Weekly Market Outlook - Even Unhealthy Progress is Still Progress

Kudos to the bulls. A week ago they stopped just short of some important lines in the sand, leading one to wonder if the then-rally was going to stopped before it really got started. Despite the wobbly start to last week, the bulls managed to follow-through on the rally effort in the latter half of last week. It wasn't an ideal move, as there's room and reason to expect profit-taking soon. It's something to build on though.

We'll explore the victory in detail below. First though, let's review last week's major economic announcements and preview what's coming this week. Spoiler alert: Cooling inflation is responsible for most of last week's market gains.

Economic Data Analysis

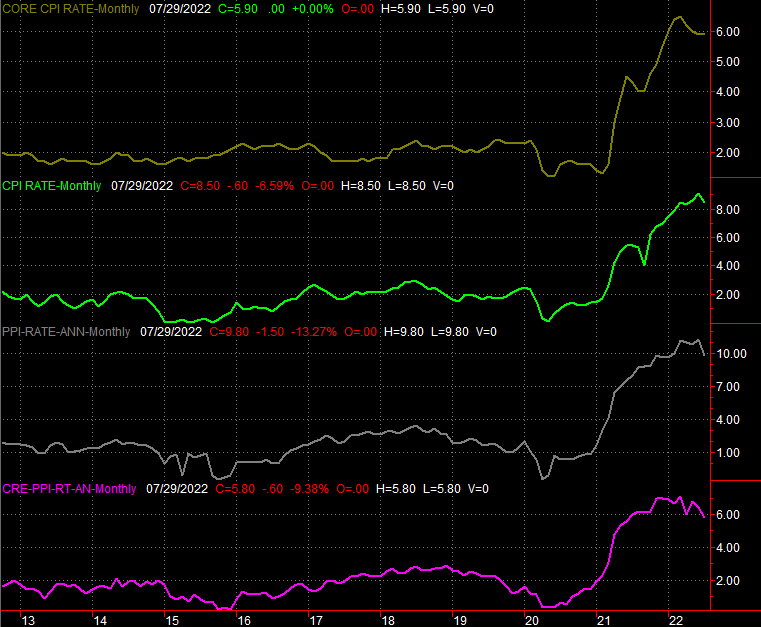

Inflation is cooling... relatively. Consumer and producer inflation rates fell from June's levels in July, to be specific, though they're still sky-high. The overall consumer inflation rate now stands at 8.5% (down from 9.1%), while the core consumer inflation rate rolled in at 5.9% again. Producers' prices slipped from 11.3% to 9.8% last month, and taking out food and fuel from the equation, producers are still looking at annualized inflation of 5.8%. That's down from June's reading of 6.4%.

Consumer and Producer Annualized Inflation Rate Charts

Source: Bureau of Labor Statistics, TradeStation

The slight lull in the annual inflation rates was obviously the prompt for last week's rally, and understandably so. While most investors understand inflation is still painfully high, they're interpreting last month's slight lull as a hint that prices will continue to cool. And, perhaps they will. It's far too soon to say this trend will persist though, and even if it does, prices are already broadly high enough to slow the economy down.

The point is, if curbed inflation is the only thing driving this bullishness, all these buyers may end up disappointed sooner or later, and sooner than later.

Everything else is on the grid.

