Q1 Earnings Breakdown By Sector: Well, This is Concerning

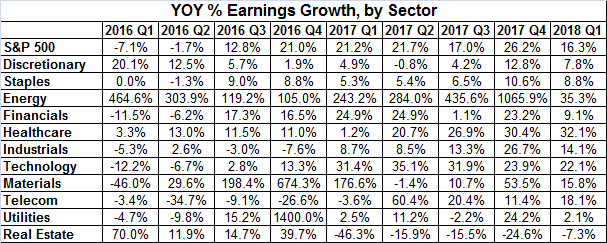

Earnings season doesn't have a "winner," per se, but if it did, the first quarter's champ would be technology stocks. However, financials would be a well-respected runner up. There were some sectors that posted bigger year-over-year growth rates, but not without a catch. For instance, the energy sector technically improved its bottom line by 243. That was only because Q1-2016's bottom lines were so pathetic, however. In terms of a normal/healthy comparison, technology and them financial stocks earned Q1's accolades.

Perhaps more encouraging it that in both cases, last quarter wasn't the first quarter financials and tech stocks reported double-digit growth. Each did the same last quarter (Q4) too. Better yet, the pros are looking for comparable growth for the coming four quarters.

Also noteworthy is a much-needed improvement in earnings for industrial stocks after a pretty frustrating 2016.

A couple of disappointments too... healthcare in particular. Analysts have been overestimating how well healthcare names would do for several quarters now, but last quarter's 1.2% earnings growth is by far the biggest shortcoming we've seen in several quarters. While the projected earnings growth rates look compelling, bear in mind the sector was supposed to be posting that kind of growth for the past several quarters, and never even came close.

Discretionary stocks also seem to have hit an earnings-growth wall.

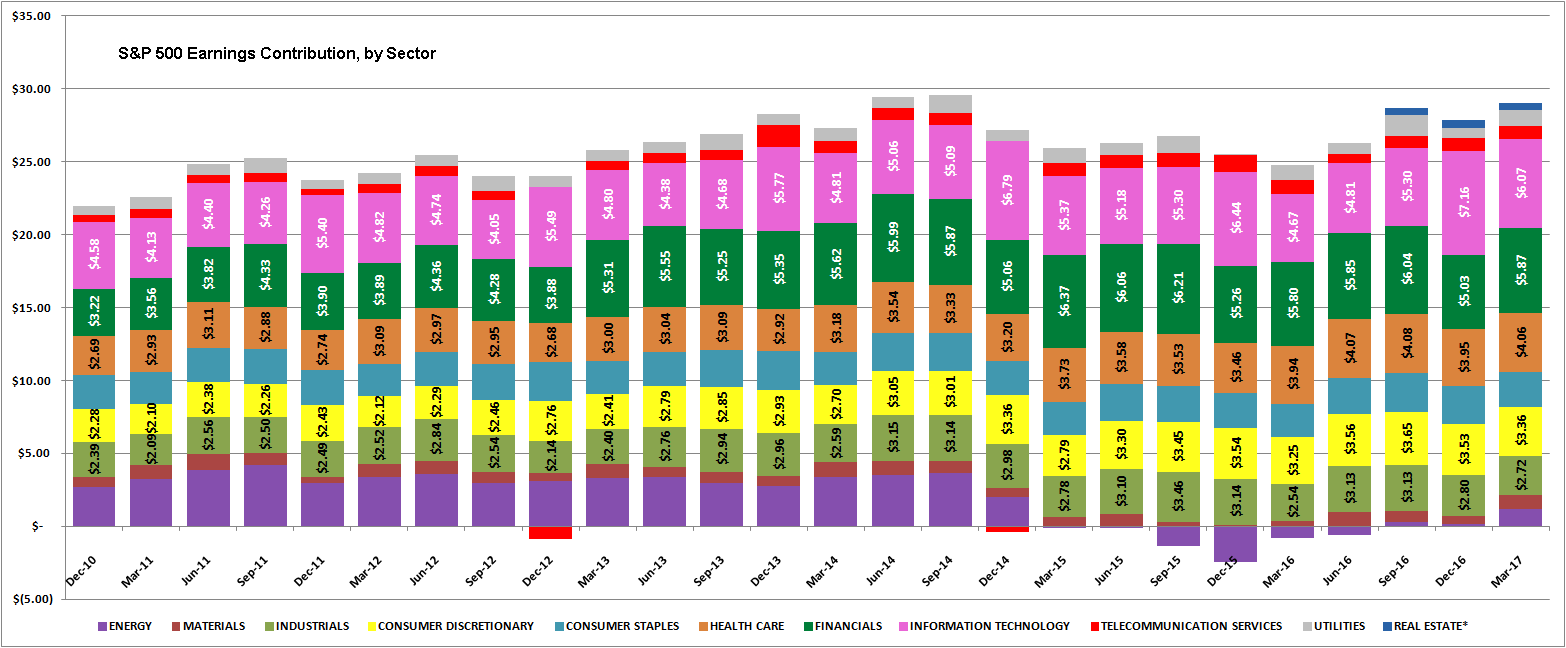

Be that as it may, a picture still says a thousand words, and a picture of the S&P 500's earnings trend, broken down by sector, is worth a look.

The image below plots the S&P 500's per-share earnings tally going back to early 2010, broken down by each sector's contribution to the overall bottom line. As you would expect, some sectors chip in more profits than others. The biggest contributors are no surprise either... technology names, then financials, and then healthcare. Consumer discretionary stocks are the fourth-biggest boost to the S&P 500's bottom line, though industrials aren't too far behind consumer discretionary names in terms of impact.

The size of each sector's overall profit contribution isn't the point or purpose of the image though. The primary goal here is simply to illustrate how little the energy sector has actually recovered since the 2015 meltdown of crude oil prices; energy stocks are still contributing less than half of what they were in 2014. Also worth noting is how the technology sector is the only one of the eleven segments that's actually mustered meaningful growth in its earnings contribution to the overall market over the course of the past several quarters. Financials, surprisingly enough, haven't added a whole lot of value to the S&P 500 since 2014. Consumer discretionary stocks have been doing the overall market more and more good, while healthcare stocks seem to have stagnated. [Click to enlarge.]

The data and its trends are important to understand if only to appreciate the notion that so much of the market's overall valuation -- the S&P 500's to be specific -- is dependent on just five sectors. The five biggest profit contributors account for 76% of its total profits.

In other words, if the S&P 500's trailing P/E of 21.7 [and forward-looking P/E of 18.0] is ever going to be "solved" be earnings growth, it's going to have to come from the technology, financial and healthcare sectors more than anywhere else. The energy sector has a chance to lend a big helping hand, but that doesn't look like it's in the cards anytime soon... especially with crude oil stuck under $50 per barrel.

Whatever the case, it never hurts to know exactly where the broad market's earnings are coming from, and where they're not coming from.

In this light, it's tough to see the S&P 500's collective bottom line justifying its valuation in the foreseeable future. If anything, disruption within the healthcare arena is going to serve as a headwind within the healthcare industry, and it's tough to imagine the tech sector being able to grow its bottom line adequately. Financials might be able to do better, if banks are able to squeeze out better margins as interest rates rise.

The sleepers: Industrials and consumer discretionary stocks. A true economic revival will provide oversized opportunities for growth there, though a lethargic economy could keep those areas in neutral, and serve as a drag on marketwide earnings.