The Scary Part About This Selling? Investors Aren't Scared.

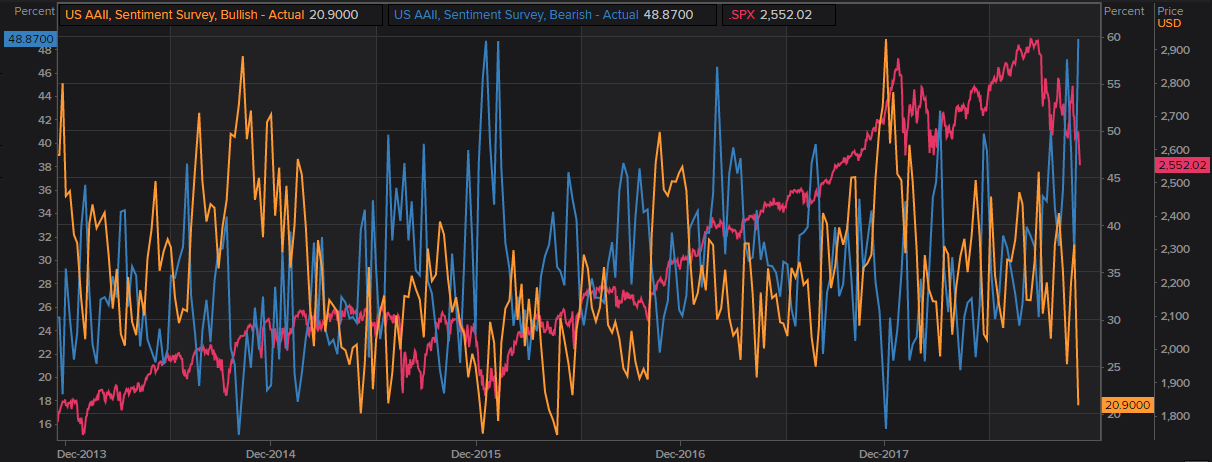

Last week it was pointed out - and we highlighted it - that the American Association of Individual Investors (AAII) was as collectively bearish as they've been in years. Of its members, 48.9% of them now count themselves as officially bearish, versus 20.9% of them being bullish. The other 30.2% of them are neutral. That's the highest bearish sentiment seen since mid-2013.

There are two interpretations of the data. One of them is the straightforward interpretation that suggests the crowd is right... that the next several months could be marked by even lower lows. The other interpretation is the less conventional but usually-more-right one, which suggests that stocks are at or near a major low.

See, history shows that, in general, the crowd is most wrong when it's most sure it's right.

AAII Historical Data

It's not just philosophical contrarianism. The graphic below compares historical AAII bearishness and bullishness to the S&P 500. It's not difficult to see that investors were the most worried when they should have been most bullish. And, vice versa. We were similarly bearish in January of 2016, at a major bottom, and conversely, we were wildly bullish in January of this year, right before a big pullback.

Yet...

Though history says this is a contrarian buy signal, that doesn't inherently mean the market's set to bounce straight away.

One of the shortcomings of using the AAII data as a contrarian tool is its lack of laser-like precision. It may well be right in telling us the selling is at or near exhaustion, but the pivot point could be weeks from now... and a lot can happen in just a few weeks. To that end, know that none of the usual short-term sentiment tools we normally consider have said we've seen a fear-based selling climax. The pullback, as big and painful as it's been, has been oddly orderly.

