May Jobs Report Was Healthier Than Headlines Suggested

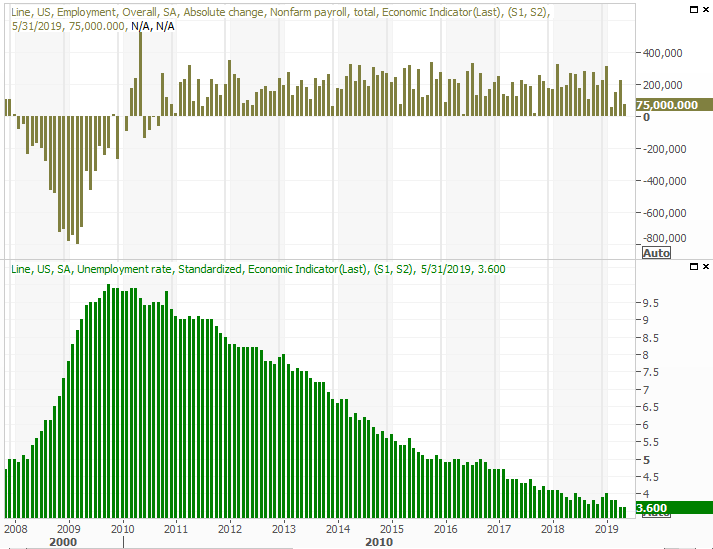

The most-touted number was admittedly ugly. That is, versus expectations of 175,000 new jobs added for May, the actual figure of 75,000 is a concern. Stocks rallied on the report, which didn't alter the unemployment rate of 3.6%, as it suggests the Fed has room and reason to not only hold off an raising interest rates, but could even lower them.

It's a dubious victory though.

Whatever the case, the rest of the numbers that largely go unmentioned by the media actually look rather solid again. Although that won't stave off a short-term selloff from stocks, it does bode well for the bigger-picture market. There's still no solid evidence that a recession is in the works.

But, first things first. Last month's addition of 75,000 new payrolls is the second-lowest figure seen since late 2007, though the unemployment rate of 3.6% keeps that figure as the multi-year low it hit in March.

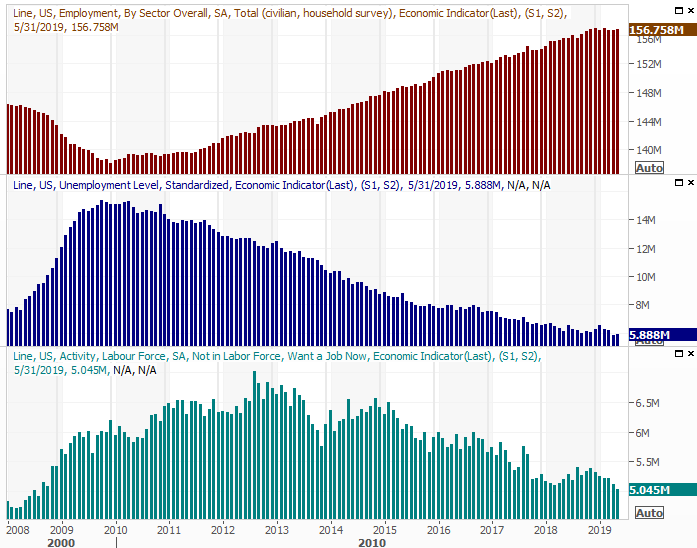

To that end, the total number of people in the United States with a job ticked higher again, from 156.645 million to 156.758 million (an increase of 113,000, using numbers other than the ones used to calculate actual payroll growth), while the number of officially unemployed individuals (those receiving benefits of some sort) edged up from 5.824 million to 5.888 million... a 64,000 increase. Where the real progress was made was in the number of people who aren't being counted as unemployed, but would still like to have a job. That figure fell from 5.121 million to 5.045 million a 76,000 decrease.

Those numbers don't jibe with the primary figures, which is why they're worth reviewing. In this case, the headline numbers arguably understate the true health of the jobs market... though not by a great deal.

