Five important reasons why a stampede into stocks may be just getting started

- Synchronized global growth further boosts the case for strong U.S. gains -

Success breeds success and strength begets more strength—that will likely be the overriding theme for stocks going forward as strong fundamentals, positive sentiment and favorable seasonality keep an already pumped-up market on a steady adrenaline rush.

All major indexes closed at records this week with the Dow Jones Industrial Average and the S&P 500 logging eight straight weekly gains, the longest for both since November 2013. The Nasdaq also notched its 63rd closing record in 2017, the most ever in a single year, according to the WSJ Market Data Group.

Ian Winer, head of equities at Wedbush, said it was technically a very bullish week, particularly for the Dow, which tested new highs almost every day.

Now a potent mix of looming tax cuts along with robust earnings may be setting stocks up for what could be a truly spectacular finale to a memorable year.

1. “I’m just a bill, yes, I’m only a bill”:

The Republicans on Thursday unveiled their ambitious tax package, which proposes lowering the corporate tax rate to 20%, a one-time tax break on repatriation of profits parked overseas, and a revision of the individual tax brackets.

Experts say the outcome of tax reforms remains uncertain given the level of resistance among interest groups and the disarray within the Republican party. However, they were cautiously optimistic that the tax bill will result in some economic stimulus when it eventually passes.

Bricklin Dwyer, senior economist for U.S. and Canada at BNP Paribas, projected the tax plan could ultimately pave the way for fiscal stimulus that could add as much as 0.6 percentage point to 2018 gross domestic product growth.

Meanwhile, Joseph Song, U.S. economist at Bank of America Merrill Lynch, predicted that there will be no fiscal stimulus given that the tax bill will not pass in its current form.

“The biggest constraint for Congress is the price tag. Reconciliation directives only allow Congress to add up to $1.5 trillion to the deficit over 10 years. If the bill cost more than that, it will run afoul of the Senate reconciliation rules,” said Song in a report.

The economist expects significant opposition to the bill from moderate Republicans and deficit hawks.

“We remain skeptical that a comprehensive tax plan will pass Congress but it is possible that a pared down version passes sometime early next year. Our baseline forecast currently assumes no fiscal stimulus but there is an upside risk that a small plan is enacted which would provide a modest boost,” he said.

Lewis Alexander, chief U.S. economist at Nomura, believes there is a 60% probability of a simple tax package passing, 20% chance of a full-scale reform, and 20% likelihood of the tax bill failing to pass.

2. Summer blockbuster:

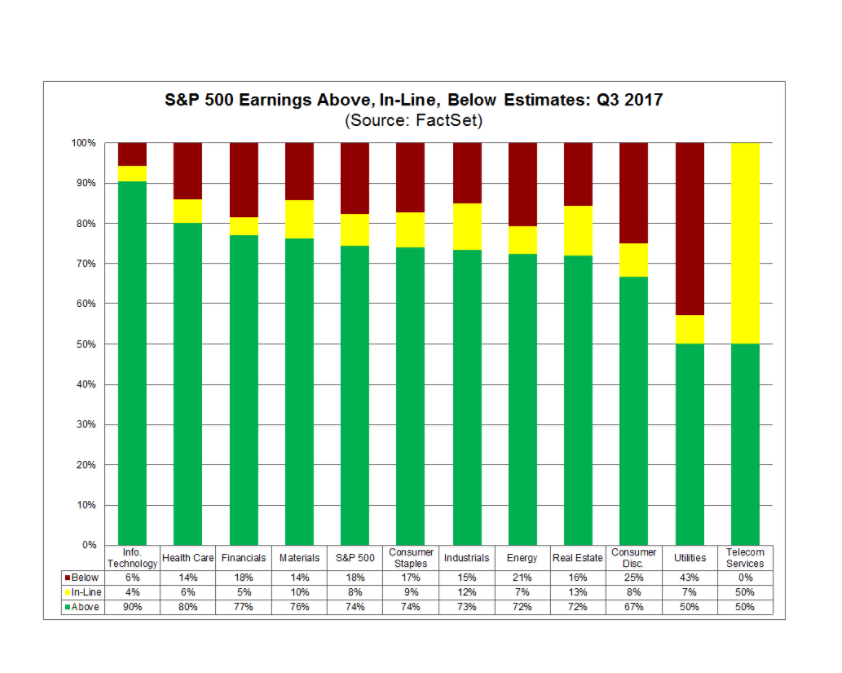

It has been a blowout quarter for earnings, with companies reporting profits that are 4.8% better than estimates and sales 1.2% above estimates, according to latest data from FactSet.