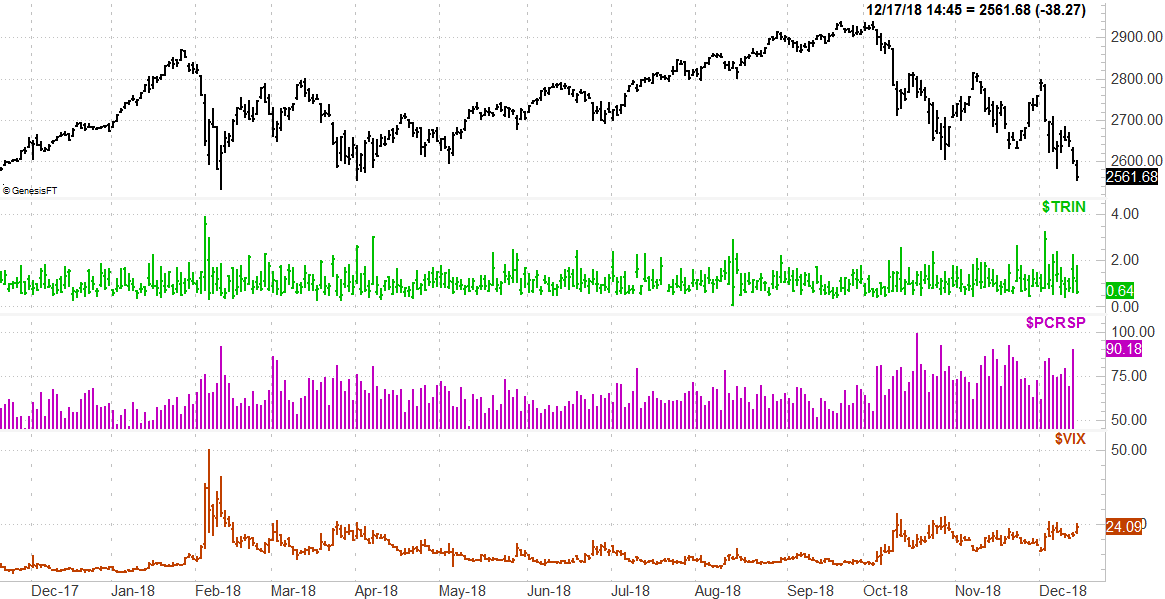

S&P 500 vs. TRIN, VIX and Put/Call Ratio

The graphic below compares the S&P 500 to (in order, from top to bottom) the NYSE's Arms Index - you know it better as TRIN - the S&P 500's put/call ratio, and the VIX. All three tend to surge when investors are panicking and flushing their portfolios. We saw this happen clearly on all three fronts in February, and though we had to do it again to a lesser degree in March, there's no denying that peak in fear was a major bottom for stocks.

This time is different, however. This time, while we've seen fair degrees of fear with a higher-than-average VIX and a higher-than-average put/call ratio, we've not seen any standout, outlier days from any of those three indicators. And, the modest surges we have seen have since been negated as buy signals by virtue of the fact that stocks have continued to move lower.

It's a problem, only because we need a blowout capitulation to make the pivot out of a downtrend and into an uptrend.

And there's the rub. The AAII data says the pump is primed for a reversal, but the final flushout of folks who've been willing to stick it out thus far has yet to take shape.

Most people are indeed out of the picture though. Investors have shifted their cash balances to the highest levels seen in almost three years; only 47.9% of portfolios are now in equities. The rest is being held as cash or cash-like instruments. Lipper said last week's outgoing flow of money from mutual funds was a record, and Bank of America/Merrill Lynch says the $39 billion investors took out of the market a week earlier was also a record.

Granted, both were records set after record-breaking inflows, but that doesn't change the message. Investors want out, en masse, and not because they were surprised. They thought about it. They planned it.

Still, in the absence of shrinking earnings or negative GDP growth, the economy is still growing. That, plus a mountain of money now sitting on the sidelines sets the stage for a big bounce once that cash gets put back into stocks.

The question is, when?

Bottom Line

The problem is, as long as the market's in the freefall it appears to be in right now, most traders and investors aren't even thinking about thinking in those terms. What they know right now is, the worse things get, the more inclined they are to sell. It doesn't pay to step in front of a freight train, even if that freight train is moving in the wrong direction. Worse, the freight train in question has developed some momentum.

Your job here is to keep a level head and understand that sentiment is a short-term phenomenon. It's a phenomenon that matters, but if investors finally do slip into full-blown panic mode, that's apt to be a buying point in front of a major pivot. Most people won't be talking about that prospect at the time.