Weekly Market Outlook - The Best and Worst Possible Kind of Breakout

Despite last week's bullish start, the buyers offered very little follow-through in the middle of the week. Too much political noise kept traders on the sidelines. That all changed on Friday though, and with very little prodding. Thanks to Friday's 1.74% jump from the S&P 500, the index booked a gain of 3.5% for the week... one of the biggest weekly gain in years. The NASDAQ Composite reached a record high,

The $64,000 question is, can it last? It's certainly not the ideal launch of a new breakout. But, this is also a market that's made a habit of doing the unthinkable and doing the illogical.

We'll look at all of it below. First though, let's set the backdrop with last week's and this week's economic news.

Economic Data

A fairly busy week last week, ending with some rather amazing employment news for February. But, let's look at the data in order of appearance.

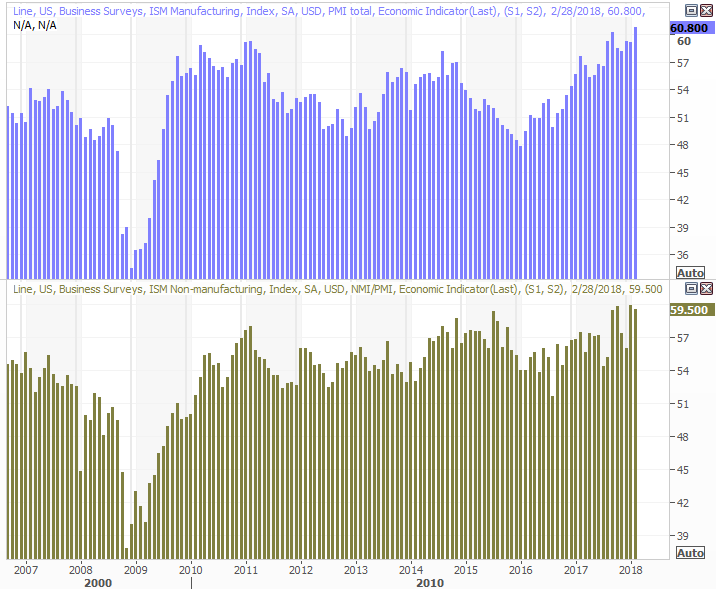

The IDM Services report for last month got the party started on Monday, rolling in a little lower than the expected 59.9, but still plenty respectable at 59.5. You'll recall the ISM Manufacturing Index from two weeks ago hit a multi-year high of 60.8. Together, the two ISM readings paint a pretty rosy picture.

ISM Manufacturing and Services Index Charts

Source: Thomson Reuters Eikon

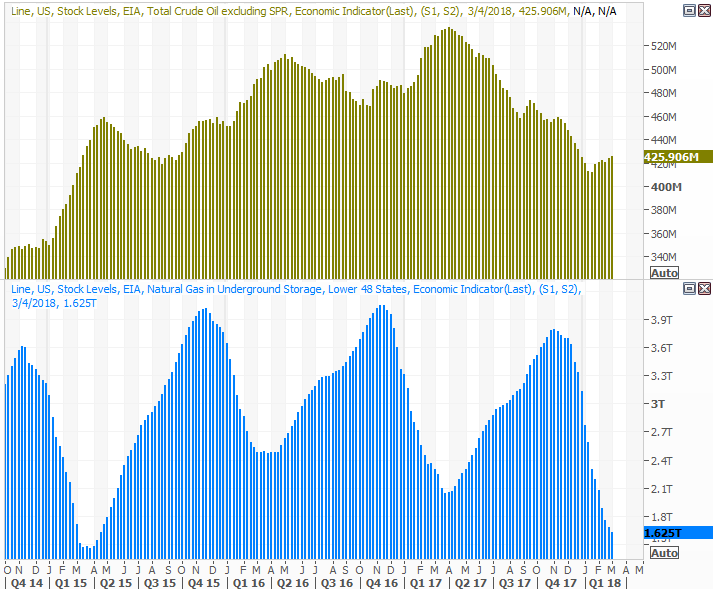

It's been a while since we needed to bother taking a look at it, but just for good measure do note the crude oil inventories continue to inch higher. They're not rising enough to outright pull the rug out from underneath oil prices, but they're certainly not helping. Meanwhile, natural gas in storage continues to slide, though that descent is slowing down.

