Weekly Market Outlook - The Rally is Saved in the Nick of Time, But...

Stocks logged a loss last week - the first in the past seven. And yet, even with the loss, they ended the week on a bullish foot, pivoting out of Wednesday's and Thursday's bearish move. Support at the 20-day moving average lines lent a helping hand.

So, the trend remains bullish, as unlikely as more gains may seem following a four-month, 14% advance. All the same, it's always wise to prepare for the worst even as you're assuming the best.

We'll look at both sides of the coin below, after running down this week's and last week's major economic news. This week is loaded with potential catalysts, for better or worse.

Economic Data

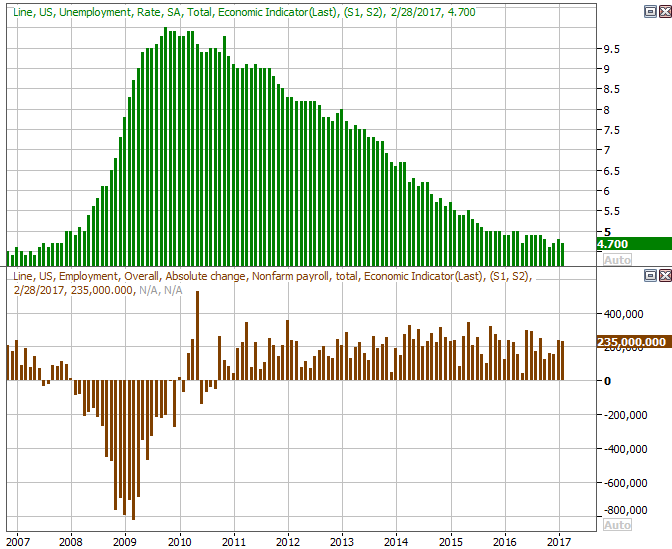

There's no doubt as to last week's biggest economic news... Friday's employment report from the Department of Labor. Then again, it wasn't too much of a surprise. We should have known after Wednesday's ADP payroll growth report (298,000 new jobs versus expectations of 180,000) and 40% reduction in planned job cuts for February -- following January's 39% decrease in planned layoffs -- that job growth was going to be strong. And, it was. The DOL said we added 235,000 new payrolls for last month, topping expectations of 188,000, and bringing the unemployment rate down from 4.8% to 4.7%. That's solid no matter how you slice it.

Unemployment Rate and Payroll Growth Charts

Source: Thomson Reuters

Though there was some other data posted last week, little of it besides the jobs-growth report is worth a closer look.

