Wall Street’s ‘fear gauge’ is falling, bonds and the stock market are soaring—something’s gotta give

The stock market and bonds are climbing together and that odd dynamic has investors uneasy

Curious moves in asset prices are raising eyebrows on Wall Street.

Of particular note is the sustained and simultaneous rally in government bonds and stocks. Meanwhile, Wall Street’s “fear gauge” just touched a 10-year low, as other measures of market volatility hover at the lowest levels in decades.

What gives?

It is hard to say but the market’s recent moves have been offering mixed signals about the outlook for the economy, raising questions about the ability of the run-ups in stocks and bonds to persist.

Perhaps the odd correlation between stock and bond prices has drawn the most attention.

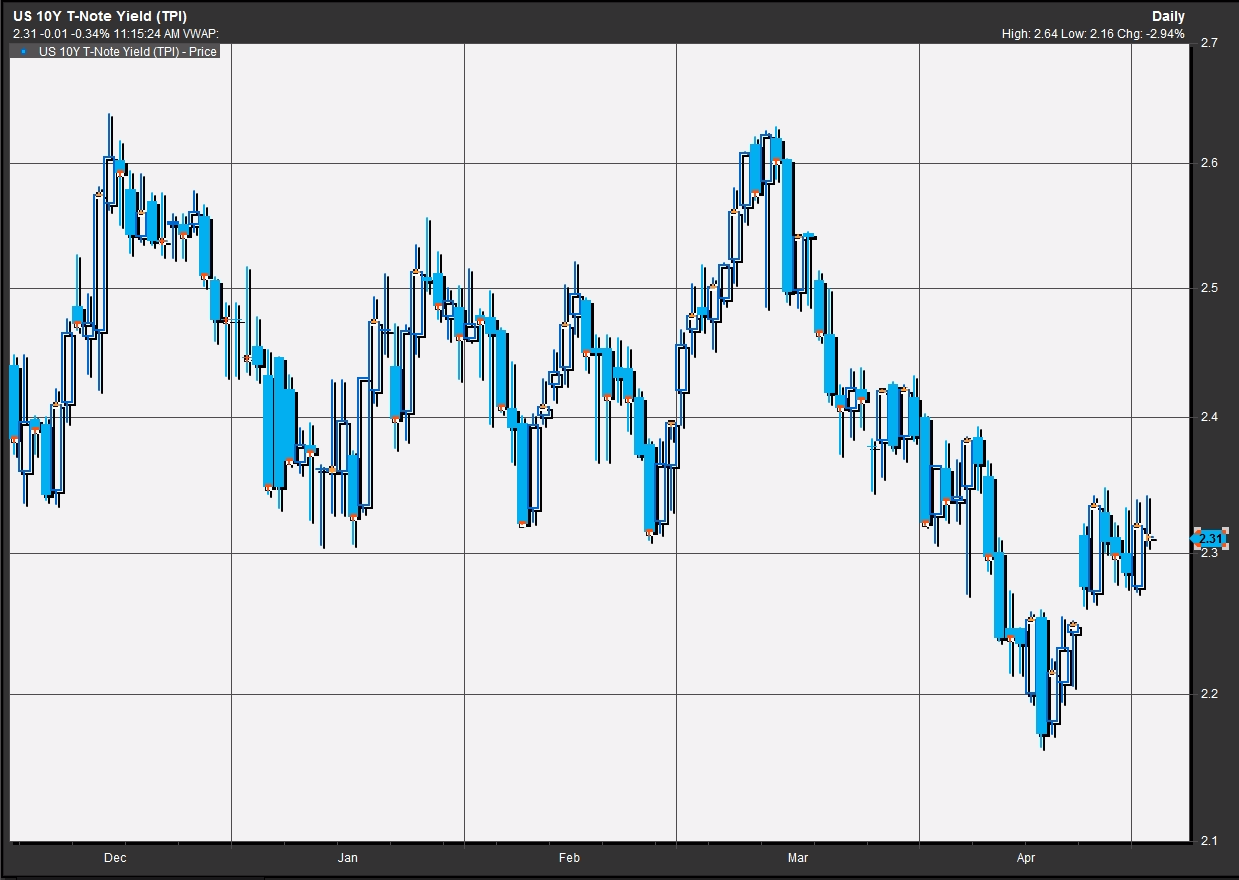

Typically, assets considered risky like stocks shouldn’t climb at the same time as havens like Treasurys are being bid higher. But that is exactly what has happened in recent trade. The 10-year Treasury benchmark, for example, is offering a yield of 2.29%, just off a recent low of 2.17% hit April 18, according to FactSet data. That implies that investors continue to scoop up bonds, pushing yields, which move inversely to prices, lower.

