The Dollar Just Plunged, and Didn't Look Back. Now What?

On Tuesday, we pointed out how the U.S. dollar -- using the U.S. Dollar Index as our proxy -- was in serious trouble. Though it was still on the high side of its absolute scale, it was teetering on the verge of a break under key support levels.

It broke under that floor in rather decisive fashion since them. Today's close of 95.71, thanks to the three-day rout, has pulled the greenback into new multi-month low territory.

As before, the weekly chart of the U.S. Dollar Index puts things in more perspective. It's also on the weekly chart we can see how important the 93.1 level is. If the dollar doesn't stop falling there, there's no telling where it may finally find a floor.

The prod for the dollar's weakness of late actually isn't about the dollar itself. Rather, it's about every other major currency. Many other central banks are now voicing a hawkish rhetoric, suggesting they'll ratchet up their interest rates at a faster pace than the United States Federal Reserve has indicated it will inflate ours. Those relatively higher interest rates make U.S. bonds and therefore U.S. currency seem worth less.

There's more psychology than actual causality in the premise, but that doesn't prevent investors from acting on the idea all the same. Indeed, it may be just the excuse needed for traders to unwind net-bullish trades that sent the greenback soaring in 2014 and 2015 for no particularly good reason.

The impact of a weaker dollar isn't all bad. In fact, in the current scenario, there's far greater upside for the U.S. economy and its investors than not. A strong dollar has led to stiflingly-low oil prices, and made it tough for U.S. companies to sell their goods overseas. If the energy sector can restore reasonable profit levels and multi-national enterprises win back some business lost to foreign competition, net-earnings for the broad stand to improve significantly.

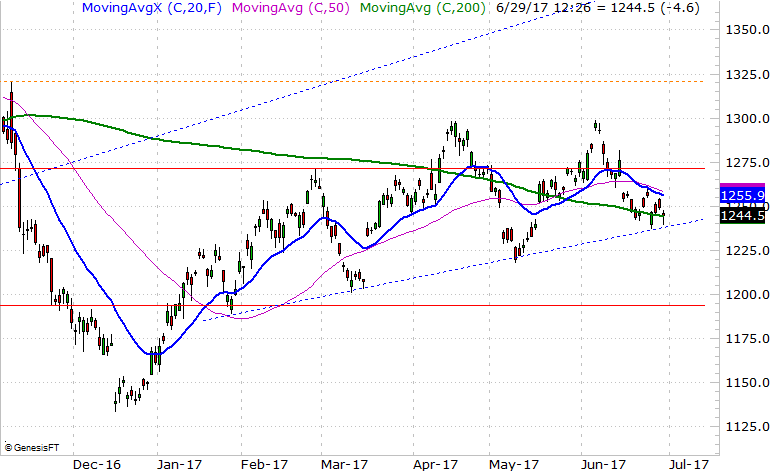

It hasn't helped oil a great deal yet. Though crude prices have bounced over the course of the past few days when the dollar's selloff gained some steam, oil prices haven't risen in step with the dollar's demise since late last year. For as much good as the falling greenback has done, persistently-high oil inventory levels have proven to be an even bigger, adverse force.

Still, this is a start for oil prices.

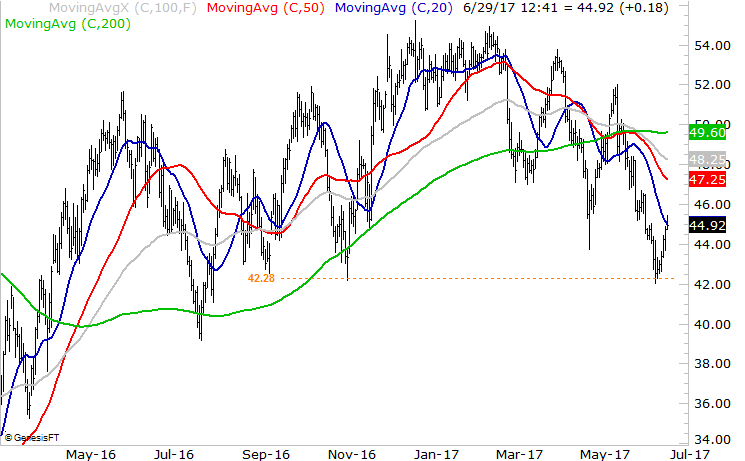

As little as crude prices have perked up relative to the U.S. dollar's selloff since January, gold has been even more -- and surprisingly so --disappoint. A lack of inflationary pressure and/or economic volatility has largely quelled any perceived need for gold's inherent defensiveness.

That said, that may be about to change too. The recent lull from gold has pulled it back to a fairly well established rising support line, and so far, the bulls appear willing to use it as a launchpad. That launch hasn't happened yet, but the selling effort has clearly abated.

A little more downside for the dollar could very well put gold and oil into a higher bullish gear. If the U.S. dollar ends up sliding all the way to the aforementioned 93.1 level, that could end up marking the beginning of a more fundamentally-based shift that makes a measurable impact on earnings... for the better.