Crude Oil, Natural Gas Inventory Charts

Source: Thomson Reuters Eikon

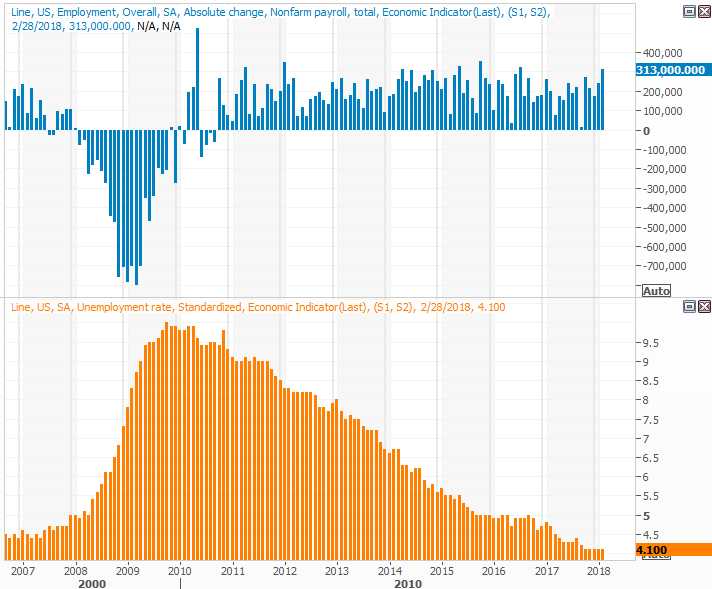

The big Kahuna, of course, was February's job growth. Economists were looking for payroll growth of only 210,000, but we actually saw 313,000 new payrolls added for the month. That's the most additions since mid-2016. It wasn't enough to push the unemployment rate any lower than 4.1%, but that's not unusual in that the nation is pretty much at its lowest plausible unemployment rate.

Payroll Growth and Unemployment Charts

Source: Thomson Reuters Eikon

If anything, the jobs report's superficial data understates the actual employment picture. We took our usual in-depth look at all the employment data at the site. Be sure to see it for the bigger picture.

Everything else is on the grid.

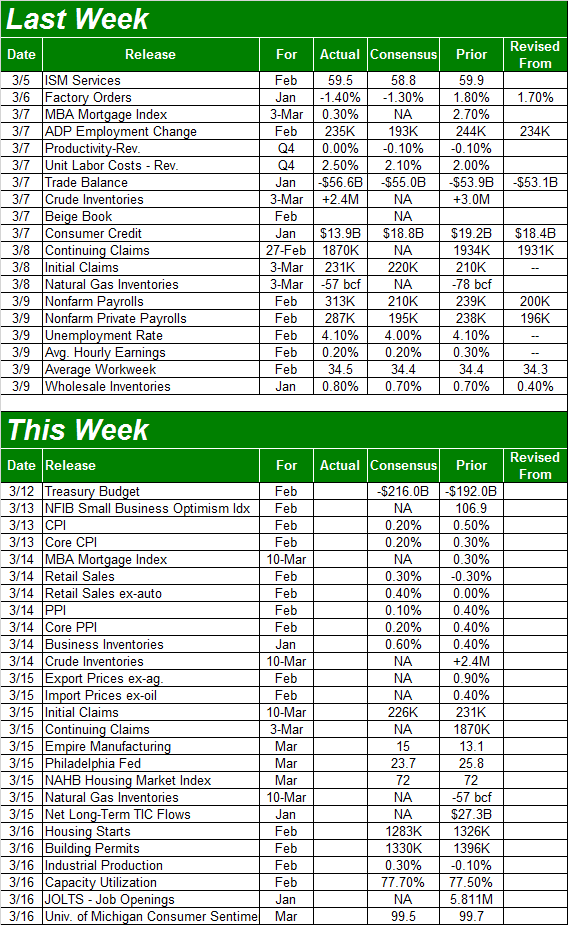

Economic Calendar

031118-econ-data)

