Iron Condors Aren't as Complicated as They May Sound

The term "iron condor" can be an intimidating term, even to veteran options traders who haven't take on such trades before. But, the nickname for the strategy is more forlorn than it really needs to be. An iron condor is simply the combination of two spreads that -- together -- offer a position with a limited amount of risk regardless of how far the underlying stock may move.

As is always the case, walking through an example will help clarify why traders need not fear this rarely-utilized approach.

In iron condor is a trade that does NOT want the underlying stock or index to move. Rather, it's a trade that achieves its maximum profitability when the stock (or index) stays right where it is at the time of entry. To that end, though it's often classified as a neutral strategy, it would be better described as a stagnation strategy.

Let's pretend we think PepsiCo (PEP) shares are going to hover right around their current price of $113.74 until the next expiration day two weeks from now. To effectively make that bet using options we would want to...

- Sell (short) one out of the money put

- Buy one out of the money put (with a lower strike price)

- Sell one out of the money call

- Buy one out of the money call (with a higher strike price)

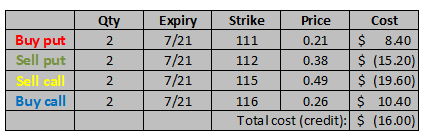

Let's assumed for the aforementioned PepsiCo that we bought two sets of contracts at the following prices:

-

Shorted the July 21st 112 puts for proceeds of 38 cents per contract,

Shorted the July 21st 112 puts for proceeds of 38 cents per contract,

- Bought the July 21st 111 puts at a cost of 21 cents per contract,

- Shorted the July 21st 115 calls for proceeds of 49 cents per contract, and

- Bought the July 21st 116 calls at a cost of 26 cents per contract.

The total net credit to take on all four legs of the position is 0.80, or $8.00 for all four legs. But, since we're buying (well, selling) two sets of the four-legged trade, we're actually putting $16.00 in our pocket upfront. This amount represents our maximum potential gain on the trade. From here, we just want to hold on as long as we can and let time -- or time decay -- whittle down the value of all four options. That's when we can lay claim to the full proceeds from the net-selling of the four pieces of the trade. Until then, it's possible that either of the short trades could be exercised against us.

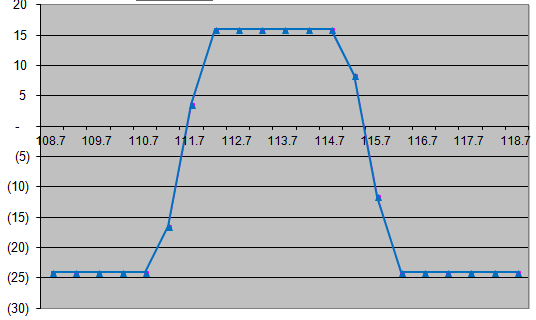

It's the shape of the profit-and-loss chart where the iron condor trade gets its name. Take a look at the graphic below. This is what are profit and loss scenario would look like two weeks from now, at expiration. (The slope of the lines would change a little bit each day between now and then.) The "iron condor" moniker derives its name from the shape of the P&L chart, which some say looks like a condor's wings were the condor made of iron. [Yes, it's a stretch to come up with that name based on the shape of the chart.] Anything between $112 and $115 means we get to keep all of our initial $16 in proceeds. Anything below $111 or above $116 translates into a $24 loss -- our maximum loss -- as we'd have to spend $24 to reverse all the contracts we initially traded. Anything between $111 and $112 and between $115 and $116 would mean varying degrees of profits or losses. It wouldn't matter if PEP was above $116 or below $111... our cost to reverse the trade would be $24 (or $12 per set of contracts) either way.

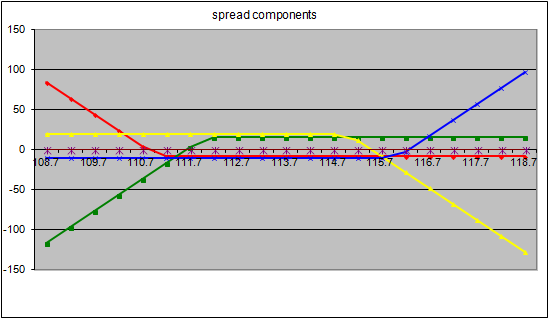

Just to put this in a little bit different, and more philosophical context, let's look at the P&L for each individual piece of spread. They're color-coded (see the table above for the colors linked to each part of the graph) below. It's from this view we can see that the ultimate intent is to lose money on at least two of the contracts, and lose money on the other two. We don't necessarily know which two of the four will be profitable and which will be unprofitable, nor do we care. We'll make some money as long as the PEP shares remain between $112 and $115.

It's this multi-legged P&L image that really drives home the key idea of spreads -- the goal is to make more money on the winning piece(s) of the trade than you lose on the losing piece(s) of the trade. The losing legs are simply insurance policies.

If you think this looks like the combination of two credit spreads, you're right. Unlike a mere one-sided credit spread though, iron condors are only profitable if the stock doesn't move. A put credit spread is a "neutral to bullish" strategy, while a call credit spread is "neutral to bearish." Iron condors are only profitable if the underlying stock or index stays put.

Does the whole thing still seem overwhelming? Don't sweat it. Iron condors aren't all that intuitive, and it may take a few "practice" trades on paper to get a feel for how they work.

If you want to learn faster from the experts, a couple of the BigTrends advisory services utilize iron condor trades when appropriate. You could become a member and "earn while you learn" how to use the strategy from Price Headley himself. Call today for more details.