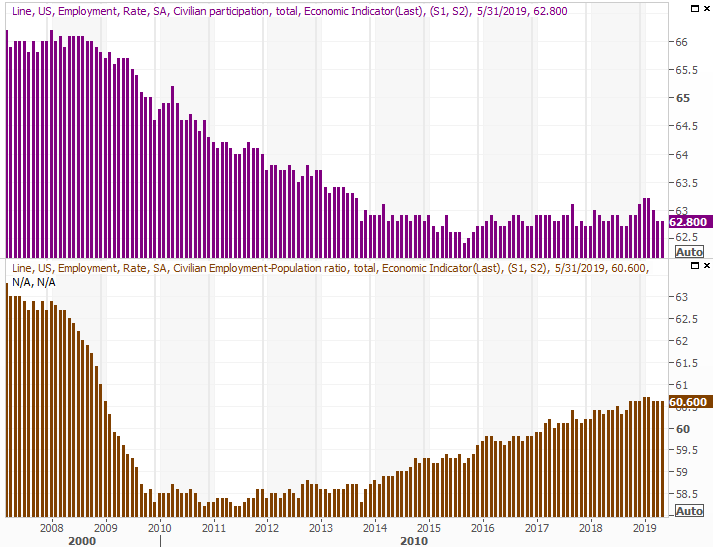

Underscoring the lukewarm read on the jobs picture is last month's employment/population ration and the civilian participation rate in the nation's labor pool. Like April's score, May's employed/population rate came in at 60.6%, while the number of people officially in the workforce (though not necessarily working) was once again 62.8%.

This may be the new norm, as the dust from the en masse retirement of baby-boomers settles and the economy hits a healthy but not overheated plateau.

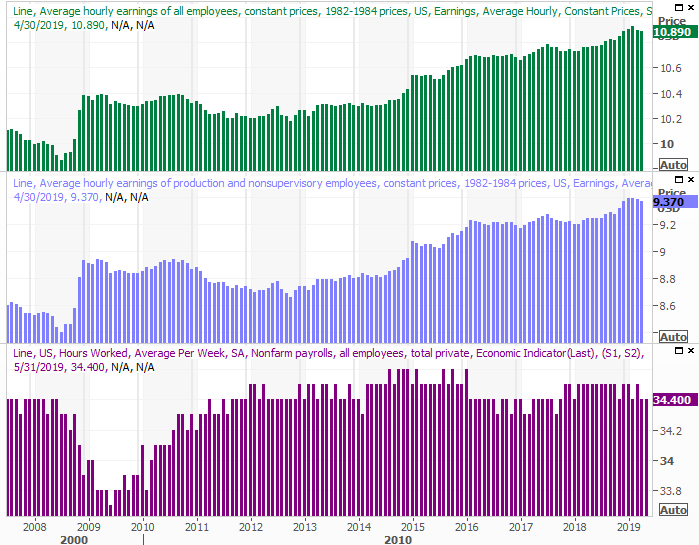

Wages are also just so-so. Hourly pay was up 0.2% for the month versus expectations of 0.3%, while the year-over-year increase of 3.1% versus estimates of 3.2%. The uptick reverses a slight decrease seen in the prior couple of months, and outpaces inflation. But, just barely. [The graphic below is only updated through April.]

Still, perhaps a more tempered rise in earnings is exactly what the economy needs to enjoy forward progress without fostering problematic inflation rates.

Brian Coulton, chief economist at Fitch Ratings, believes that is indeed the case, explaining "While the slight decline in wage growth will support the Fed's patient stance on rates, the average pace of job growth over the last 3 months (at 151,000) is hardly alarming. It speaks to a slowdown in the domestic economy but there's no suggestion of demand falling off a cliff."

That may be the ideal scenario in the latter stages of an economic growth cycle.

While far from impressive, a lackluster but serviceable print for May could be exactly what the market needed, buying time for the Fed, but not because the economy is in shambles. An end to the tariff war could still spur hot growth, but starting somewhat against the tide could make that move more sustainable for a longer period of time.

In other words, often times, raw strength comes at a price. Sometimes mediocrity sets the stage for a long-term win.