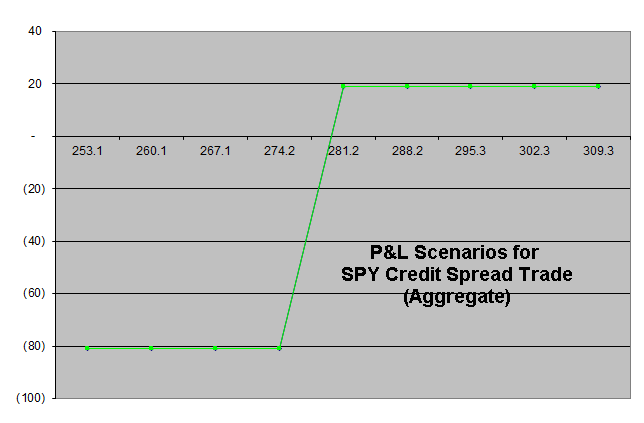

The next graphic below just plots the trade's profit and loss scenarios when combining, on a net basis, both of the P&L scenarios plotted on the image above.

It's still not a great risk-vs-reward scenario, putting $81 at-risk for a $19 credit for each contract pair we traded. It’s a misleading risk-vs-reward scenario though. The odds of the SPYders falling below $278 – or even below $279 -- were quite slim. and we were making $6.00 per contract, per day, just because time was passing. The person ‘on the other side of the trade’ was losing that $6.00 per day just because time decay was working against the value of the 279 put option. Even factoring in the time decay we were suffering with the 278 puts we owned, we were still money ahead.

By the way… in case you haven’t figured it out, for put credit spreads meant to be bullish, the shorted puts have the higher strike pricel we buy one of each (or two of each, or whatever). The puts you’re buying have a lower strike price. That’s why they’re cheaper. In this case both puts were ‘out of the money,’ though there are situations where ‘in the money’ puts used to take on bullish credit spreads make more sense.

Still confused? Again, don’t be. The best way to learn credit spreads is doing a few of them… on paper, of course.

That being said, the reason we chose credit spread here rather than simply buying a call was, with the call, we not only had to be right about the market rallying, but the market had to rally a lot in a short period of time to overcome time decay and poor responsiveness (low delta). By shorting a put instead, we didn’t have to be exactly right about the market’s direction. We would have made money had the S&P 500 ETF made its way higher, but we also would have made money even if the SPYders just moved sideways and time decay did the work for us. We were using the time decay to our advantage, rather than let it work against us.

The purchase of the 278 SPY puts was only and always a cheap way of protecting us from a dire and unlikely plunge for the market.

Clear as mud? Great.

If you’d just rather someone give you the fish rather than teach you to fish, the Index Option Timer Service is primarily a credit spread service. You could learn as much or more about the technique just by letting Price and his team tell you exactly what trades they’re recommending as you might be able to learn on your own. Or, better yet, why not take one of Price’s boot-camp classes?