July's Jobs Report Was Even Better Than the Headlines Suggested

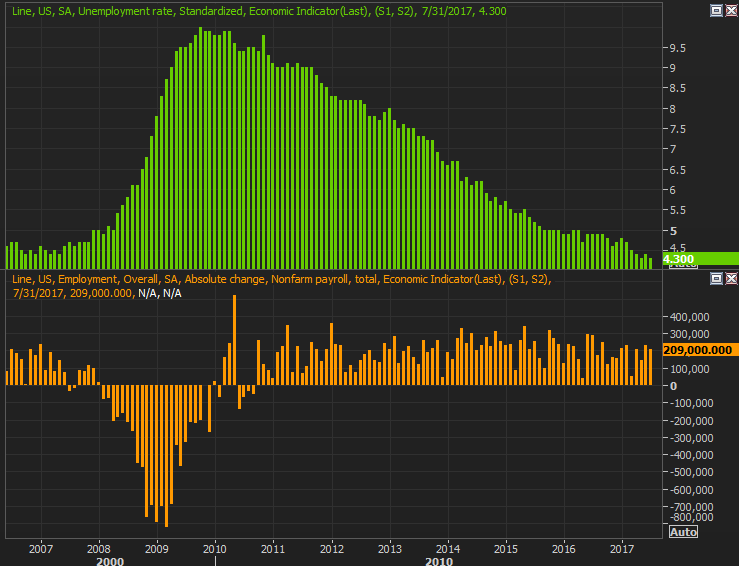

Anyone reading this likely already knows just how good Friday's morning's employment stats for July were. Though already at rock-bottom levels, the unemployment rate managed to ratchet down another notch to 4.3% on the heels of 209,000 new payrolls. Economists were calling for an unemployment rate of 4.3%, though they were also only looking for 181,000 new jobs.

It's a pretty significant victory. Thing is, the headline numbers may actually understate just how good things are now. But, first things first.

Now at 4.3%, the nation's unemployment rate stands at a seventeen-year low. Last month's 209,000 newly-created jobs is actually less than June's revised total, though a firm figure all the same in that there aren't a lot of people left that don't have jobs; they may simply be switching jobs, or getting a better job.

Far more indicative of strength in the employment market is the raw underlying data... the headcounts of people without, without jobs, and the number of people without jobs but also not actively looking for one.

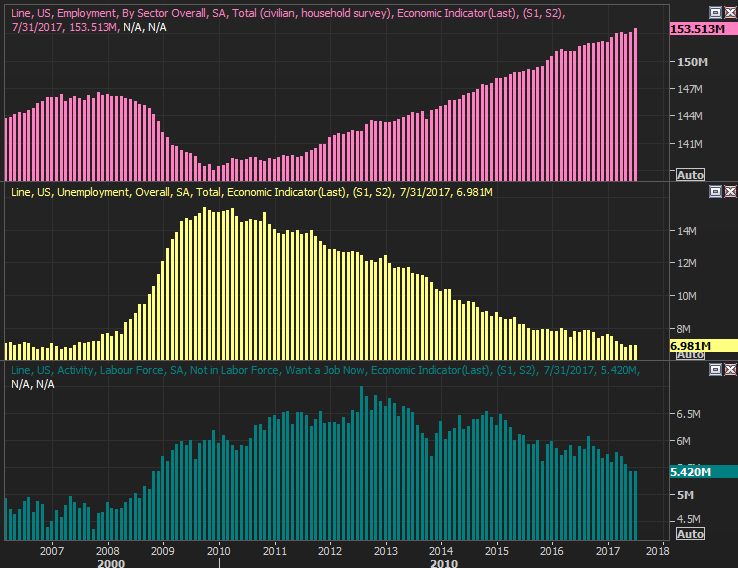

On that front, the 153.51 million people in the country who are gainfully employed is an all-time high. Conversely, while the 6.98 million people who are officially unemployed (receiving unemployment benefits) may not be a record low, but it's near an absolute recent low, perhaps unable to move any lower for structural/systemic reasons. Ditto for the number of people not counted as part of the labor force though still technically wanting a job. That figure stands at 5.42 million, sustaining a broad downtrend that began in 2013.

In that same vein, one of the sore spots for several years now has been a tepid labor force participation rate, as well as a lackluster employment/population ratio. The latter started to edge higher in 2014, though the former has remained weak since bottoming out in 2015. We're seeing signs of life on both fronts now though. The employment/population ratio has rekindled its bigger uptrend with two consecutive rises, while the labor force participation rate appears to be working on rekindling its recovery effort as well.

Holding both back is the ongoing retirement of baby boomers, so both of these figures may actually be quite strong; it's difficult to gauge how many older Americans are not working by choice, and not working because they've been forced out. The answer is a vague "some."

Finally -- and perhaps most important -- wages are decisively on the rise. They have been ever since Trump started his "America first" jobs agenda.

This may be the ultimate litmus test in terms of measuring the strength of the U.S. jobs market. While there's little to no room left for job growth (simply because everyone who wants a job has one... maybe even a lousy one), wages better indicate the actually supply and demand relationship between employers and employees. If wages are moving higher, employers are more desperate to attract and retain talent, but can afford to do so as "business is good.

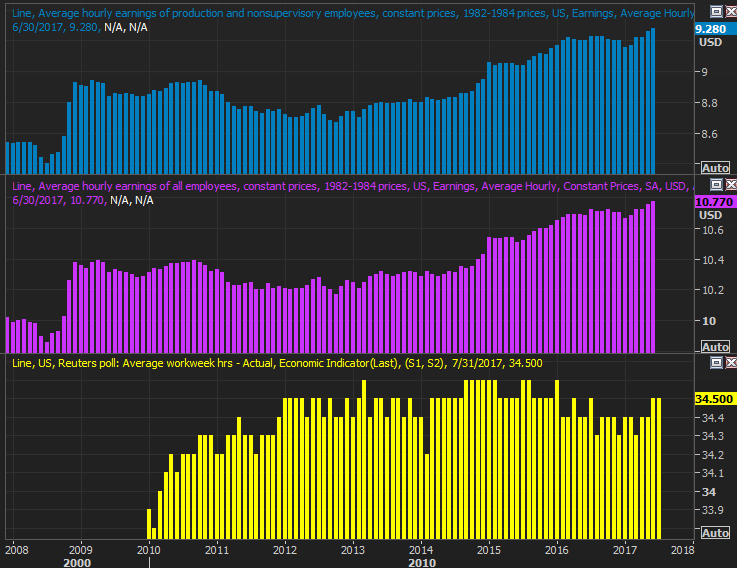

Apparently business is good. Hourly wages reached an all-time record last month, marking strong growth in four out of the past five months.

It's not a case where hourly rates went up but the number of hours worked went down either. The average workweek remained at a firm 34.5 hours for a third month in a row, as of July.

None of this is to suggest the market can't pull back. Stock prices are a function of sentiment in the short run, and earnings in the long run, and the market is arguably overvalued right now relative to earnings. Those earnings are most likely expanding though, as consumers have more to spend, and employers are more willing to spend on employees.

In other words, the economy remains on firm footing. Now it's time for publicly-traded companies to make the most of it (and most of them are).