Use Put Options to Make Money, Without the Underlying Stock Sinking: Put Credit Spreads Explained

Think a put option can only drive profits if the underlying stock or index moves lower? Think again. While the "buy low, sell high" (or "sell high, buy low," in the case of a put trade) is still sound axiom is still good advice, limiting yourself to the straightforward purchases of options doesn't let you capitalize on one of the biggest opportunities you have with puts and calls. That opportunity lies in the fact that all options experience time decay, meaning they lose value for no other reason than the passage of time... even if the underlying stock doesn't move at all.

A simple trade called a credit spread allows you to be a net-seller of options at the onset of a trade, putting money in your pocket upfront. The idea is to buy the trade back at a later time at a lower price. Or, better yet, let the options expire worthless so you don't have to buy it back at all - you keep all of the initial credit.

Clear as mud? Don't sweat it. We'll walk through an example of a credit spread.... a put credit spread, which is actually something of a bullish (or at least neutral) trade, meaning we DON'T want the underlying stock or index to move meaningfully lower.

A credit spread is a two-legged trade, meaning we use two options to take on the position. One of them is an option we short, or write, for upfront proceeds we add to our account. The idea is to keep as much of that initial credit as we can. Holding short option positions can be very risky though, so we also buy another option to use as something of an insurance policy. The cost of that purchase eats into our net proceeds, but it's worth it.

Let's assume we think fictional XYZ stock, currently priced at $139.53, is going to at least hold into its current price, and maybe even move a little higher. We think no matter what that it's not going to move meaningfully lower. We could buy a call and profit from any gain, or we could sell a put and let its value erode.... even if XYZ doesn't move at all. We'll choose the latter in this case, as there's mathematically more upside and likelihood in that trade. We can sell the $138 puts expiring a week from now at a price of 63 cents, meaning we can put $63 in our pocket right at the onset of the trade.

That's a position with near-infinite risk though. If XYZ plunges and the value of the 138 puts jumps, we'd have to buy it back at a much higher price (or risk having it exercised against us). To defend against that possibility, we also buy a cheaper put option that will increase in value should XYZ plummet. The next-best option in this case would be the 137 put, which currently trades at 43 cents, or $43 per contract.

[Note that the strike prices of both options are below the current price of XYZ; the short put's strike price is above the long put's strike price. It has to be that way. Otherwise there's no "credit."]

By collecting $63 for the 138 put and spending $43 on the 137 put, the trade nets us upfront proceeds of $20 per pair of contracts we're trading. As long as XYZ is at or above $138 a week from now when both options expire, we'll get to keep all of that $20. As long as XYZ holds above $137.80 through the next week's expiration, we'll at least get to keep some of that initial $20 credit. Anything below $137.80, and we'd have to close out both legs of the credit spread for a net less. (Or, if we chose not to close them out, we'd have them closed out at a net loss for us.)

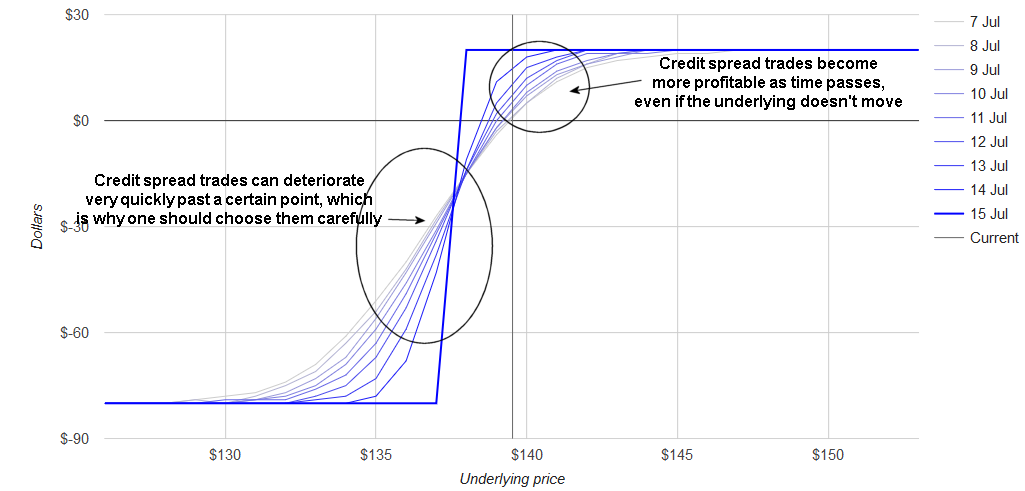

The profit-and-loss graphic below tells the tale of this trade, however, not so much because of the math but how the passage of time works in our favor.

On the image, the P&L scenario lines start faint and then get thicker as expiration day approaches. The thickest, darkest -- and straight -- line is our profit or loss on expiration day. Look closely, and you'll see that the trade becomes more profitable for us each passing day even if XYZ holds steady at its price of $139.53. That's time decay, or theta, working on our favor. When we own an option, time decay works against us because it lowers the value of the option. When we're short an option, time decay works for us because we sold the option first and are looking to buy it back later at a lower price (or not have to buy it back at all). Once the put options expire, we won't have to worry about it any longer - the $20 credit is ours to keep.

There's a downside of course. That is, should XYZ fall below $137 by expiration, we'd have to buy back the 138 put and we could sell the 137 put. Whatever the 138 put costs to buy back, we could sell the 137 put for only $1.00 -- or $100 per contract -- less than the 138 put trade's exit price. That $100 net outlay to close out both trades is subtracted from our initial credit of $20, meaning our maximum loss for the credit spread is $80. A wise trader, though, wouldn't allow himself to get that far underwater that quickly. And, as the profit and loss graphic illustrates, the passage of time helps abate that risk, and things don't get really scary until XYZ is under $138 and/or there are only a couple of days left until expiration.

Still confused? It's not your fault. Though it's a fairly simple strategy, it's also a little bit unconventional. Credit spreads essentially "sell volatility," which is not something we're generally taught is an asset you can buy or sell (or sell then buy). It's also difficult to get over the mental hurdle of using puts in a bullish scenario, or using calls in a bearish scenario.

The best way to get a firm grip on credit spreads is to try a few of them on paper first, to get the mechanics and nuances under your belt. Or, better yet, become a member of one of our service's that issues credit spread trade recommendations. Those are the Index Options Timer Service and the Credit Spread Advisory.