Modest Job Growth Isn't the Problem - Stagnant Wages is the Problem

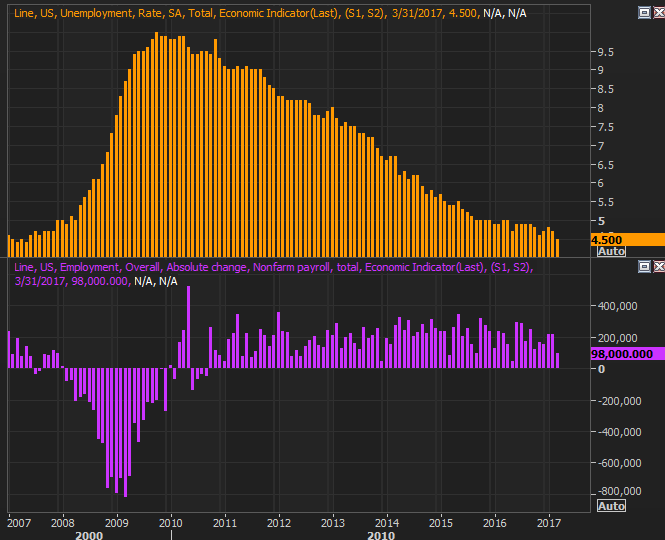

Whoops. Despite the strong showing on Wednesday from payroll processor ADP on the jobs-growth front, the Department of Labor didn't quite come up with a comparable measurement. Although the nice drop in the unemployment rate -- to a multi-year low of 4.5% -- is a big moral victory, the DOL said on Friday morning that only 98,000 new jobs were created last month. Economists were looking for 180,000 new payrolls.

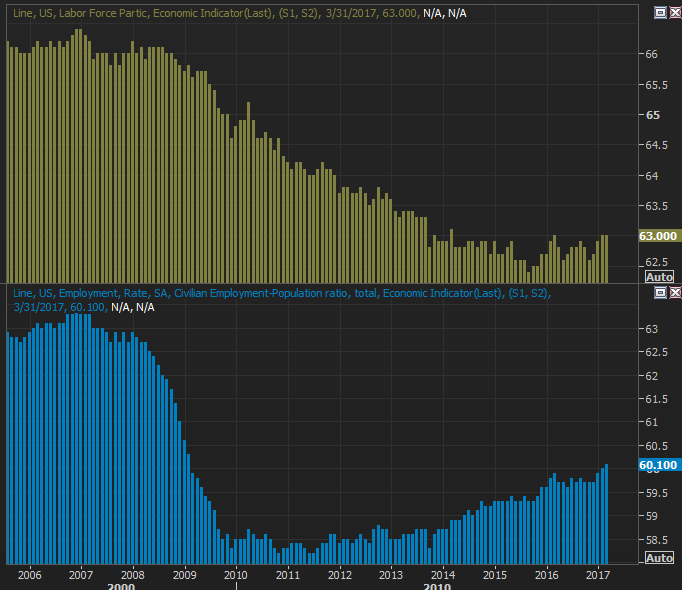

Of course, the most-touted numbers don't tell the whole story. A complete and fair look at the employment picture requires a look at all the data, beginning with the labor force participation rate, and the employment/population ratio.

Both have been uncomfortably low since cratering in 2008, although one has been somewhat on the mend since 2011... the employment/population ratio. That measure moved to a new multi-year high for March. The labor force participation rate didn't move higher last month, but it didn't move lower either, rolling in at 63.0% again.

The participation rates and employment rates tilt the overall data in a bullish direction.