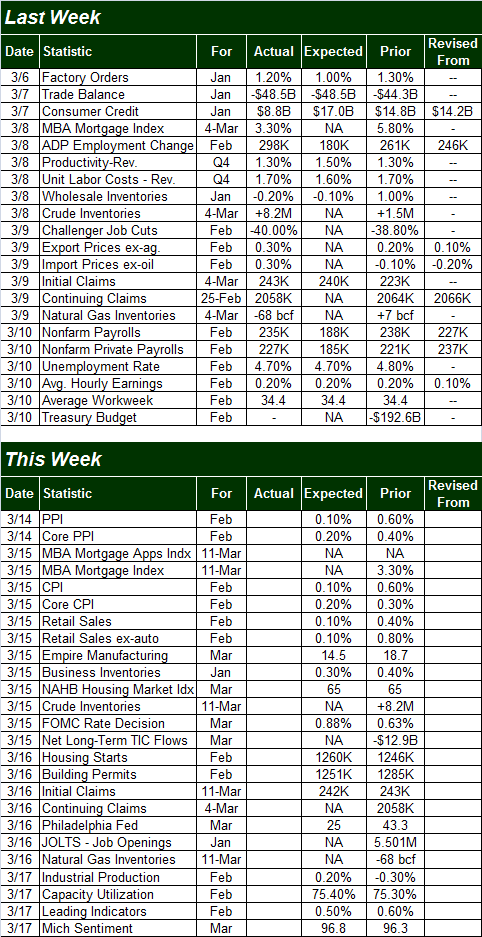

Economic Calendar

Source: Briefing.com

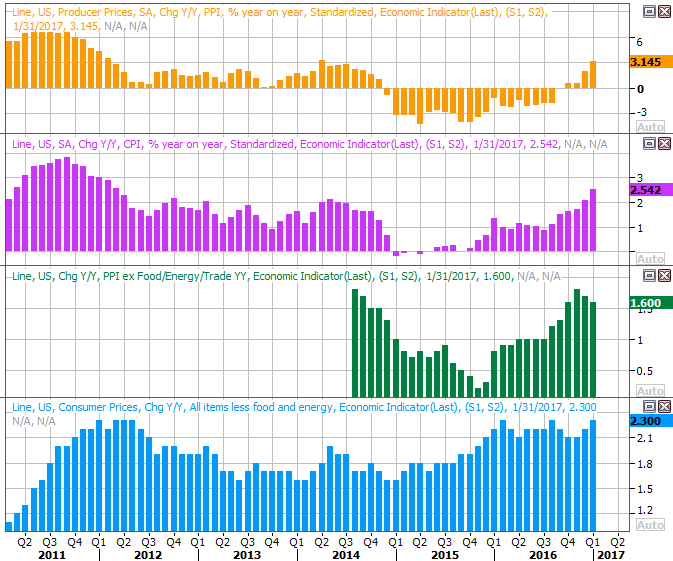

That's not the case for this week - there's a long list of items that needs to be previewed, beginning with February's inflation data. Last month's producer price inflation numbers are due on Tuesday, and on Wednesday we'll hear about February's consumer inflation. Both are expected to rise modestly (again), on a core as well as a non-core basis.

As you can see on the chart of the annualized data below, inflation rates are quickly racing out of control now. Part of that has to do with the fact that gas prices fell sharply a little over a year ago, and the year-over-year comparisons aren't as fortuitous any longer. It's not just gasoline that's driving the comparison higher though. We're seeing inflation from most categories.

Consumer and Producer Inflation Rate (Annualized) Charts

Source: Thomson Reuters

The Federal Reserve knows it needs to nip this in the bud, and right on cue, it will get its chance to do so on Wednesday. That's when the FOMC will have a scheduled chance to unveil any new changes to the Fed Funds Rate. The market's betting -- and betting big -- on a 1/4-point rate increase. That news is apt to rock the market either way.

Also this week we start a wave of real estate news that peaks next week. This week's entries into that log are February's housing starts and building permits. The experts are calling for a few more starts and a few less permits relative to January's data. We could use a shot in the arm here, though the broad still seems to be pointed upward.

Housing Starts and Building Permits Charts

Source: Thomson Reuters

Last but not least, although it largely goes ignored, Friday's capacity utilization data and industrial productivity data from the Federal Reserve is actually a rather big deal because it correlates so strongly with the long-term market. The bulk of the tepidness here since early 2015 has been rooted in crude oil's weakness. But, we should have seen at least a little more rebound in these numbers over the course of the past year or so.

Industrial Productivity and Capacity Utilization Charts

Source: Thomson Reuters

Economists are looking for a slight increase on both fronts this time around, and we need it... the bigger, the better. All of the consumer enthusiasm mustered since January will be hollow if we don't actually see factories and refineries put to more use.

Index Analysis

The confusion continues. Just on the brink of what could have been the first major pullback in weeks, the market's major indices managed to find support and rekindle the rally effort on Friday. A fluke? Maybe, but it's interesting that the volume behind the reversal effort.... wasn't too bad.

There are still concerns, not the least of which is the fact that the VIX (and to some extend the VXN) still seem to be broadly looking in the direction of higher highs even though they're not making them yet. Also, there's the sheer size of the rally since early November, which has yet to be supported by actual earnings growth. It's the bears who have to prove they're taking control, however, before we can truly assume the bullish trend is broken.

Just for the sake of variety, let's look at the daily chart of the NASDAQ Composite first today; it's where the buying volume actually grew in the upstroke from late last week. Just as bullish is the fact that it was the 20-day moving average line (blue) that sparked the bullishness when it as bumped into on Thursday. We can't ignore the fact that the bulls drew a line in the sand as the one place where they had the best shot at holding the line.

NASDAQ Composite Daily Chart

Chart created with TradeStation

It's more or less the same story for the S&P 500's daily chart, with one exception... the VIX is in an even better position than the VXN is to finally make a thrust to new highs. That's potentially bearish, but hardly overcomes the fact that the buyers ARE buying again (or were as of Friday anyway).

S&P 500 Daily Chart

Chart created with TradeStation

It's hardly a perfect bullish effort though. For starters, the MACD indicator is still in bearish territory, and the PercentR line is below 80. Remember, the PercentR line needs to move above the 80 level -- and stay there while the S&P 500 moves to new highs -- to confirm this very reliable bull/bear signal.

S&P 500 Daily Chart, With PercentR and MACD

Chart created with TradeStation

With all of that being said, while the undertow is bullish, any trade to that effect is mostly a bit of a coin toss. That's because on Wednesday the Federal Reserve is almost assuredly going to raise interest rates. This is a binary event if there ever was one. On the one hand, rising rates are bad for bond values and bad for commodities, which in turn is good for stocks (money always flows to the best, relatively, bet). On the other hand, investors could be concerned that higher interest rates will stifle the economic growth we've enjoyed of late, and with more rate hikes to come we could find earnings growth hitting a wall.

Which of the two we'll see largely depends on what kind of mood traders are in when the time comes. On balance, however, we see more downside risk than upside potential either way. Even a bullish response to the news could set up a "sell the news" (for profit-taking) effect. Just tread lightly here. The VIX and the 20-day moving average line are still you're ultimate bearish cues.