Not surprisingly, June's employment report needs some explaining.

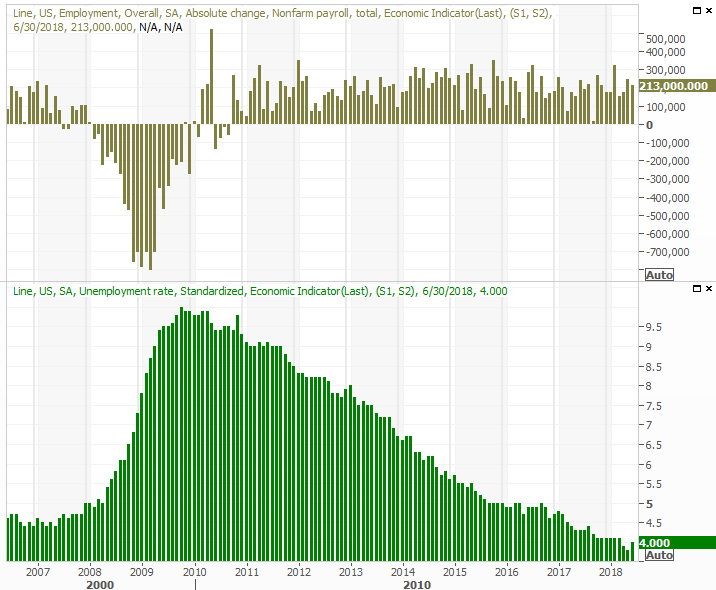

What you know. Last month, the U.S. economy added/created 213,000 new jobs, versus expectations of only 190,000. And, despite job growth, the unemployment rate edged a little higher, from 3.8% to 4.0%. The pros were expecting another read of 3.8%.

Few would argue that June's numbers weren't "good" overall, but were lamentable relative to expectations. They were also problematic in that the economy is supposed to be roaring. Rising unemployment and a rising unemployment rate [nope, not the same thing - we'll discuss below] aren't exactly screaming beacons of strength. This is a case, however, where you have to understand HOW these numbers are calculated and also appreciate the nuances of this data. All things considered, June's report was about as good as you'd want a report to get.

But, first things first... the plot of payroll growth and the unemployment rate. For what it's worth, April's and May's job-growth figures were both revised upward again. The only reason these numbers haven't been higher is a lack of employees willing and able to do particular jobs.

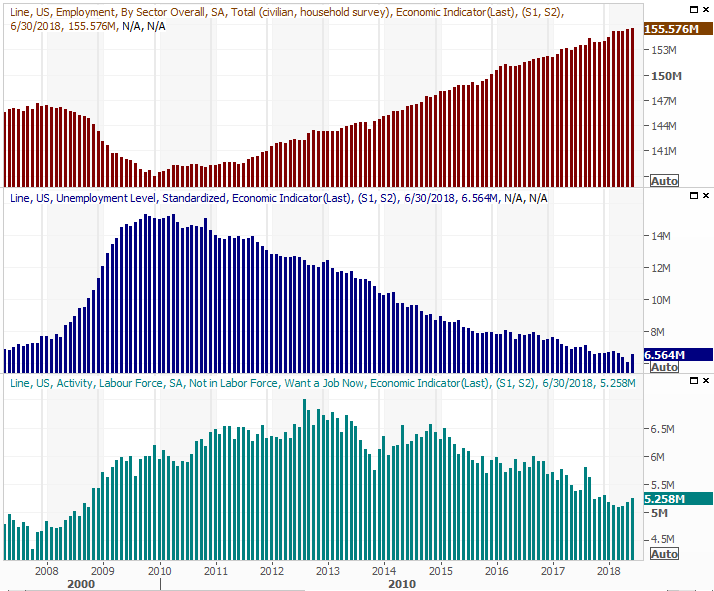

The raw, underlying data: Last month, 155,576,000 million people had jobs in the United States. That's good. In fact, it's (another) record. The bad news is, 6,564,000 people were officially unemployed... meaning they were able to claim unemployment benefits, forced out of employment not by choice. That was up from May's abnormally low print of 6,065,000 unemployed folks, but still, one would hope/expect this number to continually inch lower. Meanwhile, the number of people who aren't officially unemployed - not eligible for benefits - inched higher again as well, from 5,183,000 to 5,258,000. Again, this is a case where you'd hope/expect the figure to be falling, in light of news that so many job opening are going unfilled.

This is tricky to read. And, this is why the unemployment rate was able to move a little higher last month.

The official 'unemployment rate' is the result of dividing the number of people officially unemployed (6,564,000 people, as of last month) by the total number of people officially in the labor pool. The former grew a lot more than the latter did in June. But, there could be transitional reasons for it. One of them is the introduction of recent college graduates that ultimately displaced people who didn't just graduate from a college or university. Another less transitional explanation is the ongoing outsourcing of jobs... either moved overseas, or taken on by robots/automation.

