Here's why stock-market investors need to get used to rising volatility

VIX has never been so sensitive to real yields and long-term inflation expectations at same time: SocGen

The stock market can continue to rise, but the ultralow volatility backdrop that accompanied the relentless 2017 rally is gone and investors will need to adjust, said a pair of quantitative analysts at Societe Generale.

While the U.S. macroeconomic picture has seen only a whiff of higher U.S. inflation and wages, "it should no longer provide a security blanket for risk takers," wrote Jitesh Kumar and Vincent Cassot in a wide-ranging Wednesday note that cited a variety of factors that have effectively set the stage for a return to more normal levels of volatility.

That dovetails with the narrative favored by some macro traders and economists, who argue that the Federal Reserve is moving to normalize monetary policy, a shift that will see less hand-holding for market participants who have grown accustomed to the notion of a so-called Fed put that saw policy makers rush to assure market participants in bouts of market weakness.

For their part, the SocGen analysts noted that the Fed "is more tolerant of market volatility, and central-bank balance sheets are gradually becoming lighter. Hence, options-market flow could move further away from the kind of short vol carry trade that flourished in the recent past, and which have been fueling the depressed volatility environment."

Volatility, as measured by the Cboe Volatility Index or VIX, spiked above 50 earlier this month as the stock market sold off. The VIX, which is calculated using options on the S&P is a measure of expected, or implied, volatility over the next 30 days.

The VIX rose 1.11 points Wednesday to trade at 19.70, near its long-term average of 20. The VIX last year had often traded near or below 10, testing all-time lows.

A popular volatility carry trade on Wall Street mostly entailed betting for the VIX's price to remain subdued, if not fall, and using the proceeds from that wager to buy stocks on their dips.

The index's early February spike wrecked the short-volatility trade. A pair of leveraged vehicles used to bet against rises in volatility collapsed and others were left bruised and battered, sending shudders through financial markets. Worst-case fears of broader, forced selling were largely averted, however, with stocks taking back a large chunk of the ground lost in the pullback.

Meanwhile, investors are likely to show more prudence when it comes to selling volatility, ending the trap and leaving the "abnormally low volatility environment," which they describe as 1-month realized volatility of less than 5% or a VIX below 10%, behind.

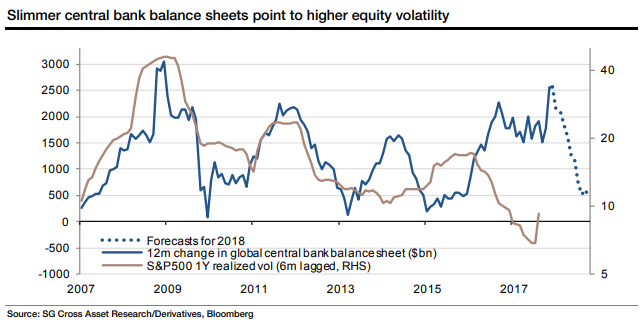

As far as macro factors are concerned, the analysts said the unwinding of central-bank balance sheets would make for lower liquidity and should allow volatility to rise. The Fed is in the midst of reducing a balance sheet that swelled to around $4.5 trillion in the wake of the financial crisis.

In the chart below, the analysts juxtapose the 12-month change in total central bank balance sheets with equity volatility.

"Until the taper tantrum, it seems like central banks increased the size of their balance sheet in response to deteriorating market conditions-causing the two graphs to move in sync," they wrote. "However, since the taper tantrum, any expectation of less liquidity or a slowdown in balance sheet growth has been accompanied by higher equity vol."

Meanwhile, even though neither 10-year real, or inflation-adjusted, yields nor long-term inflation expectations have managed to break through to five-year highs, global markets are growing more sensitive to the data, the analysts said.

Indeed, it was a stronger-than-expected reading on wage growth in the January U.S. jobs report that sparked the early February stock-market selloff.

"U.S. Treasury yields are straddling historically significant technical levels even as markets are trying to second guess the Fed's hiking path and digest higher Treasury issuance (as a consequence of recent tax cuts) at the same time," they said. "It is therefore unsurprising that the pricing of risk in equities is being given another appraisal."

In fact, the VIX has never, at least in the last 12 years, been this sensitive to both real yields and long-term inflation expectations simultaneously, they said (see chart below).

Kumar and Cassot outline a number of other factors that point to a further rise in volatility.

These include climbing volatility in earnings, rising single-stock volatility, and the fact that volatility now appears to be back in sync with the corporate profit cycle.

The only factor pointing to lower volatility, they said, is strong and synchronized global economic growth. Periods of robust growth are expected to lead to better corporate earnings keeping a lid on volatility.

That said, while economic fundaments continue to warrant low volatility, the length of the business cycle should naturally prompt some concerns about the sustainability of growth, which would make it a "major surprise" if volatility fell back to 2017 levels, they said.

From MarketWatch