031118-econ-data)

Source: Briefing.com

This week is going to be super-busy, perhaps fanning the flames of the bullishness that materialized last week.

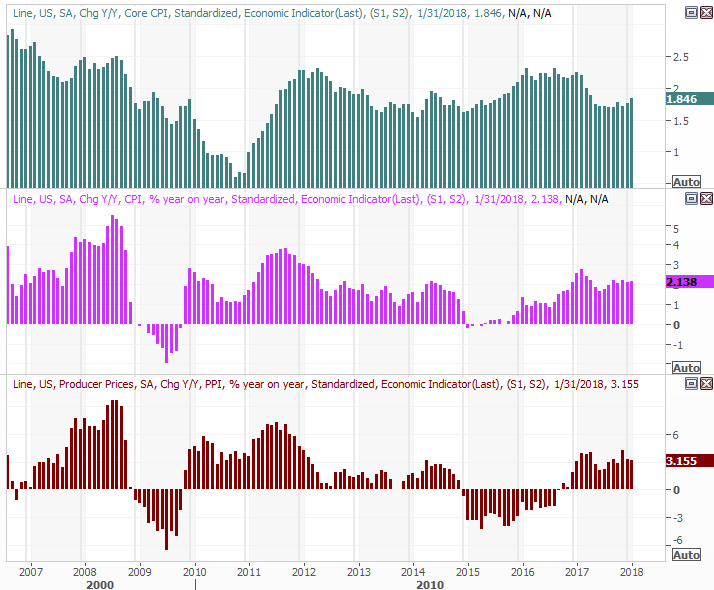

The party starts on Tuesday with last month's consumer inflation report, which will be followed on Wednesday with February's producer inflation numbers. The pros are calling for more muted price gains than we say a month ago, though are calling for price gains nonetheless. Annualized rates remain high enough to keep the Fed on track to put in two or three more rate hikes before the end of the year (and maybe more, if inflation persists).

Consumer and Producer Inflation (Annualized) Charts

Source: Thomson Reuters Eikon

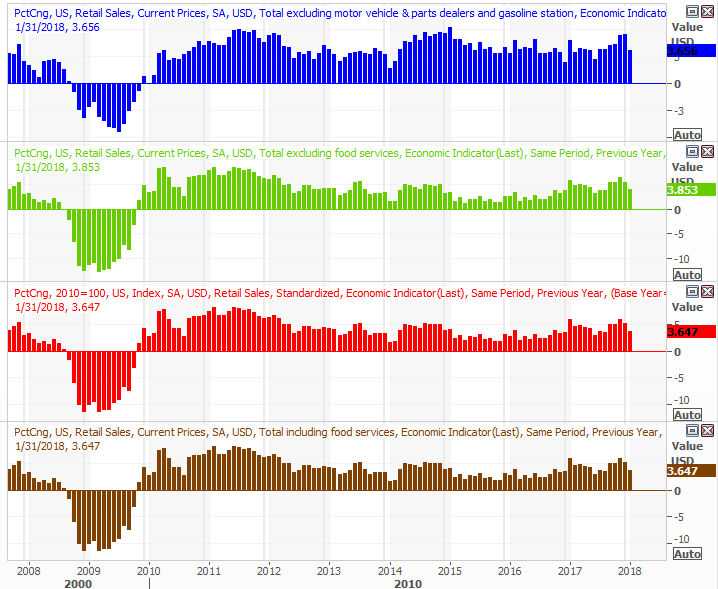

We're also going to get last month's retail sales report on Wednesday. You may recall the headlines from last month's retail spending data sounded grim, but the comparison to December's growth wasn't exactly meaningful. On a year-over-year basis, they were still up quite a bit. Thing is, not only are analysts looking for very strong comparisons to January's spending levels, the numbers may even be stronger on a year-over-year basis. We'll dish out those details shortly after the data comes out. Either way, consumerism is alive and well, regardless of the suggestions saying otherwise.

