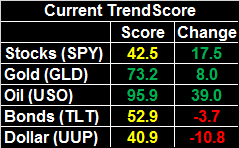

Weekly Market Outlook - Proof That It's All in the Follow-Through

The market may have mustered a gain last week, but it was anything but a decisive victory. The indices didn't clear some key technical resistance, and once again the volume supporting the advance was feeble. This whole thing could still crumble easily enough... ultimately proving it's not the initial bullish effort that matters, but the one that will carry stocks over the proverbial hump.

Traders are mostly waiting on earnings season to begin in earnest, which could prove very good, or very bad, for stocks.

Traders are mostly waiting on earnings season to begin in earnest, which could prove very good, or very bad, for stocks.

We'll dissect the indecision below, as always, after a run-down of last week's economic news and a preview of what's on the dance card for this week.

Economic Data

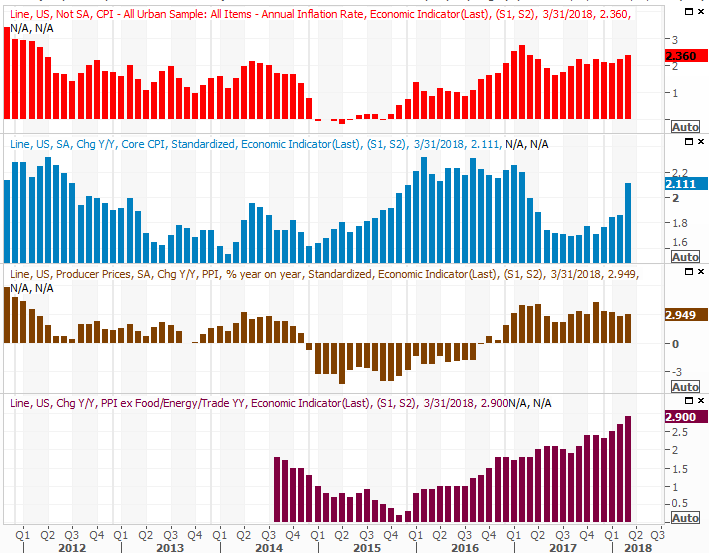

A relatively light week last week in terms of economic information, with the highlight being inflation. As has been the case for a while, we have some, though not an overwhelming amount (and producers have even less). It's a nice "not too hot, not too cold" balance that the Fed seems to understand it has to maintain. The "annualized inflation rate" now stands at a palatable 2.36%.

Producer and Consumer Inflation (Annualized) Charts

Source: Thomson Reuters

No need to chart is, but the Job Openings and Labor Turnover Survey ("JOLTS") reading for showed 6.05 million open positions, down from 6.22 million in January. It doesn't mean a lot; both are still sky-high readings. And, February's numbers may have been stifled by inclement weather.

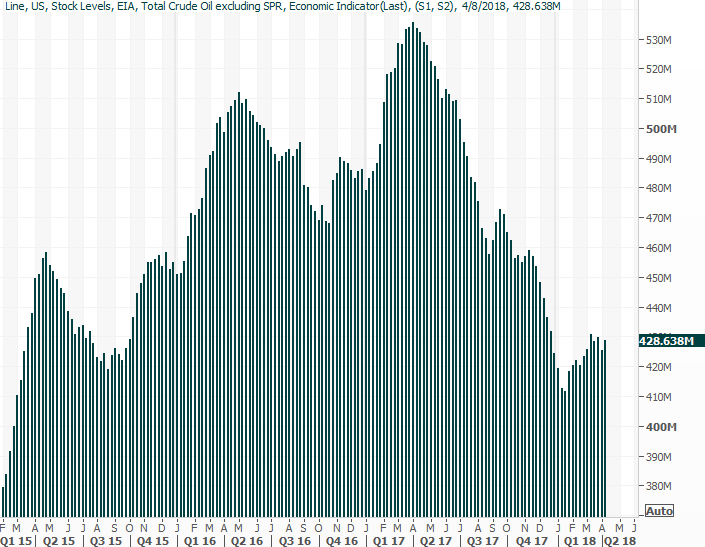

Also note that crude oil inventory levels edged a little higher a week ago, after a modest lull the prior week. It's still not clear which direction the trend is presently pointed.

