It was an ugly gain, with the week's net progress all confined to Wednesday's big post-Fed-announcement surge. But, a win is a win. The S&P 500's 0.2% gain was almost imperceptible, but it's better than the alternative. Last week's gain quelled a downtrend before it got started with the small loss from two weeks ago.

Nevertheless, there's no denying stocks are hitting a headwind here. It would be wise to prepare for the worst even as you're hoping for the best.

We'll analyze and scrutinize all of it below. First, though, let's run down last week's major economic news and preview this week's big economic announcements. We've yet to see the defining economic victory that says the economy is fully rekindled.

Economic Data

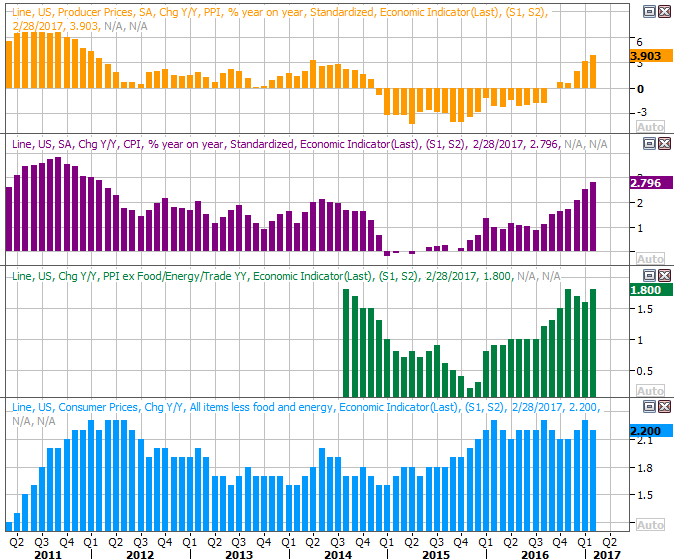

There's a mountain of economic data news from last week to sift through. We'll stick with the highlights, starting with the first big news we saw for the week... February's inflation report. Although the month-to-month numbers showed a cooling of the pace seen in January, they were still up, and the more important year-over-year comparisons continue to move to uncomfortable levels. Producers are dealing with inflation of 3.9% now, and even stripping out the rising costs of food and gas, our factories and plants are seeing costs up 1.8% year-over-year. Consumers are feeling the pinch too. Their prices are up 2.8% versus year-ago levels, and even on a core basis consumer inflation is up 2.2% now.

Producer and Consumer Inflation (Annualized) Charts

Source: Thomson Reuters

That, of course, was a big part of the reason the Federal Reserve chose to put the widely expected 1/4 point interest rate hike in place last week. What was unexpected was her still-dovish plan to keep the next two planned hikes for the year (though three more are still possible, some say) spaced out and as delayed as possible. That threw the overzealous hawks for a loop, and sent the U.S. dollar into a steep -- though not surprising -- dive.

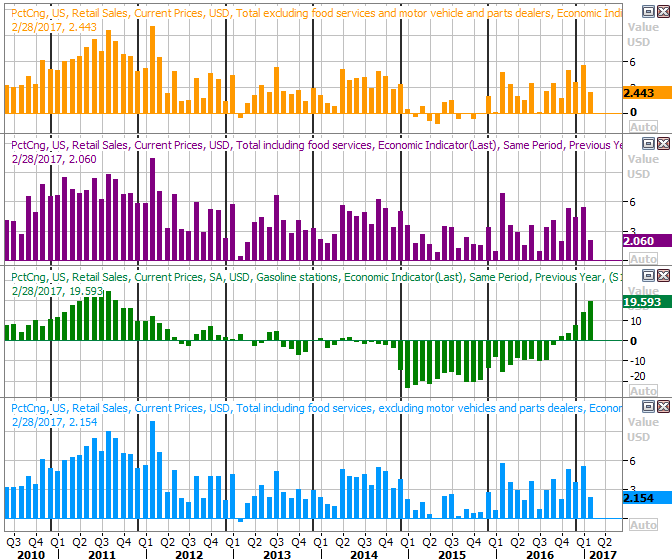

We also heard last month's retail sales growth figures. They were good. Thought the pace of year-over-year progress slowed, the comparisons were much tougher last month then they had been through January. (This is the new normal... but it's still healthy.)

