Active beats passive in downturns, but not enough to make it worthwhile, Morningstar says

- Active stock funds hold up better during down markets, but the success doesn't last, Morningstar analyst writes -

By Ryan Vlastelica, MarketWatch

Amid a decadelong period of dominance by passive investing, which has seen both greater adoption and better general performance than its active investing rivals, portfolio managers have had one primary argument: investors, you're going to miss us when things turn rough.

Active managers have long maintained that they are better positioned to perform in the event of a market downturn, and new data from Morningstar gives some credence to this point of view, although not so spectacularly so that the analyst views it as a reason to favor active products over passive.

The basic debate is this: passive products mimic the performance of an underlying index like the S&P 500 holding the same securities it does, in the same proportions. What this means is that by definition, an index fund will never do worse-or better-than the index it tracks, so if the market were to correct or fall into a bear market (defined as a 10% and a 20% drop from a peak, respectively), so would an S&P fund.

In contrast, the components of an actively managed portfolio are chosen at the discretion of a manager, who in theory can pick undervalued or high-growth names, or otherwise position in a way that the fund avoids the full pain of any decline.

For years, using passive products have been a highly successful strategy. Data have repeatedly shown that few active funds have been able to outperform the broader market on a long-term basis, particularly when the lower fees of passive funds are taken into account. This has contributed to wide adoption and proliferation of passive funds. Over the past year, $68.9 billion has moved into passive U.S. stock funds, according to Morningstar Direct, while $202.8 billion has been withdrawn from active ones.

Passive strategies have also gotten a boost from a bull market in its ninth year that started in the wake of the financial crisis. Stocks rose broadly in the rally, creating what was sometimes referred to as a "rising tide" market where basically all sectors and securities benefited. Active funds are seen as having a harder beating a market that is already performing well.

A blip to that uptrend-stocks had previously been almost completely bereft of volatility or even mild pullbacks-came in early February, when the S&P suffered its first correction, defined as a pullback of at least 10% from a recent peak, in about two years.

So, did the active prediction of better performance come to pass? For the most part, yes-although those who think this ends the debate shouldn't necessarily rest on their laurels.

According to Jeffrey Ptak, global director of manager research at Morningstar, the recent retrenchment in equities was "actually a pretty good period for actively managed U.S. equity funds," though he noted it was "a very short period of time" being analyzed.

Per his data, 57.4%% of actively managed funds did better than their benchmark in the period from the market's most recent record (Jan. 26) though a subsequent closing bottom (Feb. 8). That's higher than recent statistics; according to Morningstar's "Active/Passive Barometer," 43% of managers across its nine equity segments (for large, mid, and small-cap stocks, and value, growth, and blend strategies) beat their benchmark. Even that represents improvement, as only 26% did over 2016.

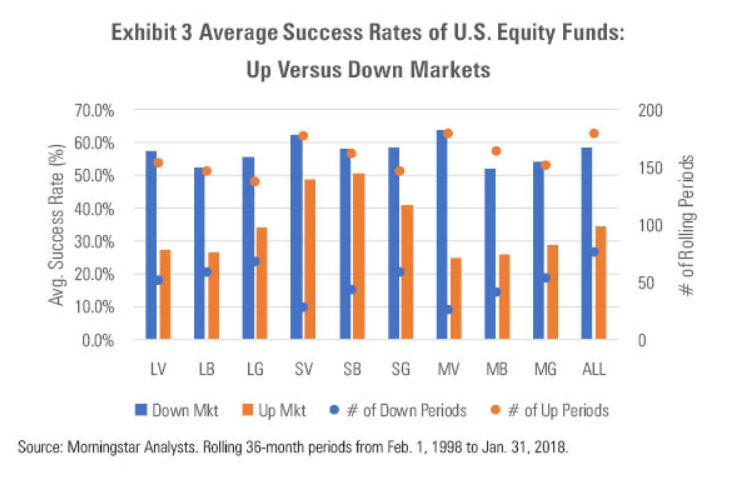

"There is a kernel of truth to the notion that active funds perform a bit better during downturns," Ptak said in an internal interview that he followed up with a blog post. "All told, nearly 60% of active U.S. equity funds outperformed their bogy in down periods, on average. By contrast, only about 32% of active U.S. stock funds beat their indexes in up periods, on average, meaning the odds of succeeding were almost twice as good when the market was down than when it was up."

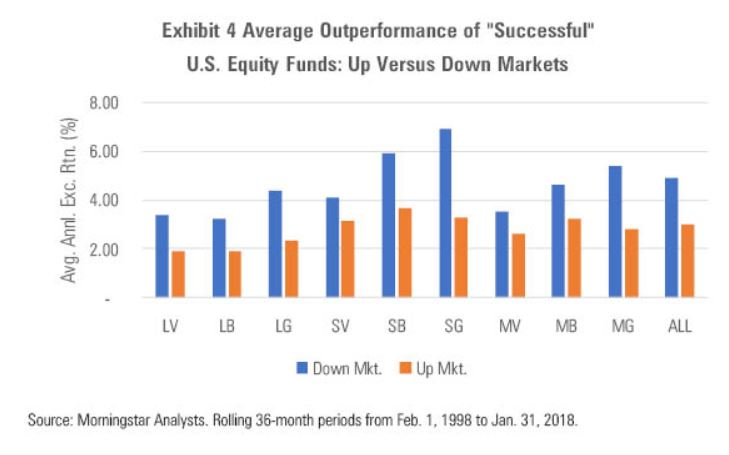

Furthermore, the degree of outperformance for market-beating funds in a down market is "far wider" than for funds that outperform in rising markets. "In other words, success was more frequent and the payoff larger in down markets than up markets, on average."

In the following charts, categories beginning with L, S, or M refer to large, small, or midcap funds, respectively, while V, G, or B stands for value, growth, or a blend.

Courtesy Morningstar

Courtesy Morningstar

Periods of broader active outperformance has long been viewed as cyclical, as seen in the following graph, which was provided by Altus Securities and uses data from the Center for Research in Security Prices.

"Active managers may outperform their passive peers in the latter part of a recovery, where we believe this recovery may be," Wells Fargo wrote last year.

Despite these statistics in favor of active managers, Ptak said there were still reasons to favor passive strategies. For one thing, getting the benefit of active outperformance means the investors has to have chosen the right fund ahead of time, which is extremely difficult. Furthermore, "There were far more up periods than down periods during the 20-year span we examined," he wrote, with more than 175 of the former and about 75 of the latter.

In addition, the funds that do outperform their benchmark typically don't maintain that outperformance for long. Of the funds that outperform in a "down" 36-month period, only a third of them continue to outperform in the subsequent one, which is typically a positive period for the market.

"Defenders of active U.S. equity funds have been right...and wrong," he concluded. "Right in the sense that they appear be correct that active stock funds hold up better during down markets than their indexes. But wrong in that the outperformance hasn't translated to long-term success, as up markets have greatly outnumbered down markets and success has proved fleeting, especially among active funds that have beaten their bogies during down markets."

That more funds hold up, he said, "is not sufficient reason" to choose active stock products over passive ones.

From MarketWatch