Moreover, those moves come as the Federal Reserve has been on a path toward normalizing interest-rate policy and shrinking its balance sheet, which should result in higher yields.

On its face, lower yields suggests that bond investors have been bearish on the U.S. economic outlook or are anxious about geopolitical tensions—or both.

Source: FactSet

Meanwhile, equity markets are rallying, with the Nasdaq Composite Index finished at a fresh record on Tuesday (see chart below), while the S&P 500 index is off about 0.2% from its all-time closing high hit March 1 and the Dow Jones Industrial Average is less than a 1% shy off its own record close.

“So far, these moves seem to be pressing against common wisdom,” said Boris Schlossberg, managing director at BK Asset Management.

Schlossberg said part of the divergent narrative is that stock investors are still holding out hope that President Donald Trump will make good on promises to cut taxes, along with delivering on a host of other Wall Street-friendly pledges.

Bond investors, however, have been keying in on other factors, including weakness in recent economic reports. A preliminary reading of first-quarter gross domestic product, the official scorecard for the U.S. economy, showed the slowest pace of growth in three years. Rising geopolitical tensions between the U.S. and North Korea and concerns about elections in France that have threatened to disrupt the global markets, have kept Treasury yields low but hasn’t rattled the resolve of equity investors.

And bond investors appear to have growing doubts about Trump’s ability to implement his legislative agenda. That’s a shift from the postelection environment, when expectations Trump’s policies would spur growth, inflation—and larger budget deficits—pushed the benchmark 10-year yield to a peak of 2.62% mid- December.

“Hope springs eternal and there’s an enormous amount of built-in optimism around a massive tax stimulus, fiscal stimulus or both. If Trump produces neither that is going to be a serious shock to the market,” Schlossberg said.

VIX

That said, the markets don’t appear to be worried about much. Wall Street’s :fear gauge,” the CBOE Volatility Index VIX, +4.72% touched its lowest reading in a decade on Monday, falling to 10.11, and briefly hit single digits. The VIX is a measure of the market’s expectations for volatility 30-days in the future, and is based on options on the S&P 500 index. The gauge usually moves in the opposite direction of the S&P and at around 10 it is far from its historic average of 20, suggesting that investors aren’t making big bets on equity prices tumbling soon.

Nicholas Colas, chief market strategist at New York-based global brokerage Convergex, said the VIX is flirting with levels that bode ill for stock bulls. He said when the VIX closes “below 10 [it is] is historically correlated with a one-year pause in S&P 500 returns.”

Jeffrey Saut, chief investment strategist at Raymond James, in a Tuesday note, said the retreat in the VIX coincided with France’s presidential election, which saw centrist Emmanuel Macron decisively come out on top in the first round on April 23, putting him in pole position heading into the Sunday runoff against far-right candidate Marine Le Pen, who has threatened to drag the country out of the European Union.

Saut writes that an “’upside leg’ [for equities] has begun with the French pre-election results where Macron (the internationalist) looks to be the next French president!”

