As has been noted more than once, the broad market's year-over-year earnings growth for Q1 has been impressive, but should be taken with a grain of salt. The first quarter results from 2016 were horribly bad for oil and gas companies, and that's not the case for the recently completed. They're still far from 'good,' though.

Nevertheless, the current readings are never the whole story. Just as important -- if not more so -- is the trajectory of the industry's results. In that light, the picture is pretty compelling. Revenue us up partially on the heels of higher oil prices since year-ago levels, but earnings are decidedly better as most of the key names in the business have done a good job of culling costs and thinking more strategically when it comes to capital expenditures. Being efficient with capital is the new norm.

The question remains though... just how far have oil and gas companies come, and how much further might they have to go to say they've fully recovered.

As is usually the case, a picture tells the story better than mere words can.

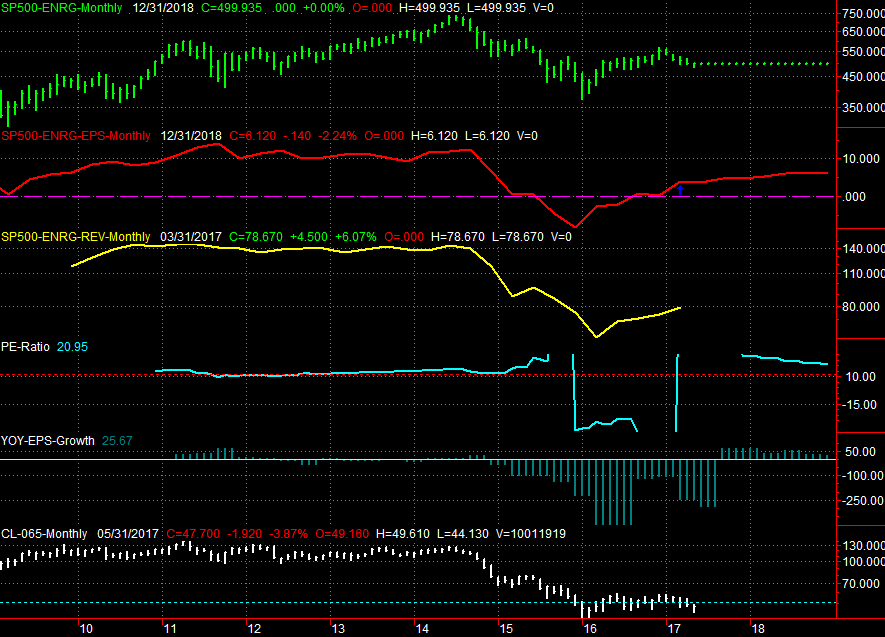

The image below is of the S&P 500 Energy Sector Index. With it appears its revenue trend through the first quarter, its per-share earnings trend through the first quarter, and its earnings projections for Q2 of this year through the end of 2018. Also plotted is what's arguably the most important detail in the matter -- the price of crude oil. Take a look. (Click to enlarge it.)

It is what it is. Q1 was a nice swing to a profit. But, we're still nowhere near the kinds of quarterly earnings we were producing between 2011 and 2013; quarterly income for the S&P 500 Energy Sector then was on the order of $10.00 to $11.00 per share, when crude was trading in the $100's. Now crude is struggling to hold onto $50 per barrel.

Revenue has improved after bottoming in the first quarter of 2016, which was a quarter after the industry's earnings hit bottom. By then the key players were already waist-deep in their defensive maneuvering. The benefit of that careful handling of a tough situation became evident over the course of 2016, and now early 2017. That is, while oil prices haven't really moved above their rebound prices reached by mid-2016, profits have continued to rise on a relatively modest sales recovery.

Still, the outlook is anything but exciting. Though the sector is back on a track to sustained profitability, it's nothing like the kinds of profits we were seeing just four years ago. And, with oil-price projections saying it's not going to exceed the $60/barrel level anytime soon, it's not like we have good reason to believe analysts are low-balling the group's 2017/2018 profit outlooks.

Cost-reductions aren't going to help as much going forward either. Any kind of meaningful cost-paring efforts have already been put into place.

To that end, the forward-looking (2018) P/E is still a rather frothy 20.9; the trailing P/E is 160, as trailing-twelve-month earnings are being bogged down by the Q1-2016 earnings disaster. Even once the ill effects of those losses are no longer part of the equation though, the scenario isn't exactly thrilling. The 2017 earnings-based P/E is still 28.6, and that's with four straight quarters of positive profitability.

The point is, while the energy sector may be past its dire straits, these companies have and will continue to have valuation problems relative to their realistic earnings potential. Unfortunately, there's not a lot they can do about it. This is apt to keep a lid on any long-term upside some hopeful oil bulls who had been entertaining stepping in for the long haul while these names are "bargain-priced." Bargains are only worth buying if there's a legitimate shot that the stock in question will justify a higher price in the foreseeable future. That's just not happening here with energy names (though the turnaround strides they've all made have been commendable).