As of late October, S&P 500 earnings are up by 4.7% with six of the 11 sectors turning in higher profits. Some 76% of companies are posting better-than-expected results, ahead of the one-year (71%) and the five-year (69%) averages, said Brad McMillan, chief investment officer for Commonwealth Financial Network.

S&P 500 revenues are also up 5.7% with 10 of the 11 sectors reporting higher sales, he said.

3. Timing is everything:

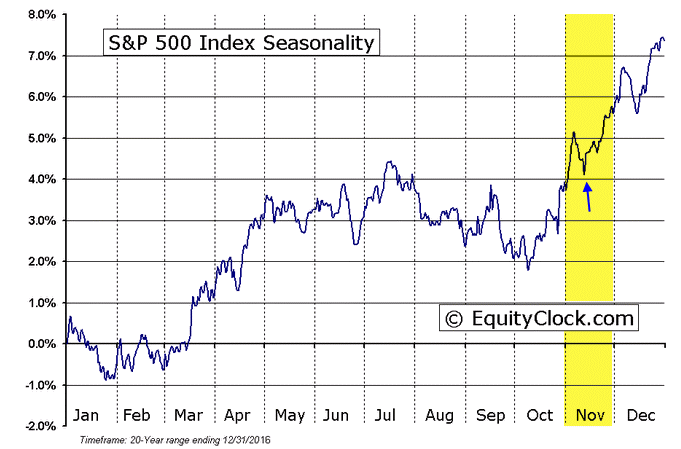

Stocks are heading into the strongest couple of months of the year, particularly for the S&P 500.

According to Frank Cappelleri, a technical strategist at Instinet LLC, the S&P 500 has been higher in November 60% of the time for an average gain of 0.67% going back as far as 1928, while in the past two decades, the large-cap index been higher 15 out of 20 Novembers with an average rise of 1.5%.

“Difficulty is one thing that the SPX has not witnessed in 2017,” said Cappelleri, who pointed out that the S&P 500 has risen for each month of the typically weak period spanning May to October.

4. Scale tips in favor of bulls:

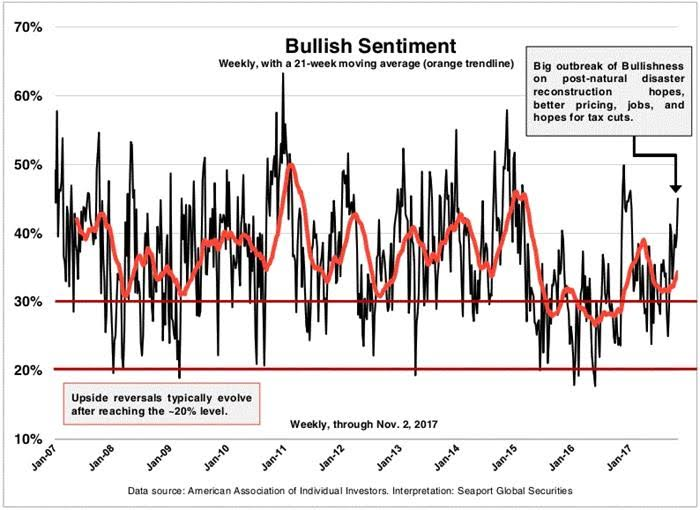

Richard Hastings, macro strategist at Seaport Global, noted that aside from bullish sentiment, which soared to 45% in a recent American Association of Individual Investors survey, other positive developments such as job growth, hopes for tax cuts, and higher crude-oil prices are coming into focus.

“This is a very constructive situation for the big picture investment story. We could be going into a brief period of piling up, where sentiment ignores valuation and sticks to momentum. The FANG [Facebook, Amazon, Netflix and Alphabet’s Google] rebound in recent days is probably a great big ‘We Are Open’ sign to investors,” he said.