Retail Sales Growth (Annualized) Charts

Source: Thomson Reuters

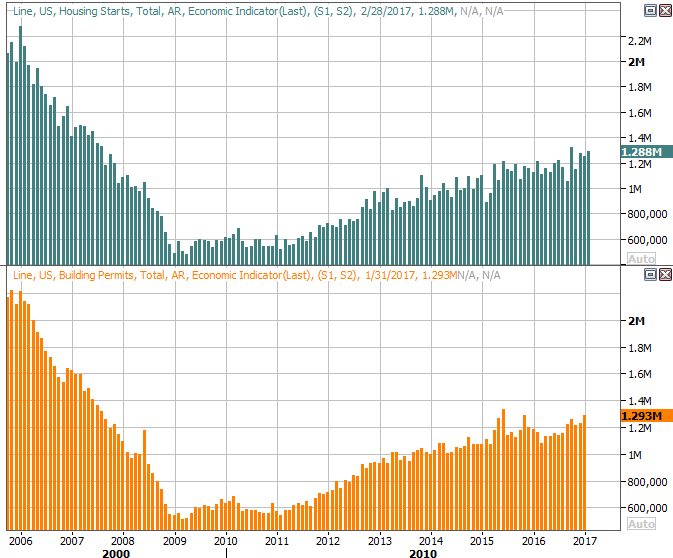

It was also an important week for real estate data... the first of a two-week stretch that really paints a picture of where real estate is. Last week's data was housing starts and building permits, and they were... ok. Starts were a little stronger than expected, and permits were a little shy of forecasts. Both are still trending higher though.

Housing Starts and Building Permits Charts

Source: Thomson Reuters

This week we'll get February's new-home sales and existing-home sales, rounding out the real estate picture, along with some home-price index data for January. The pros aren't expecting any great progress on these fronts either. This lethargy is a concern, though until we're going backwards, we can't be too worried.

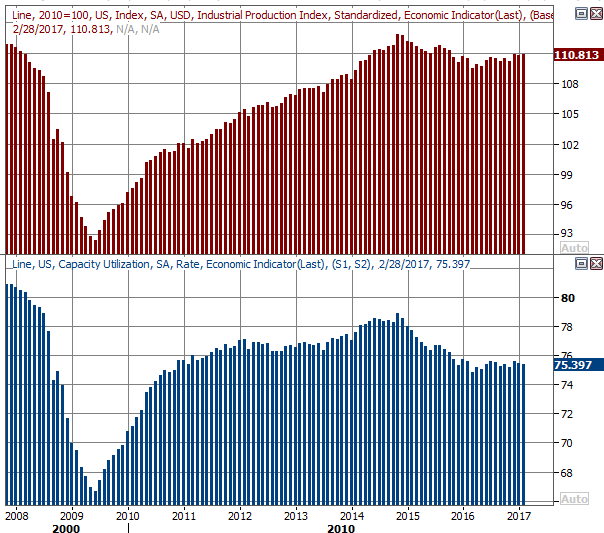

Finally, though it largely went undiscussed, last month's industrial productivity and capacity utilization data was unimpressive. Productivity was flat, and capacity utilization slumped ten basis points. In light of all the stock market has done (and Trump has said) since November, one would have expected to see more convincing evidence of economic expansion. And, it would show up on these charts if that was the case.

Industrial Productivity and Capacity Utilization Charts

Source: Thomson Reuters

Everything else is on the grid.

