Opinion: What’s Better for Stocks: a Strong or a Weak Dollar?

President Trump isn’t the only one who’s confused.

Donald Trump isn’t the only one confused about whether we should prefer a stronger or weaker dollar.

Almost all investors are too.

Fortunately, however, you don’t have to call the national security adviser at 3 a.m. to find out.

That’s because I am going to give you the answer in this column:

Neither.

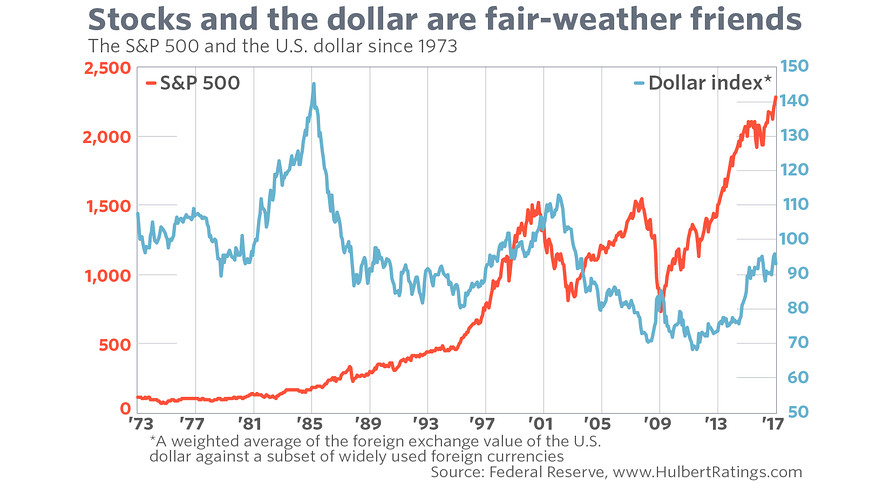

The S&P 500 index (SPX) sometimes has risen in the wake of a strengthening dollar DXY, +0.24% and at other times has fallen. And this is exactly what we should expect, according to Campbell Harvey, a finance professor at Duke University’s Fuqua School of Business. The relationship between equities and the dollar, he told me in an interview, is not a simple cause-and-effect relationship.

Even when it might look like a strong or weak dollar is having a positive or negative effect on stock prices, he explained, it’s most likely that something else is impacting both. For example, a strengthening economy could very well lead to both a stronger dollar and a higher stock market. But then it’s the economy that is the cause of higher stock prices, not the dollar.

The investment implication is clear: Don’t base your stock-market forecast on your outlook for the dollar.

Does this advice apply to individual companies as well? Might it be the case that certain firms will be hurt by a stronger dollar, for example?

In theory the answer is yes, though even here the cause-and-effect relationship is anything but straightforward. It could very well be, as companies often claim when trying to excuse poorer-than-expected earnings, that the stronger dollar reduces the dollar value of their foreign sales. But what those companies never tell you is how many of their costs of production are also non-dollar-denominated—costs that will be reduced because of the stronger dollar.

Furthermore, as Harvey points out, a company’s currency-hedging operations could very well eliminate some or all of the positive or negative impacts that the dollar’s fluctuations otherwise would have. Even if a company divulges the extent of its currency hedging operations, it still can be difficult in advance to determine what the net effect of those operations will be.

None of this means that the dollar’s foreign-exchange value isn’t important, or that you shouldn’t care about it as a matter of general public policy. But when it comes to your stock portfolio, there are many more important factors on which it is better to focus.

Courtesy of MarketWatch