Crude Oil Inventory Charts

Source: Thomson Reuters

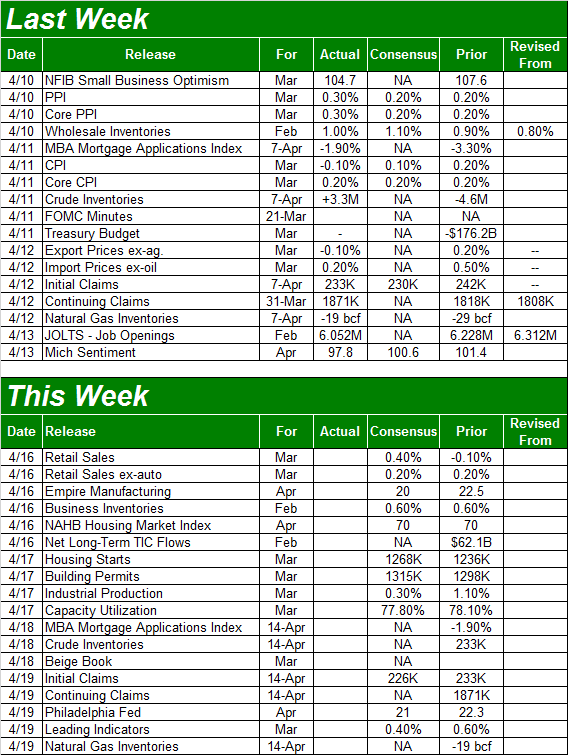

Everything else is on the grid.

Economic Calendar

Source: Briefing.com

This week will be a little busier, and a lot more important.

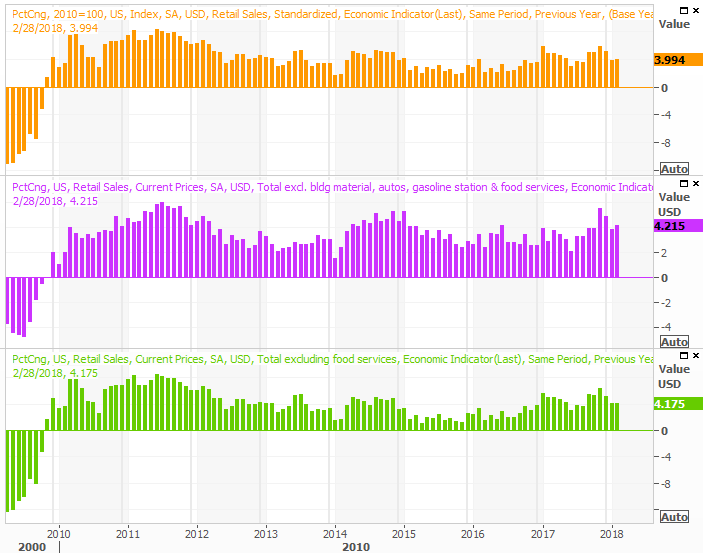

The party starts on Monday with March's retail sales figures. The pros are calling for healthy gains, and even more so when factoring in last month's auto sales (which we already know were quite strong). Economists expect a 0.4% uptick from February's pace. Whatever's in the cards, the bigger trend is pretty strong, and strengthening.

Retail Sales YOY Growth Charts

Source: Thomson Reuters

We'll also get last month's housing starts and building permits report on Tuesday. This has been one of the economy's real bright spots, and not gotten the full credit it deserves. Though it ebbs and flow, the bigger trend remains encouraging, and economists expect even slightly better numbers for March.

Housing Starts and Building Permits Charts

Source: Thomson Reuters

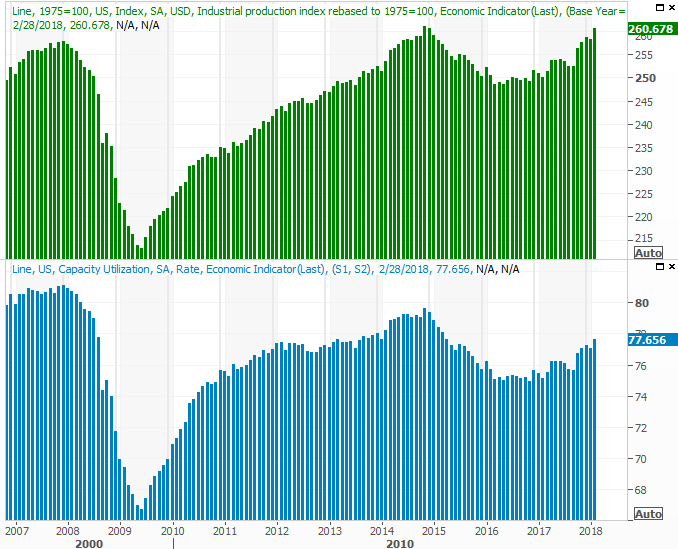

Finally, and arguably the most important data set to watch as we head into earnings season, look for last month's capacity utilization and industrial productivity figures for last month on Tuesday as well.

