Weekly Market Outlook - The Bulls Are On the Ropes

After 17 weeks of sheer bullishness since the end of October followed by six weeks of mediocrity, the market was finally dealt a decidedly painful blow. This is the most reason the bears have had to be motivated in months.

Will the sellers be able to do anything with the opportunity? That remains to be seen - the deal's not entirely sealed yet. There are some read lags waving, however, that we haven't seen waving in a long, long time.

We'll examine those red flags below, but first, let's take a look at last week's and this week's economic news. We've got a couple of market-moving data sets in the lineup, and we need to be prepared for them.

Economic Data

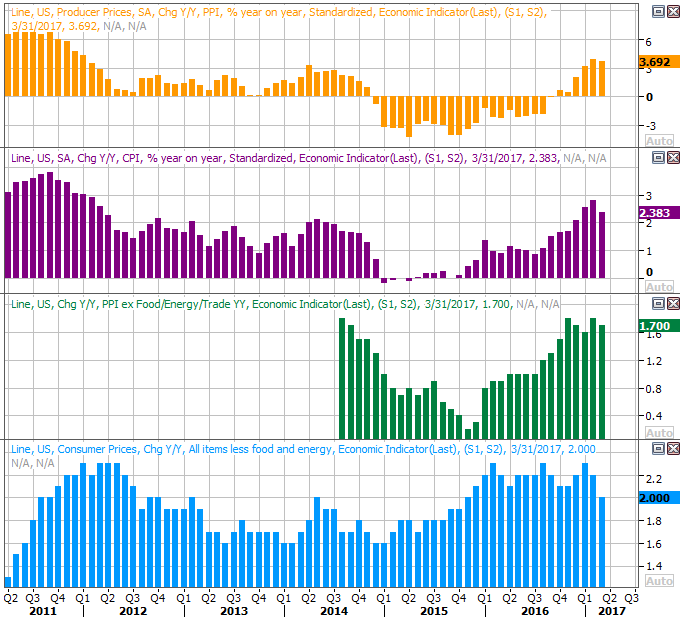

In February and March, inflation levels -- which were already on the rise -- reached a point where the Federal Reserve had no choice but to do what it could do to quell the rise. And it did. Last month, the Fed upped the Federal Funds Rate by a quarter of a point for the first time in months. It worked, though one can't help but wonder if it worked a little too well. Producer prices fell 0.1% overall in March (month-to-month), and on a core (ex food and energy) they were flat. Consumer inflation fell 0.3% on an overall basis, but stripping out the costs of energy and food, they were still off 0.1%.

Producer and Consumer Inflation Charts

Source: Thomson Reuters

On the more important year-over-year basis, inflation is still in positive territory no matter how you slices it. A couple more months like last month though, the and Federal Reserve will have plenty of time and reason to back off on its hawkish plans.

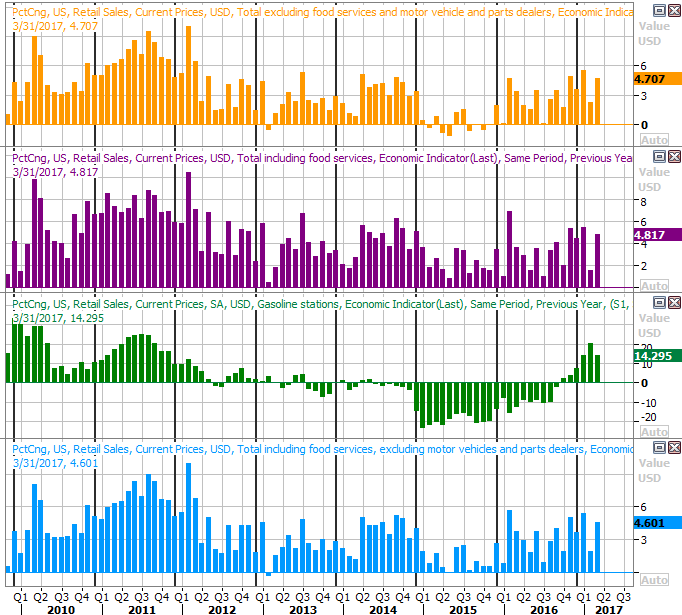

The only other item of real interest last week was March's retail sales growth. These too fell on a month-to-month basis, thanks to weak car sales. But, even taking automobiles out of the equation, consumer spending was flat. On a year-over-year basis though, retail consumption continues to rise in all stratifications. That's the more important growth comparison.

Retail Sales Year-Over-Year Growth Charts

Source: Thomson Reuters

Everything else is on the grid.