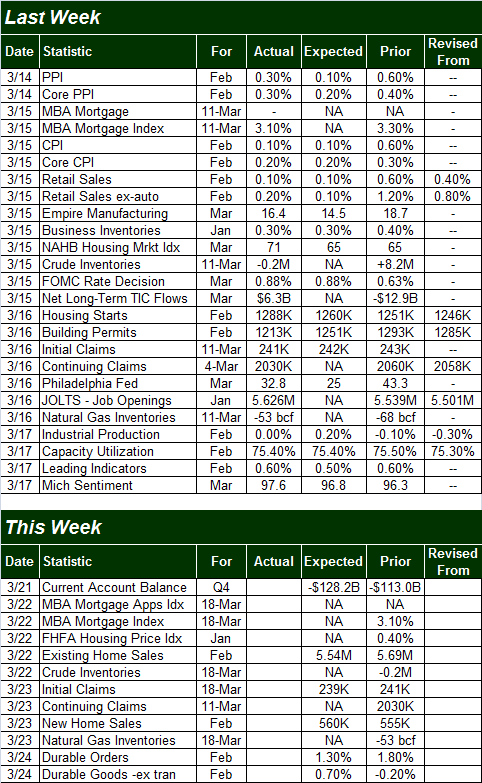

Economic Calendar

Source: Briefing.com

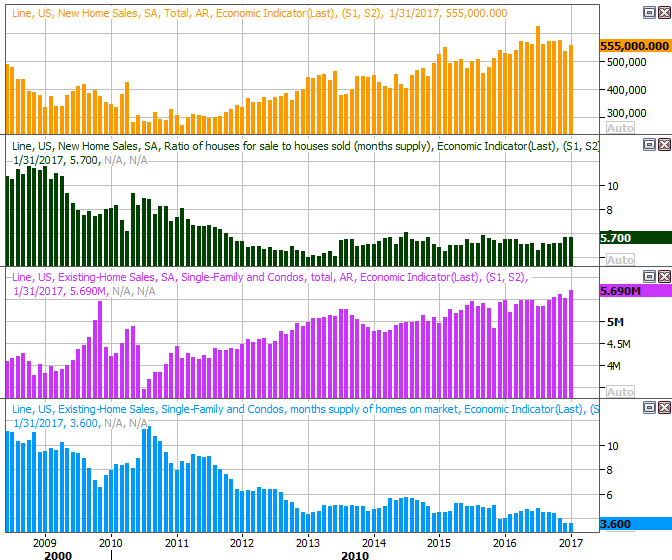

This week is going to be fairly light. In fact, the only item we're interested in is the aforementioned new-home sales and existing-home sales. Don't look for anything too impressive. As the chart below illustrates, while new home sales are slowing, that's being offset by ongoing growth in existing home sales. The irony? Existing home sales are growing despite a lack of inventory, and inventory of new homes is starting to build... but they're not selling all that well.

New and Existing Home Sales Charts

Source: Thomson Reuters

Index Analysis

The weight of the runup since early November is starting to show, and matter. Though stocks eked out a gain last week, there's no denying the market was straining to do so. And, if there was ever a good place for the bears to make a stand, this is it.

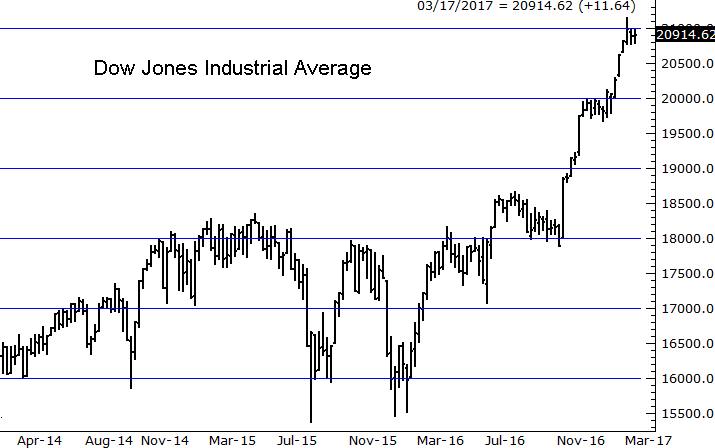

The basis for that theory is evident on a chart we rarely look at... the weekly chart of the Dow Jones Industrial Average. It's on this graph we can see that the 21,000 level -- a big round number -- has capped the rally from the blue-chip index.

Dow Jones Industrial Average Weekly Chart

Chart created with TradeStation

If the stall hadn't been so precise, and if the battle at the 20,000 mark (and all the other XX,000 levels) also hadn't been crystal clear, it may not be worth mentioning. There's something about this though. Traders may simply be following the script they - subconsciously - think they're supposed to follow.

The S&P 500's daily chart also waves a couple of red flags, not the least of which is that after Wednesday's big move higher, it spent the last two days of the week back-pedaling. It didn't take long for the bulls to close their pocketbooks following the rate hikes. Not only did the index fail to move to a new high, the upper Bollinger band seems to have played a rally in the flame-out.

S&P 500 Daily Chart

Chart created with TradeStation

That being said, take Friday (and Thursday, for that matter) with a grain of salt. See, it was a quadruple-witching day, which can wreak havoc on the market.

A quadruple witching is when a great number of equity and index options as well as a big number futures all expire, forcing traders to either use them or let them expire... worthless. Many traders also roll these traders over to a later expiration day. All of it, however, can have an effect on the market. It usually has the effect of keeping the market contained rather than pushing it decidedly higher or lower. That's a big part of the reason the VIX went so much lower and the total trade volume soared on Friday.

It's also a big part of the reason we can't take anything we saw late last week to heart - it doesn't really tell us anything about the market's undertow. We're still working off the same analysis and assumptions we were working off of a week ago. That is, for a breakdown to become real, the S&P 500 is going to have to break below the floor at 2353, and the VIX will have to break above 12.9. Anything less, and it's just a little volatility. We don't see the Dow making a run on 22,000 anytime soon.