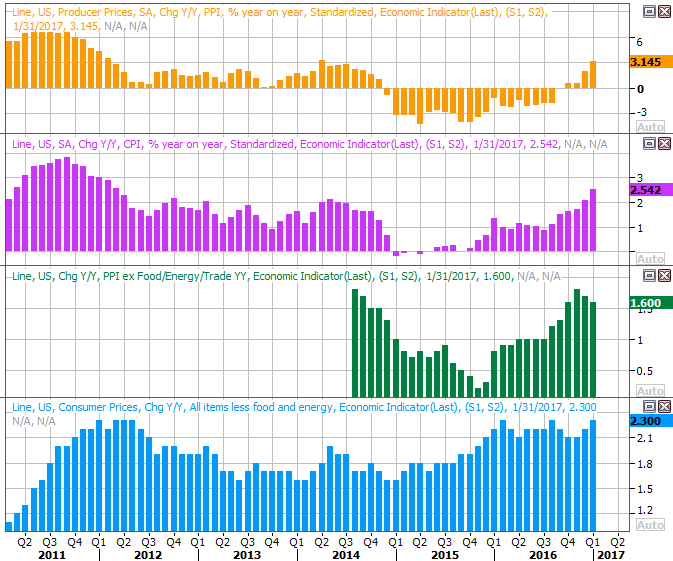

Whatever the odds of a rate-hike were before Friday, they just got better (and they were pretty good odds to begin with). February's strong jobs growth - and wage growth - make it tough for Fed Chairperson Jane to Yellen to say anything except the economy is on firm enough footing that the risk of inflation is too great to do nothing. Indeed, inflation is no longer just a risk. As of the most recent report from January, the annualized consumer inflation rate stands at a multi-year high of 2.5%, and is trending higher. The Fed's target is 2.0%.

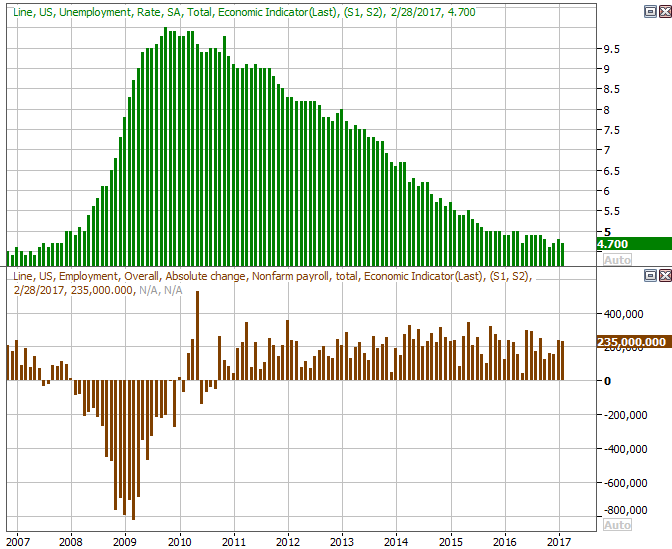

The specifics from Friday's morning's jobs report from the Department of Labor: The pros were only expected 200,000 new nonfarm payrolls, but they got 235,000. Wages were up too, and the average workweek of 34.4 was in line with the prior month's workweek length. That report mirrored a similar report from payroll processing company ADP posted earlier in the week. ADP was expected to report 180,000 jobs had been created in February, but the figure was actually 298,000.

All that data points to an improving labor market, which points to an improving economy, which in turn points to a need to raise interests rates sooner than later.

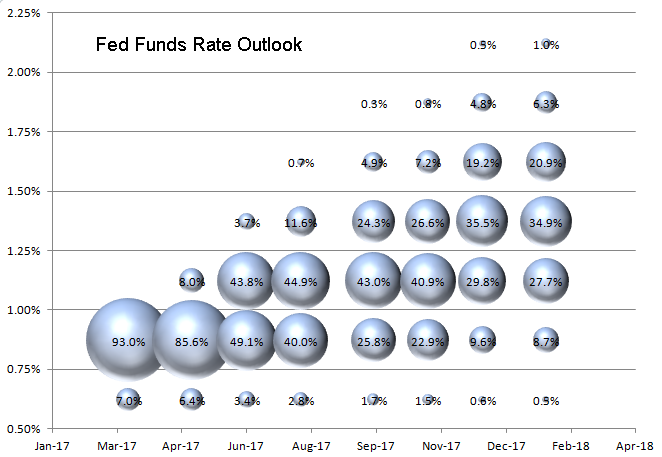

The market was already counting on higher rates this year, of course. All told, traders were pricing in three rate increases before the end of the year, with them being spaced out all the way through 2017 in anticipation of a gradual economic ramp-up. The first of them, however, was and still is expected this month; the Fed will get a chance to do so in the middle of the coming week.

The chart below tells the tale of the bets real traders are making with real money regarding the Fed Funds rate through the early portion of 2018. Traders have already priced in a 93% chance of a 1/4 point interest rate increase for March 15th. Moreover, they've already priced in a second rate hike in August (though just barely), and the third rate 1/4 point interest rate increase is expected either at the end of 2017 or the beginning of 2018. None of those odds are weak.

The one 'catch' to this outlook is simply that the bond market has already done a lot of this work preemptively, pushing rates higher in the recent past in anticipation of the Fed's moves in the near future. As such, there may not be a significant bump in market interest rates once Yellen actually pulls the trigger. On the other hand, there will likely be some sort of bump, even though yields have been inching higher for a while now.

The market tends to be more right about interest rates than the professional forecasters usually are, possibly because they have some real skin in the game. Economists and analysts can afford to be wrong - traders can't.

Whatever the case, following Friday's employment report, the Fed's going to be hard-pressed to not put a rate-hike in place.