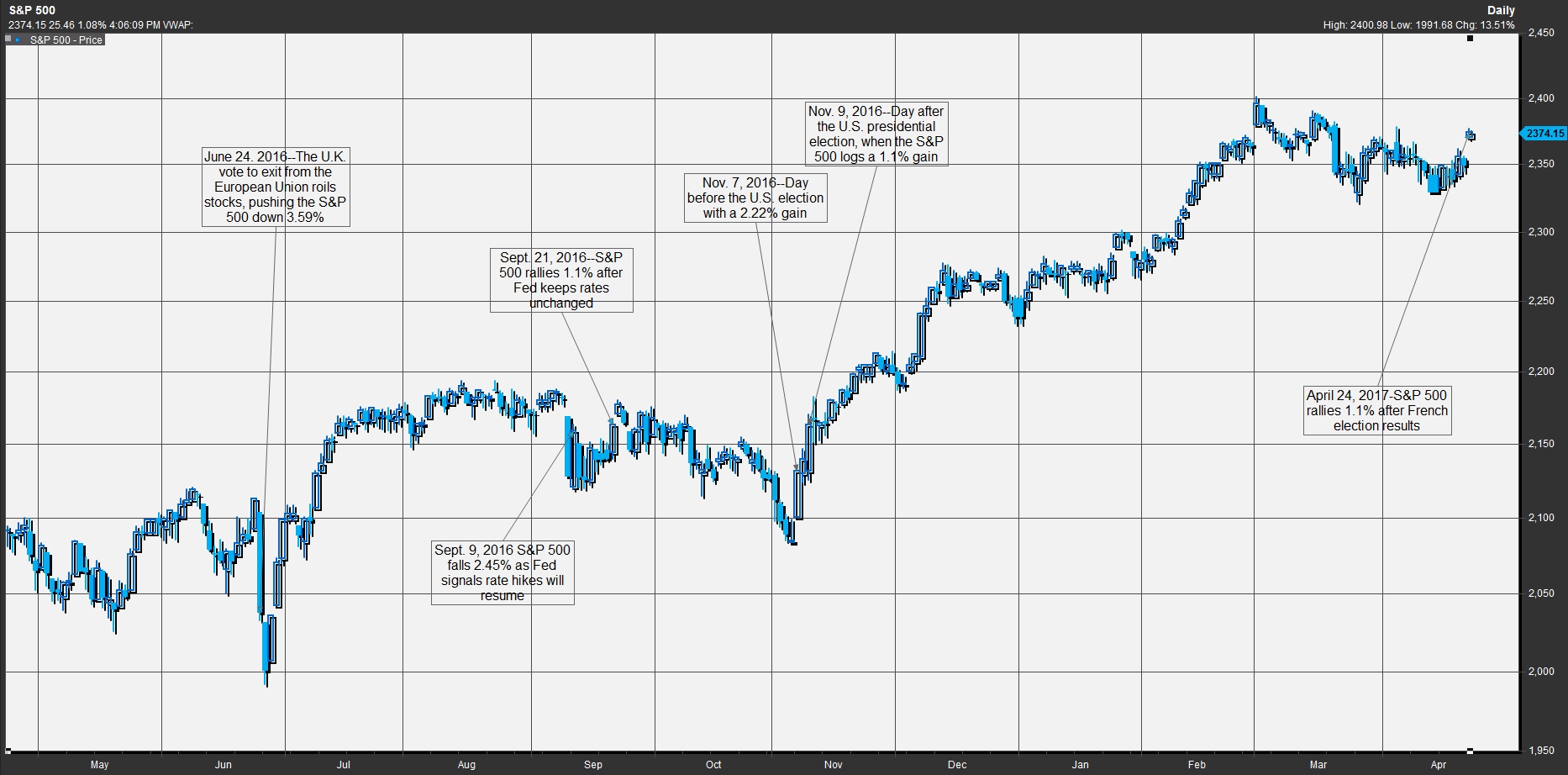

Indeed, elections and referendums have been among the most significant catalysts of market swings of at least 1% over the past year, (see chart below, which shows the S&P 500’s reactions to recent elections and Fed announcements):

Source: FactSet, MarketWatch

Volatility

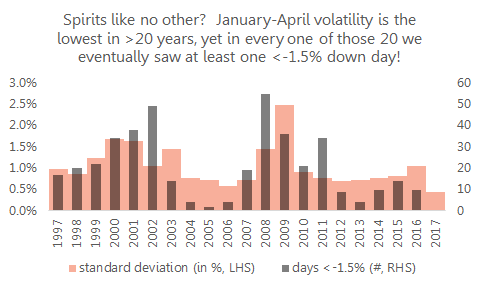

Another uncanny element of the market’s recent ascent has been its inexplicable buoyancy. Salil Mehta, a statistician and a former director of analytics for the Treasury Department’s TARP program, says the standard deviation for the S&P 500 index from January to April is at its lowest in 20 years (see chart below).

Source :Salil Mehta

The S&P 500’s standard deviation has been roughly 0.4% on average, as of April 28. Mehta says that equates to a VIX of about 8.

Mehta makes the logical case that what goes up must come down, and that with such a protracted period of calm that when the market does slump it will likely be particularly spectacular.

Here are few other statistics Mehta offers up on the length of time since the S&P 500 saw significant drops of varying intensity:

- 1.5% or worse (160 days ago, average is 22 days)

- 2% or worse (160 days ago, average is 47 days)

- 5% or worse (1,441 days ago, average is 706 days)

- 10% or worse (7,443 days ago, average is 16940 days)

“Now is not the time to believe markets will continue to unrelentingly rise,” he said.

Looking ahead, Peter Boockvar, managing director at the Lindsey Group, said he thinks that the Fed’s monetary policy will offset any benefits from the expected Trump stimulus program, should they become a reality. He sees the Fed raising rates at more rapid pace if the economy starts to heat up.

“I don’t know why people think everything is going to change just because we get some tax cuts,” he said.

Courtesy of MarketWatch