Either way, last month's uptick isn't alarming. It would only turn alarming if it started to trend higher... something that could take a few months to determine.

As for the people who aren't in the labor force but still want a job (all 5,258,000 of them), that's a modest concern that doesn't quite make sense either. Again, there are a massive number of unfilled job openings.

Answer: There aren't as many 'willing' workers to take certain jobs. That's the polite way of saying a sizeable segment of the people polled by the Department of Labor like to say they'd like to work, but they don't really want a job... or only want a certain kind of job that's out of reach.

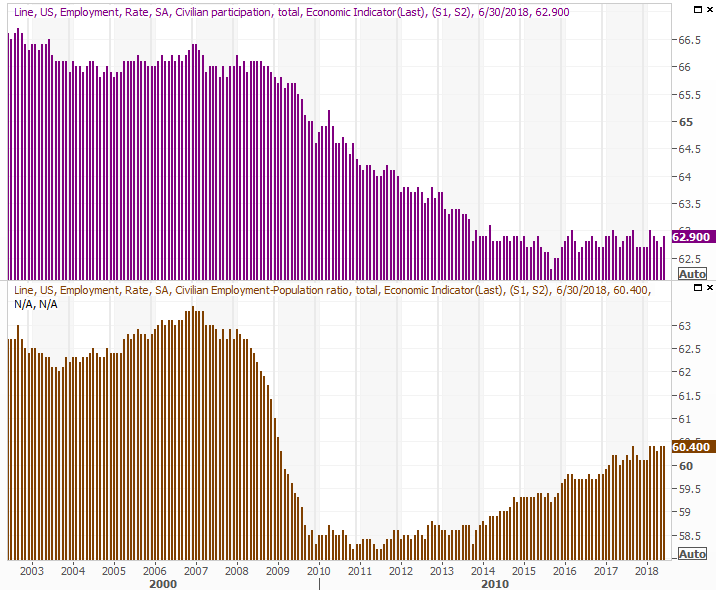

That premise is supported by the fact that, despite the uptick in the unemployment rate, a greater portion of the country's inhabitants are now in the labor pool (employed or not), and just as important, a greater portion of the U.S. population is now working than we've seen in a while. Those proportions are 62.9% and 60.4%, respectively. The fact that the latter - the employed/population ratio - didn't sink but has held steady since early this year is the proverbial litmus test that says we're not moving backwards in terms of jobs.

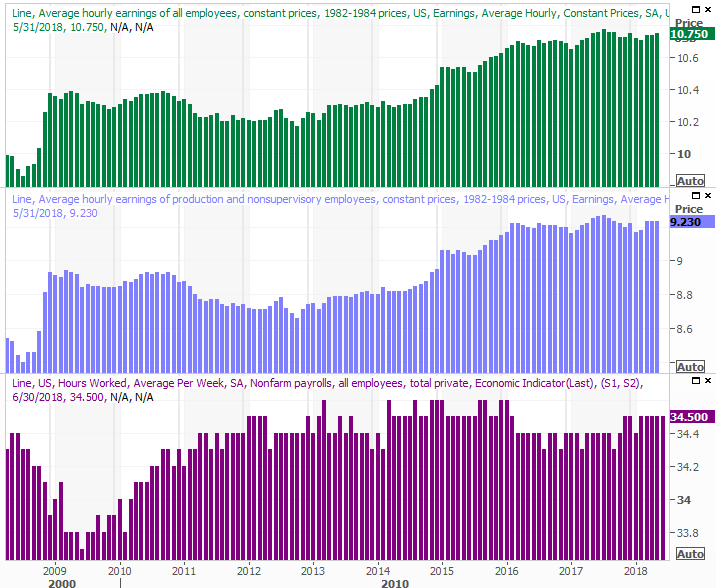

Last but not least, average hourly earnings grew 0.2% versus expectations of 0.3%. That's a month-to-month calculation. On a year-over-year basis, wage growth was more in line with inflation, and then some.

This is another two-edged sword. In the one hand, wage growth is an indirect sign of how strong or weak the job market is. On the other hand, too much wage growth implies an unhealthy level of inflation. In this case, the tempered but measurable growth loosely indicates that hiring hasn't become painful for employers. More than that, it implies those companies won't have to pass along those higher labor costs to customers. [The graphic below only shows hourly rates through May; you'll have to mentally add the impact of slight wage increases for June.]

Bottom line? June's job report is one that many observers are trying to turn into a "glass half empty" scenario. But, the effort to do so is largely unsuccessful, and off target. If anything, Friday's jobs report is a glass-half-full scenario, and then some. We're seeing more jobs created, and accepted, with wages improving. But, wages aren't improving at a rapid rate that will force the Fed to get overly aggressive in its fight against inflation.

But rising levels of unemployment? That's arguably the most misleading aspect Friday's numbers. Jobs are there for people who really want jobs, despite headwinds.

All in all, last months' jobs report was a 'Goldilocks' report, in that it wasn't too hot, or too cold. That kind of consistency is just what we need right now.