Weekly Market Outlook – Room (and Reason) To Keep Running

Stocks didn’t exactly end the week on a high note. But, the gains logged on Monday were enough to set up what was a sixth consecutive winning week. The S&P 500 even notched a new record high, with more room to keep running.

As unlikely as it should be from here, the current trend is bullish. Let’s assume it will remain that way until it clearly isn’t.

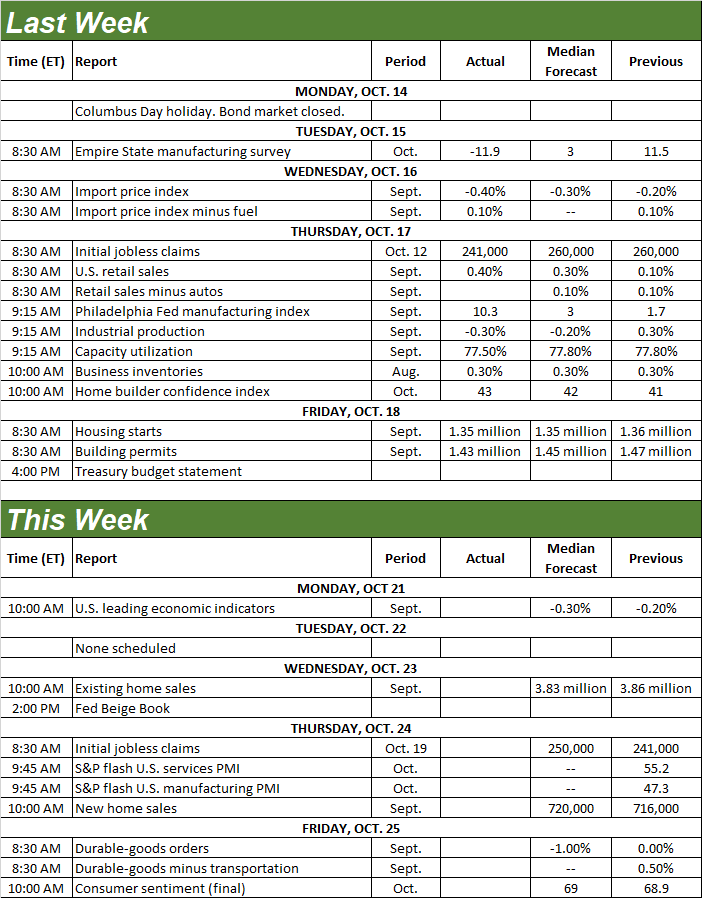

We’ll take a detailed look in a moment below. Let’s first look at last week’s most important economic news, and preview what’s in the lineup for this week.

Economic Data Analysis

Big week, with most of it being crammed into the final two days of the five.

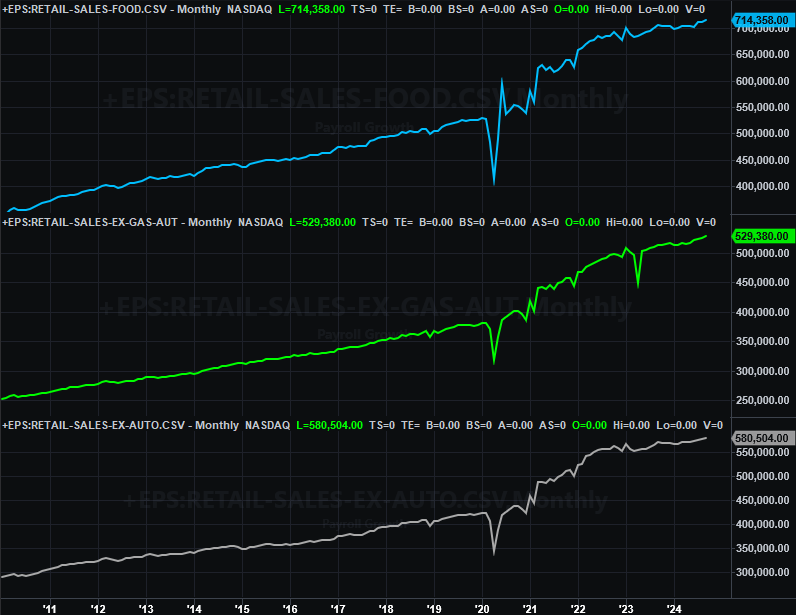

One of Thursday’s biggies was a look at last month’s retail spending. It was up, and mostly by more than expected. Although still relatively shallow, it does appear that consumers’ spending is starting to accelerate again as inflation levels off and income remains (mostly) stable. We’ll take it.