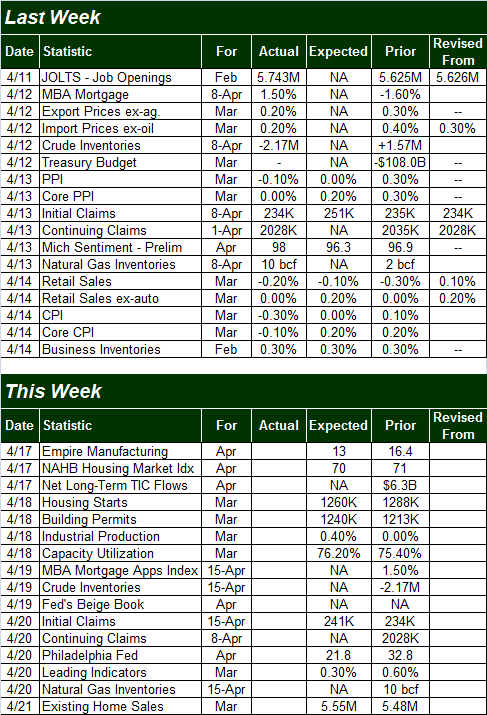

Economic Calendar

Source: Briefing.com

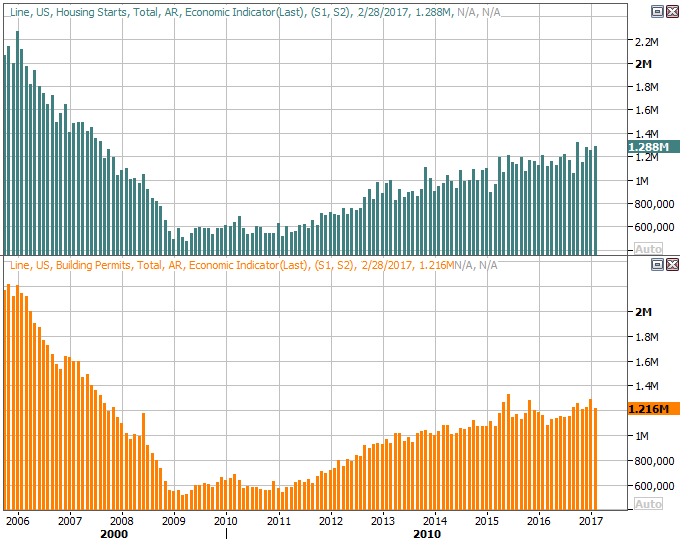

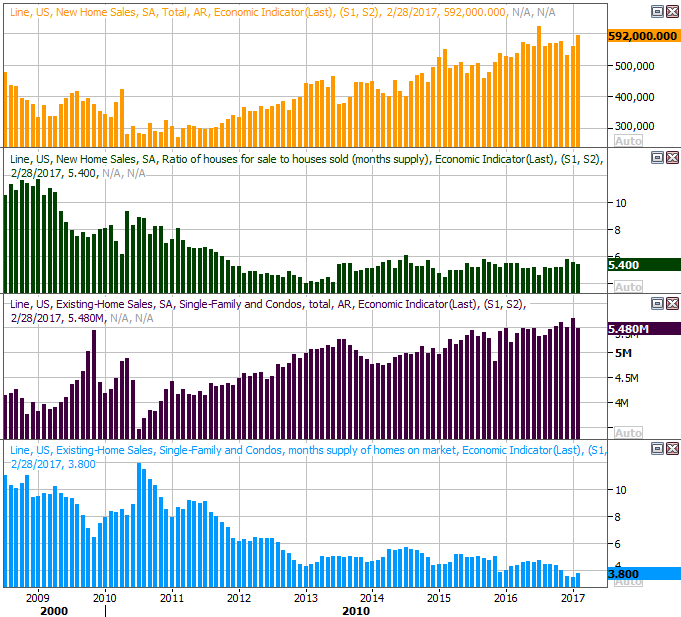

This week will be a slightly busier week, particularly when it comes to real estate data. On Monday we'll hear the NAHB Housing Market Index score for April, on Tuesday we'll get last month's housing starts and building permits figures, and on Friday look for March's existing home sales data. Starts and permits are expected to fall just a bit from February's levels, and sales of existing homes are projected to rise a bit. In all cases though, the bigger trends are still positive ones.

Housing Starts and Building Permits Charts

Source: Thomson Reuters

We won't get new homes sales numbers for last month until next week, but that trend through February still appears on our chart below... along with inventory levels for each.