Retail Sales Growth (Annualized) Charts

Source: Thomson Reuters Eikon

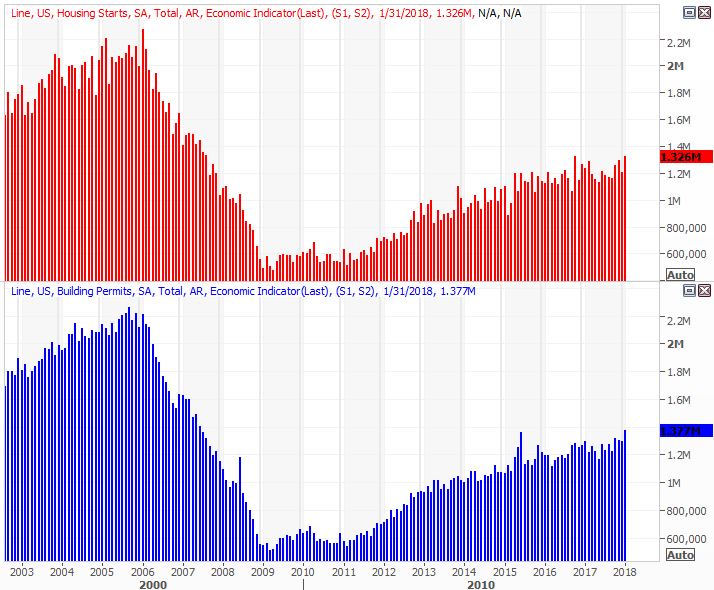

On Friday we'll hear about February's housing starts and building permits. Both were well up in January; economists are looking for a slight cooling on both front. Each trend is still broadly on the rise though, even if actual purchases of new homes remain lackluster. One or the other will have to give eventually, and with mortgage applications slowing down in step with rising mortgage rates, we fear it's the starts and permits data that's going to stumble.

Housing Starts and Building Permits Charts

Source: Thomson Reuters Eikon

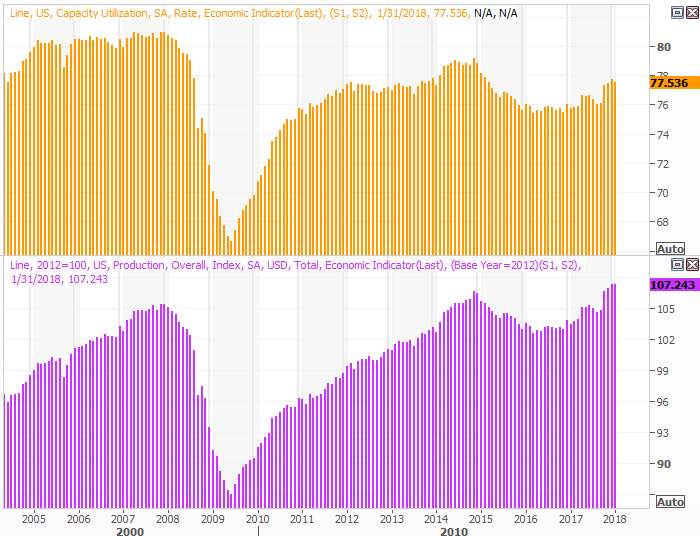

Last but not least, also on Friday we'll get last month's industrial productivity and capacity utilization data.