Retail Sales Charts

Source: U.S. Census Bureau, TradeStation

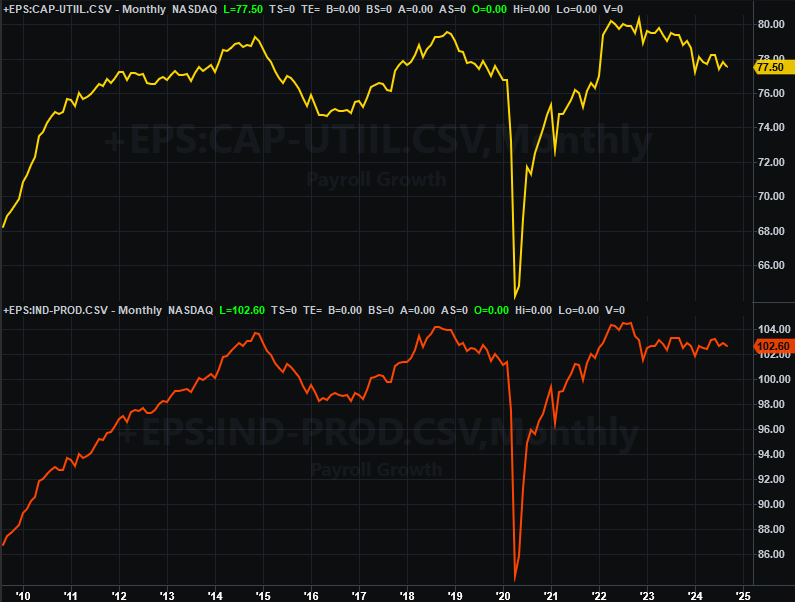

The Federal Reserve also served up an update on the nation’s factory activity. And, it wasn’t great. As expected, industrial production reversed August’s progress, while utilization of the nation’s production capacity fell a bit from August’s levels. In both cases, the bigger-picture trend is a weakening one. This is a concern. Corporate earnings tend to move in tandem with this data. Right now they’re not, but there’s got to be a convergence one way or another sooner or later. These trajectories are a concern.

Capacity Utilization, Industrial Productivity Charts

Source: Federal Reserve, TradeStation

Finally, housing starts and building permits for September were posted on Friday. They were down slightly from August’s numbers, deflating budding hopes that demand for homes would be renewed by lower interest rates. It might be a bit too soon to expect this prospective interest to be rekindled by cheaper borrowing costs. But, we’d anticipate at least a glimmer of progress. Perhaps consumers and would-be homebuyers remain hesitant to commit to any major purchases, recognizing that home prices are still wildly high.

Housing Starts, Building Permits Charts

Source: U.S. Census Bureau, TradeStation

It’s also possible that the demand or capacity to start constructing new homes has been stifled by the horrific damage done in the southeastern U.S. not by one but by two devastating hurricanes. It’s equally possible people are waiting on the sidelines to see who the next President of the United States is.

Everything else is on the grid.

Economic Calendar

Source: Briefing.com

The real estate picture will be rounded out this week, with Wednesday’s look at sales of existing homes in September, and Thursday’s new-home sales report for last month. Forecasters are calling for a slight improvement in sales of new homes, offering a glimmer of hope that demand indeed still edging higher. The much-bigger existing-home sales number, however, is expected to lose a little more ground, sustaining a downtrend that has the data back near last year’s multi-year lows.

New, Existing Home Sales Charts

Source: U.S. Census Bureau, National Assn. of Realtors, TradeStation

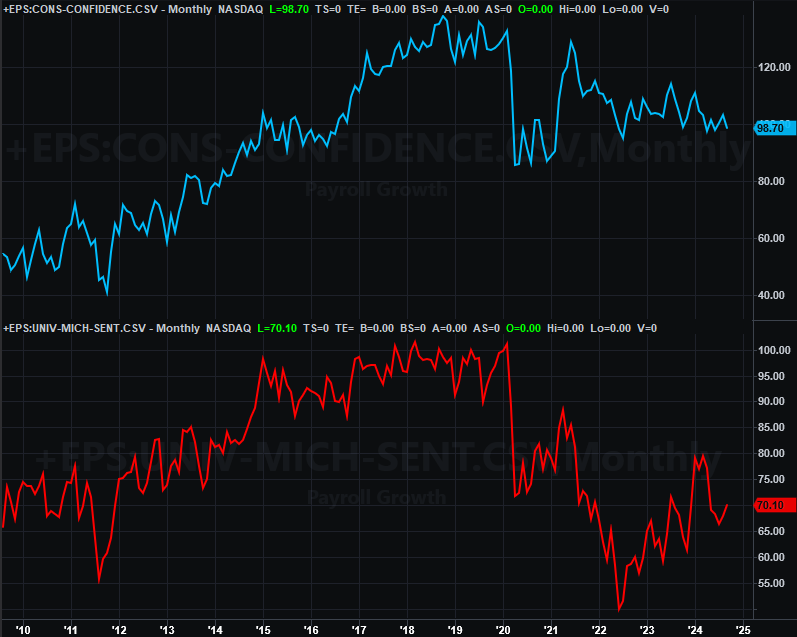

The third and final update of the University of Michigan’s consumer sentiment index for October will be given on Friday. Economists believe it will roll in lower than last month’s still-weak levels, although the longer-term trend here is still encouraging (even if that encouragement is inconsistent).