Existing Home and New Home Sales, Inventory Charts

Source: Thomson Reuters

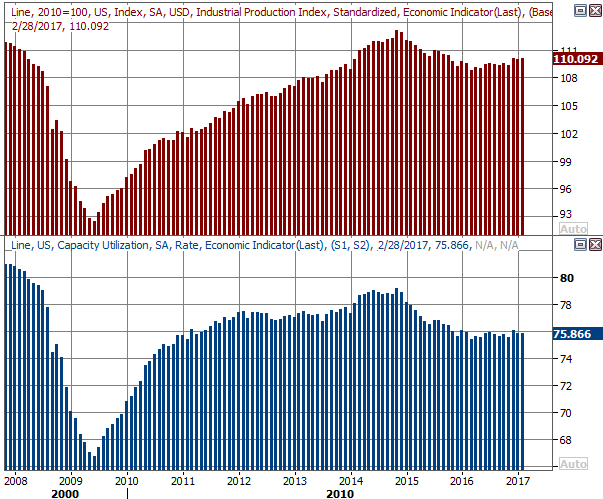

This week we'll also hear about March's industrial production and capacity utilization - two of the data sets that show a very strong correlation with the market's long-term earnings trend (and two tools that reliably move in tandem with overall economic cycles). Economists are expecting measurable growth for both measures, and we need it. Though both have been logging shallow improvements since early last year, we need more and better if the economy is to reach escape velocity.

Industrial Productivity and Capacity Utilization Charts

Source: Thomson Reuters

Index Analysis

It's still a little too soon to say the market's beyond hope for the near term. It's not too soon, however, to start having that conversation. Indeed, the pressure is now officially on the bulls to prove to... well, everyone that the overdue pullback has started.

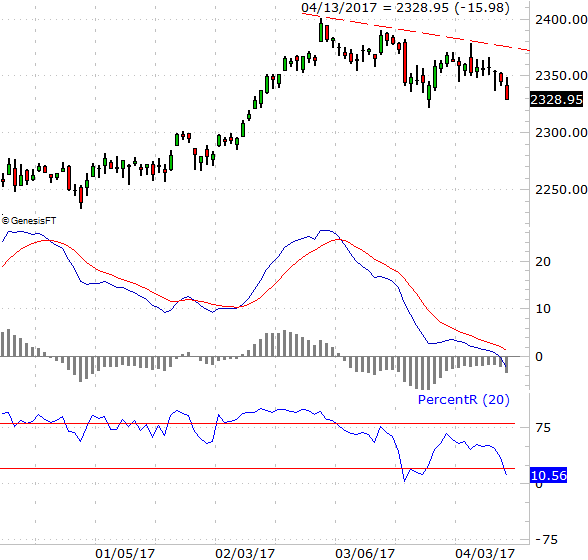

The daily chart of the S&P 500 below tells the bulk of the relevant story right now. Last week's close of 2328.95 is the lowest close in weeks, and worse, it's the first closer below the lower Bollinger band we've seen since early March (well before we had any good reason to think the broad uptrend was in trouble.

S&P 500 Daily Chart

Chart created with TradeNavigator

Realistically speaking, if history is any indication, there are going to be some bulls that push back early this week. The VIX's doji bar from Thursday also suggests it's ready to pivot. Don't get too excited about it if that happens though. Unless that bullishness actually pushes the S&P 500 above the 20-day moving average line, the bears are still in control. In fact, the 20-day line (blue) is on the verge of crossing below the 50-day moving average line (purple) at a fairly important 2353 level. If that happens, it will be the first time we've seen it since November, confirming the short-term weakness has turned into a full-blown trend.

Zooming out to a weekly chart of the S&P 500 we can glean a little more perspective on how the bigger undertow is shifting, and why it should. It's also in this timeframe we can see that, though the VIX may dish out a small pullback from Thursday's pivotal bar, there's still a ways to go before the VIX reaches its prior key peak levels.

S&P 500 Weekly Chart

Chart created with TradeNavigator

So what will seal the deal on a downtrend? Let's flip back to a different version of the daily chart of the S&P 500 to answer the question.

On the chart of the index below we've plotted MACD lines and a PercentR indicator. The MACD lines are already in confirmed bearish territory. The PercentR line almost is. A confirmed PercentR sell signal is made when the PercentR line moves higher with the market but does not break above the 20 threshold, and then moves lower again on a day the S&P 500 itself makes a new low (below Thursday's low of 2328.95).

S&P 500 Daily with MACD and PercentR Chart

Chart created with TradeNavigator

We might get that signal this week. Or we might not get it at all. It certainly looks like it's only a matter of time though. It all really depends on how traders respond to any bullish pushback. Will they pile on and prolong it, or will they use it as a last chance to get out at a decent price?

If the market manages to punch through the 20-day moving average line this week, we can start talking about upside targets then. Assuming the bearishness persists, the most logical downside target from here is the S&P 500's 200-day moving average line (green) currently at 2230. It's not likely we'll get there in a straight line though.