Verizon (VZ) Shares Taken to the Brink by Earnings

In the grand scheme of things, it could have been worse for Verizon (VZ) shareholders following a disappointing first quarter report. On the other hand, it should have been better.

For the quarter ending in March, telecom giant and wireless leader Verizon earned 95 cents per share on revenue of $29.8 billion. The pros, however, were looking for a profit of 97 cents per share and sales of $30.57 billion. Worse, both figures were down from the year-ago top line of $32.17 billion and bottom line of $1.06 per share of VZ stock. The company lost 307,000 higher-value postpaid customers for the recently-completed quarter, translating into churn of about 1.15%.

It was the second consecutive earnings miss for the company, though waning sales and profits aren't anything new. The wireless market reached a saturation tipping point a little over a year ago, and to continue winning market share all the players in the business began lowering prices, offering sweeter deals, and accepting weaker margins. Shareholders have suffered the brunt of the new mindset. VZ is down 1.5% today, and is currently trading at the same price it was trading in March of 2013.

It could have been worse though, and still may be.

For the time being, the knee-jerk selling was stopped at February's low, where the stock logged a double-bottom. The bulls appear willing to try and close the bearish gap left behind by today's open, though there are no guarantees. The gap from January has yet to be filled.

That being said, the bigger tide is still ultimately turned against Verizon shareholders. As the weekly chart of VZ below shows, the stock's already logged a couple of lower highs, and arguably, a couple of lower lows. The key line in the sand is the $45.20 level, where Verizon made several major lows in 2013 and 2014. It fell under that mark in 2015, though in retrospect that appears to be an anomaly that can be disregarded.

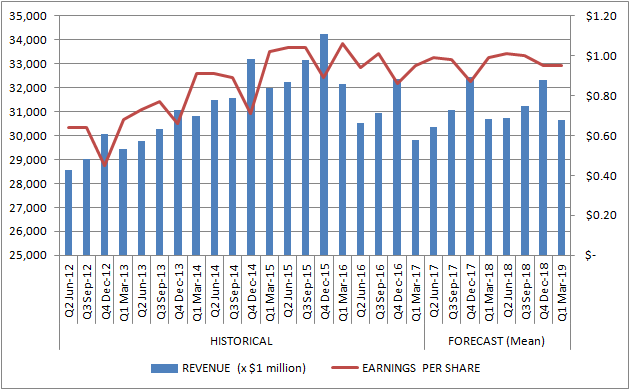

Investors have good reason to suspect the worst is in store for Verizon. Though revenue and earnings growth was tremendous through late 2015, past that point began what became a brutal price war. The tumble in sales and stagnation in earnings then is crystal clear on the chart of both below, and analysts don't foresee significant growth on either front through at least the first quarter of 2019.

This outlook doesn't include the impact the addition of Yahoo (YHOO) will have on Verizon's books. That deal will close within a few weeks, and will be reflected on Verizon's books as of the next quarterly report. Know that Verizon's AOL, though it got off to a great start shortly after the 2015 acquisition, saw its revenue fall 4% last quarter. Yahoo's top and bottom line were up for Q1, though there's little doubt Verizon has its work cut out for it in terms of turning Yahoo around. The recently-weak chart of VZ suggests investors aren't giving the company the benefit of the doubt.