Option Traders Are Betting Stock Volatility Will Rise With Bond Volatility

Traders Are Betting that Volatility is About to Spread

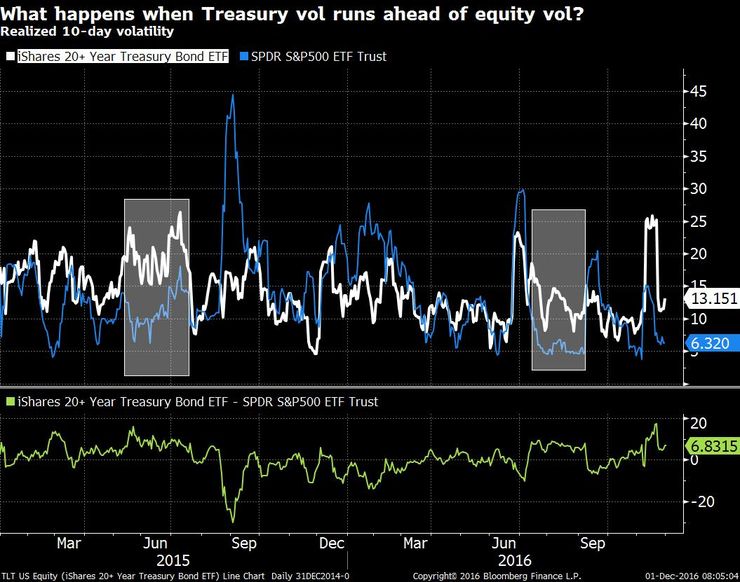

Will equity volatility catch up with the move in bonds?

by Luke Kawa

A measure of volatility for longer-term U.S. Treasuries recently hit its highest level since July 2015 as traders begin to price how President-elect Donald Trump's potential fiscal policies could prove game-changing for inflation and growth.

The 10-year U.S. Treasury yield has jumped nearly 70 basis points to 2.42 percent since Americans' votes were being tallied on election night, fueled by rising market-based measures of inflation expectations and uncertainty surrounding the new administration.

The S&P 500 index, however, proceeded to march to fresh record highs following the election — but now, traders appear to be betting that volatility won't remain confined to bonds.

The ProShares Ultra VIX Short-Term Futures exchange-traded fund (UVXY), which uses leverage in an attempt to magnify the daily returns an investor would receive from holding VIX futures, posted record trading volumes in November, surpassing its unleveraged peer in this regard in three of the past four months.

That could be a sign that investors are increasingly preparing for imminent turmoil in equities following the bond selloff, as VIX futures tend to move inversely to the S&P 500. Brean Capital LLC Head of Macro Strategy Peter Tchir noted that UVXY reached a record amount of shares outstanding on Wednesday, and that if history repeats itself, bond volatility could trickle through to other asset classes.

"We have recently seen one of the largest divergences with treasury realized volatility being much higher than equity realized volatility," writes Tchir. "The last two times we saw treasury volatility run higher than equity volatility for a period of time, we saw selling pressure in equities shortly thereafter."

Source: Bloomberg

"It is a weak link and recently treasury vol has subsided (even if it doesn't feel like it) but something to watch," he added, highlighting the event risk of the Italian referendum and likely Federal Reserve rate hike later this month.

It's worth noting that this series of events, if realized, would be nearly precisely what Bank of America Merrill Lynch's Head of Global Rates and Currencies Research David Woo had predicted ahead of the election.

In August, Woo warned that if the Republicans or Democrats managed a clean sweep, expectations of fiscal expansion would spur a selloff in rates and cause acute harm to risk-parity portfolios, which at the time were standout performers on the year. A BofAML index highlighted by the strategist as a suitable proxy for such a portfolio has come under pressure since the election, falling by more than 3 percent to trail the S&P 500 index on a year-to-date basis.

Source: Bloomberg

Similar indexes from Salient and AQR have also fallen on tough times since Nov. 8.

This approach to portfolio construction, at its most basic level, employs a long, levered position in Treasuries in tandem with a long position in stocks.

Typically, Woo said, weakness in the bond portion of this portfolio is the proximate cause of its bouts of underperformance. The potential for volatility to bleed over to stocks, as indicated by traders' enthusiasm for leveraged VIX products, would be both bad news for risk assets and afflict further stress on risk-parity portfolios.

Courtesy of bloomberg.com