The persistently buoyant sentiment “engineers” volatility and inefficiency out of the market and helps to shield stocks from frequent corrections, according to Hastings.

The Bank of America Merrill Lynch’s Sell Side Indicator—the bank’s barometer for Wall Street’s bullishness on stocks—also edged up to 55.9, hovering near its highest level since 2011.

5. It’s a small world after all:

One of the most interesting traits about the current stock market’s epic run is that it’s not just the U.S. setting the world on fire but a concerted international effort.

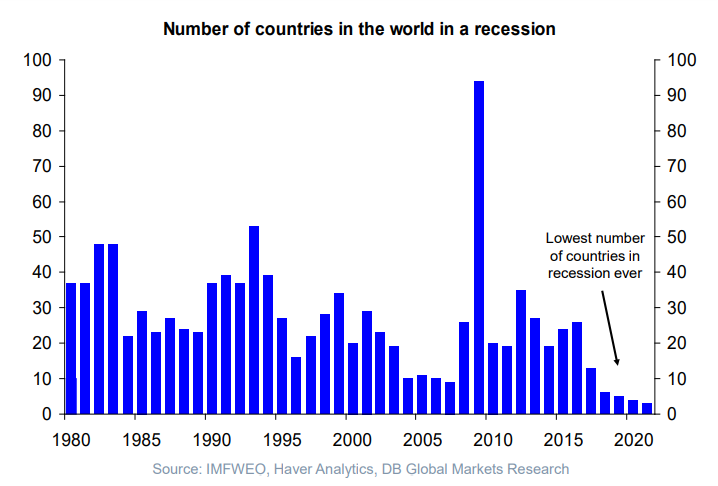

As Jeffrey Saut, chief investment strategist at Raymond James, highlighted in his report, with major countries in synchronized expansion mode, global growth is projected to reach 3.6% in 2017 and 3.7% in 2018, the best since the Great Recession.

Torsten Slok, chief international economist at Deutsche Bank Securities, this week also shared the chart above that showed that the number of countries in a recession at a historic low, a clear sign that global economy is booming.

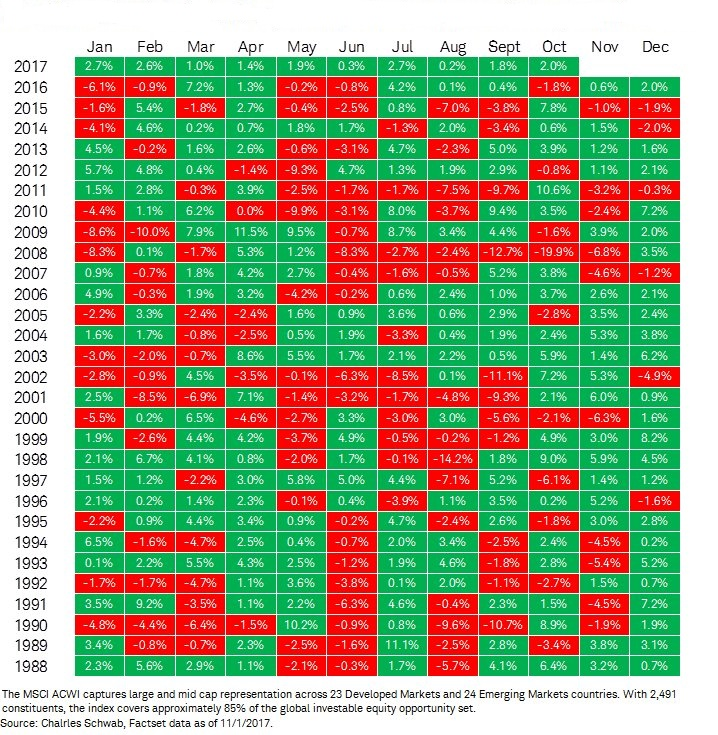

This uniform expansion has helped to spark a global rally in equities with the MSCI All Country World Index gaining for a record 12 straight months.

The previous longest streak was 11 months that ended in February 2004 following a drop of 50%, according to Jeffrey Kleintop, chief global investment strategist at Charles Schwab & Co.

From MarketWatch