We've mentioned before the correlation between those numbers and corporate earnings is a strong one, so we won't belabor that point again. We'll just point out that the pros are expecting a little forward progress again, which bodes well for the long-term market. The short-term market... not so much.

Industrial Production and Capacity Utilization Charts

Source: Thomson Reuters Eikon

Index Analysis

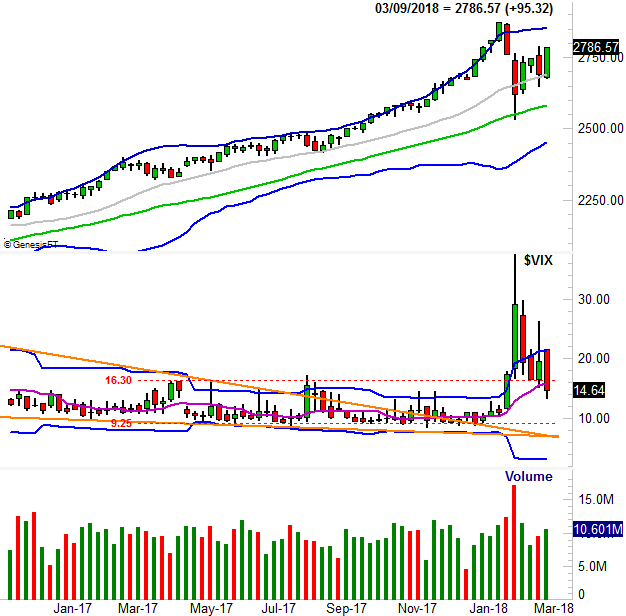

We'll start this week's analysis with a look at the weekly chart of the S&P 500, just to put last week's bullish reversal of the previous week's bearish reversal in perspective. Nothing really changed with the status quo from... well, now three weeks ago. But, traders continue to be willing to keep buying on the lack of adverse news.

S&P 500 Weekly Chart, with VIX and Volume

Source: TradeNavigator

Also notice that the VIX broke under a key level at 16.3, and also broke below its 50-day moving average line at a time when it didn't look like it would do either. And, there's room for the VIX to keep moving lower before it revisits the more absolute floor at 9.25. That's all bullish.

When we zoom into the daily chart of the S&P 500, we can see the cracks in the bullish effort. Namely, we left behind a bullish gap between Friday's low and Thursday's high. Generally speaking, the market doesn't like unfilled gaps. Never even mind the fact that the gain unfurled despite a lack of any 'new' news.

S&P 500 Daily Chart, with VIX and Volume

Source: TradeNavigator

The daily chart of the NASDAQ Composite looks about the same, for better or worse, though it hit record highs on Friday as it left behind a bullish gap. It's also interesting that the volume behind the gains last week was not only firm, but progressively better. This had been the missing ingredient with many of the past rally efforts (though that volume growth isn't evident on the daily chart of the S&P 500).

NASDAQ Daily Chart, with VXN and Volume

Source: TradeNavigator

And this is where some philosophical problems start to surface.

We posted some third-party commentary on the matter at the site last week. One of them was a concern that tech giants Netflix and Amazon had been stunningly bullish, but a closer look at the market reveals not much else has been all that hot. It's a problem, because rallies should have broad participation. Jim Cramer made a similar complaint the day before that not enough stocks were going higher, which would eventually prompt investors to throw in the towel in a broad sense. Yet another similar argument was made the day before that, pointing there weren't enough advancers compared to decliners, despite the bigger-picture rally.

Put it all together, and this rally may not be everything it's supposed to be.

Still, it's tough to deny there's some bullish momentum on the table, and this is an environment where momentum has been able to remain in motion by keeping traders excited.

We're not going to make a call here. We're just going to caution that the bears are apt to push back here, if only to close the gap. It's what happens when this rally is tested that will really interest us. As long as the S&P 500's moving average lines hold up as support levels, we'll lean bullishly. It's certainly not going to be straight-line bullishness though.