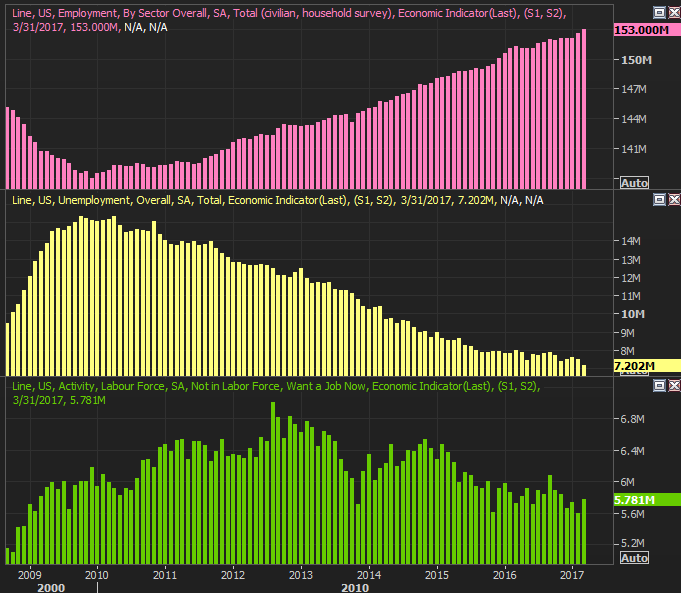

Perhaps the most telling of all the numbers are also the least-discussed ones - the raw number of people who are working, who are officially unemployed, and the number of people who are unemployed but aren't receiving any kind of unemployment benefits either. The number of people with a job reached a record high of 153.0 million, the number of people counted as unemployed fell to a multi-year low of 7.202 million, and though the number of people not in the labor force that still want a job edged a little higher to 5.78 million, that bigger trend is still pointed downward.

The glass is half full rather than half empty.

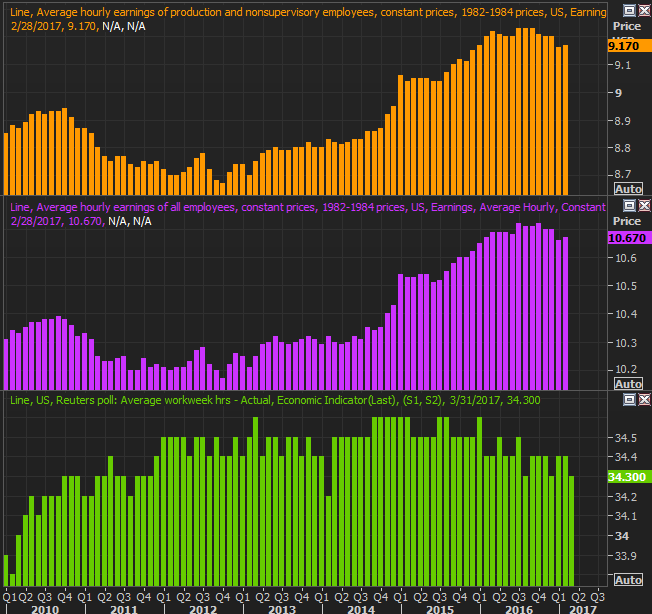

One of the biggest challenges in adding a large number of new jobs to the mix is that most people who want to work are indeed working. It may not a job they like or they may not be on the career path that want, but structurally, an unemployment rate of 4.5% is considered full employment. The litmus test, so to speak, is on the wage front. If the jobs picture is truly improving and employers have to compete for qualified workers, that will show up on everyone's paycheck.

To that end, wages did go up last month. They didn't rise the expected 0.3%, but hourly pay rates did rise 0.2% in March. Workers worked almost the same 34.4 hours they did the prior month - in March, they typically worked 34.3 hours.

The chart below only plots the average hourly income through February, though the workweek bars are through March. While the updated version will show a second month of improving wages, the broadly shrinking workweek isn't a step in the right direction. And, though wages are edging slightly higher, it's easy to muster a bounceback in the shadow of the earnings decline we saw late last year. This isn't "strength" in the usual sense.

While this information doesn't make the glass half empty again, it does make the glass just barely half full. We're making about as much measurable progress as we could expect to make here. It could take months to see economic strength start to make a big difference in wages and hours. In the meantime, we'll have to settle for small differences.