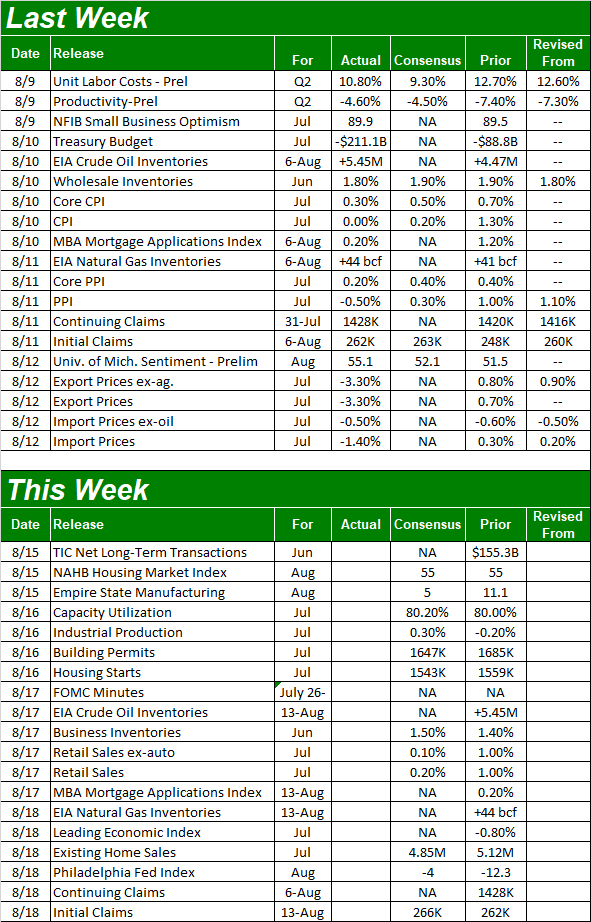

Economic Calendar

Source: Briefing.com

This week's got some market-moving reports in the lineup... real estate reports in particular. The party starts on Tuesday, however, with a look at last month's capacity utilization and industrial figures. Economists are looking for slight improvements for both, which would be a welcomed development following last month's slight stumble.

Capacity Utilization and Industrial Production Charts

Source: Federal Reserve, TradeStation

Also on Tuesday we'll hear July's housing starts and building permits figures. You may recall June's figures were more or less in line with May's, but May's figures were uncomfortably low. Analysts are modeling slightly lower figures this time around, again suggesting the housing market continues to weaken.

Housing Starts and Building Permits Charts

Source: U.S. Census Bureau, TradeStation

Brace for July's retail sales data on Wednesday. This has been a bright spot for the economy, indicating consumers are still spending despite higher prices. Forecasters believe retail sales growth cooled dramatically in July though. Here's the thing... much of that slowdown reflects falling prices. Overall spending is still pretty healthy.

Retail Spending Charts

Source: U.S. Census Bureau, TradeStation

Last month's sales of existing homes will be published on Thursday, though new home sales figures won't be released until next week. This is where we've seen real estate pain, with new home sales reaching multi-month low levels just last month. In fact, removing the outright shutdowns linked to COVID-19's arrival in the United States, sales of new and existing homes reached multi-year lows just last month. Economists don't anticipate any relief this time around either, and are actually calling for another moderate decline is sales of existing homes for July.

New and Existing Home Sales Charts

Source: U.S. Census Bureau, National Association of Realtors, TradeStation

It's nothing to chart, but also know that the minutes from the Federal Reserve's governors most recent meeting will be posted on Wednesday. This is always important insight, but it will be especially important this time around, as it may tell us what to expect about future interest rate increases.