Consumer Sentiment Charts

Source: University of Michigan, Conference Board, TradeStation

The Conference Board’s measure of consumer confidence will be posted next week. Notice this data is slowly deteriorating.

Stock Market Index Analysis

The market’s been overbought and ripe for a correction for some time now. But, it continues to defy the odds, logging its sixth straight week of gains. The thing is, although the longer this bullishness persists the closer we get to a pullback, the easier it gets for the bulls to defy the odds.

That’s the long way of saying don’t assume a stumble is immediately inevitable.

Oh, there’s pitfalls ahead to be sure. As the daily chart of the NASDAQ Composite below shows us, last week’s highs connect all the key highs going back to late-July’s pre-plunge peak (green, dashed). This straight-line technical ceiling has now been touched four times without actually being hurdled.

NASDAQ Composite Daily Chart, with VXN and Volume

Source: TradeNavigator

Take a step back and look at the longer-term weekly chart of the composite though. There’s a longer-term technical ceiling (red, dashed) connecting all the even-more-major highs going back to late-2022. There’s at least another 1,500 points between where the NASDAQ is now and where that resistance is before it could be tested. Given than we just got a fresh bullish MACD crossover this past week, the arguable trend here is more bullish than bearish.

NASDAQ Composite Weekly Chart, with VIX and MACD

Source: TradeNavigator

Perhaps the strongest aspect of the current bullish argument is the fact that the NASDAQ’s volatility index (VXN) actually has some room to continue falling before finding an absolute floor near 16.

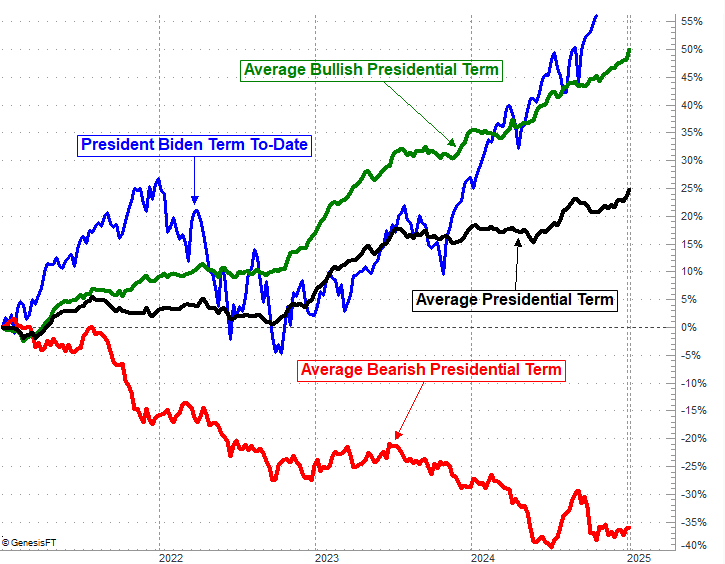

This is stunningly unusual, although less-so for the final year of any four-year Presidential term.

While the S&P 500 would normally only be up by a little less than 12% at this point in any bullish year, it’s higher 24% this time around. But, the 56% gain seen since President Biden took office is actually in-line with norms. So, it’s not crazy. It’s also possible stocks will continue higher from here, given that this is so often the case in the fourth year of any Presidential term.

S&P 500 Performance Chart, Four-Year Presidential Term

Source: TradeNavigator

And the weekly chart of the S&P 500 is telling the same basic story, although it’s closer to its most likely end than the NASDAQ is. Already at record highs, the S&P 500 is only a few points away from bumping into the technical resistance line (red, dashed) that connects a handful of key highs for the past few months. This index doesn’t have quite as much room to run as the composite does.

S&P 500 Weekly Chart, with VIX and MACD

Source: TradeNavigator

There is room to run, however… maybe around 200 points. The S&P 500’s volatility index (VIX) also has some room to continue falling.

This doesn’t mean you can rule out a pullback taking shape sooner than later. Again, none of this is really “supposed to be” happening from a perspective that ignores the calendar. Stocks are just plain overbought. There’s plenty of technical support below though (moving average lines, mostly), standing ready to push back against any selling. It’s going to take a lot of persistent damage to actually get the market moving lower in a major way. The path of least resistance remains upward until then.