We've said before that the correlation between this data and corporate earnings, and therefore its correlation with the prevailing market tide, is tremendous. Though this information can't stave off a short-term swing (for better or worse), it is an anchor for long-term action.

The bad news is, the pros aren't looking for the same heroic numbers we got in February. Production growth is only expected to move up to the tune of 0.3%, and capacity utilization is expected to slide from 78.1% to 77.8%. All the same, the overall trend remains a healthy one.

Capacity Utilization and Industrial Productivity Charts

Source: Thomson Reuters

Tepid numbers on Tuesday aren't the end of the world. A string of tepid numbers would be a concern though.

Of course, we've seen some pleasant surprises on this front in recent months, and have no reason to think we're headed into any real trouble now.

Index Analysis

It coulda been worse, but it coulda been better. The market managed to eke out a gain last week, but it was a half-hearted effort... the kind that doesn't exactly inspire follow-through.

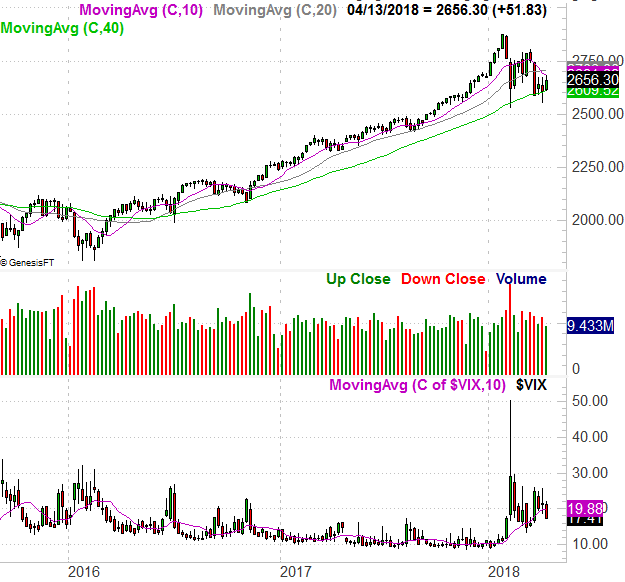

How so? The S&P 500, for instance, fought its way back above the 20-day moving average line (blue), but the move didn't push its way back the 50-day (purple) or the 100-day (gray) moving average line. And, if you look closely, you'll see a relatively alarming lack of volume with last week's modest bullishness.

S&P 500 Daily Chart, with VIX and Volume

Source: TradeNavigator

Zooming out to a weekly chart of the S&P 500 puts things in more perspective, including the whole "stuck between a rock and a hard place" paradigm. Most investors more or less know the 2016-2018 move was unusual and leaves behind the need for a correction. But, most investors also know that headlines are doing a lot of heavy lifting here... more so than they normally might.

That's the long way of saying traders are wise to ride the tide, even if it's not a completely rational bullishness.

S&P 500 Weekly Chart, with VIX and Volume

Source: TradeNavigator

There's empirical evidence to call this a low-volume rally effort. It's on the chart below, which plots moving averages of the daily "up" volume and "down" volume - marketwide - each day. Though the amount of bearish volume has been broadly slumping since the market bounced a couple weeks, the bullish volume growth has fizzled out the past few days. Investors just aren't convinced enough this is going anywhere. [The faint lines are the raw daily data; the bolder, brighter lines are the moving averages that indicate the underlying trend.]

S&P 500 Daily Chart With Up/Down Volume Trends

Source: TradeStation

The take-away? More than anything, right now know this is a scenario where making any kind of assumption isn't worth the risk. The short-term trend is bullish, as is the long-term trend, but the intermediate-term trend is actually bearish by virtue of what is a lower high... a high lower than March's peak. Politics, more than anything else, has investors second-guessing themselves every few days, and it's time for such another swing. And, with the way the upper Bollinger band is falling fast into the 100-day and 50-day moving average lines, it would be a miracle for the S&P 500 to push its way past the technical ceiling around 2695.

The flipside? The S&P 500 would need to break below the 200-day line (green) for this whole thing to get ugly to the point where it merits doing something about it. And, the lower Bollinger band is rising fast. It could bolster the 200-day line's support qualities within just a few days.

If you think this indecision is an accident or coincidence, it isn't. The market tries to vex as many people as possible as much of the time as possible, and that's certainly what's happening here. The market will break out of the funk soon enough - right when people are convinced stocks are going to stay stuck in the mud for a while.

Again, we're looking for the VIX to tell us when things are ready to move outside of the market's current confines. Until then, be patient... as tough as that may be.