Stock Market Index Analysis

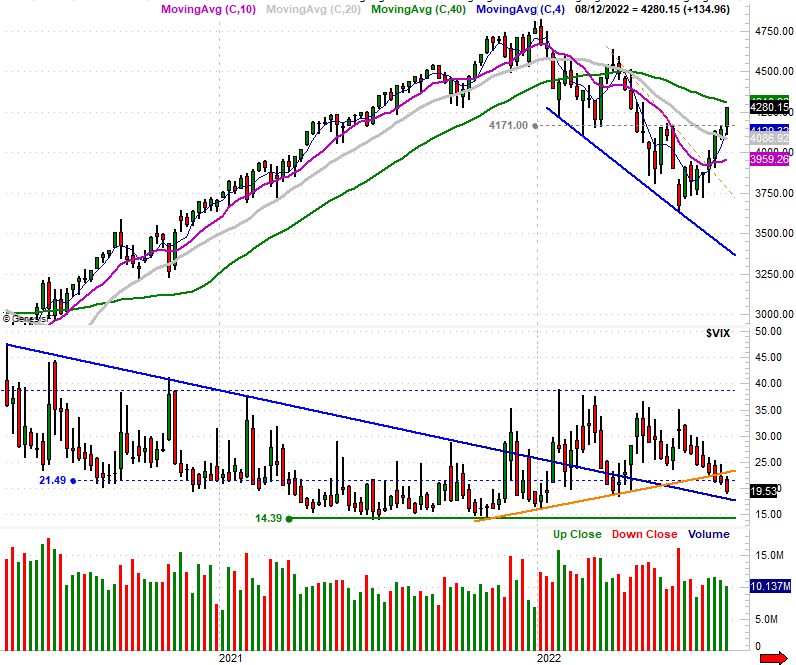

The S&P 500 rallied 3.2% last week, and in so doing, hurdled a key resistance level we discussed a week ago. That's the 4171 mark, where the index stalled and then rolled over in late-May and early June. As the weekly chart of the index also shows us below, the volatility index (VIX) is now firmly below a major support level.

S&P 500 Weekly Chart, with VIX and Volume

Source: TradeNavigator

It's not the perfect rally effort, however. Take a look at the daily chart of the S&P 500 below. As you can see from this vantage point, the index left behind a pretty big bullish gap on Wednesday, and while Friday's gain was powerful, it was also a rally made on light volume -- it may not represent a majority opinion.

S&P 500 Daily Chart, with VIX and Volume

Source: TradeNavigator

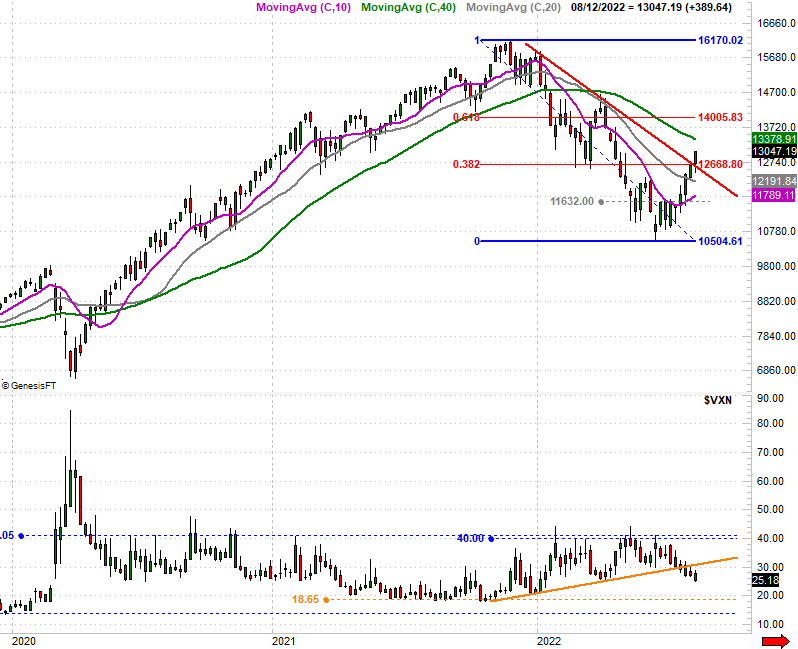

The NASDAQ Composite punched through some ceilings of its own, the biggest of which is the 38.2% retracement line at 12,669 we discussed a week ago. The composite's 3.1% gain from last week caps off a 24% advance from June's low, in step with the NASDAQ Volatility Index's confirmed slide below its rising support line (orange) that had been steering it higher since late last year.

NASDAQ Composite Weekly Chart, with VXN

Source: TradeNavigator

The daily chart of the NASDAQ Composite below shows us the index also pushed through a key technical resistance line last week as well (red), after stalling at that line a week ago. As was the case with the S&P 500, however, the NASDAQ also left behind a gap on Wednesday that traders may feel needs to be filled in. It doesn't have to be. But, if investors think it, they're apt to act accordingly.

NASDAQ Composite Daily Chart, with VXN

Source: TradeNavigator

The current trend is bullish, so we have to assume that trend will remain in motion until it's clearly broken. Just be cautious, as usual, though perhaps even more than usual. If there's one thing the market hasn't done well of late (particularly this time of year) is make bullish follow-throughs on young rally efforts. This one's gone on longer than you'd normally expect. Let's see how well it holds up when really tested.