Style and Market Cap Rotation Starting to Take Shape

This year hasn't been a great one for value stocks, nor has it been a great one for small cap growth stocks. But, mid caps and large caps from the growth side of the table -- thanks to a ton of bullishness from the FAANG stocks -- have led the way. It looks like the tide is turning for all of those arenas though. That is to say, yesterday's laggards are starting to lead, and yesterday's leaders are starting to lag... with "yesterday" meaning since the beginning of the year.

It's not a complicated idea to embrace. Investors tend to seek out certain hot spots, and they'll forego picks from certain slivers of the market (or even sell their existing holdings) to gain exposure to those hottest picks. Nothing lasts forever though, and we're now seeing hints that investors are starting to migrate out of the recent winners and looking to go bargain shopping and redirect that money into this year's more disappointing performers. Those disappointments are large cap and mid cap value names, and small cap value names in particular.

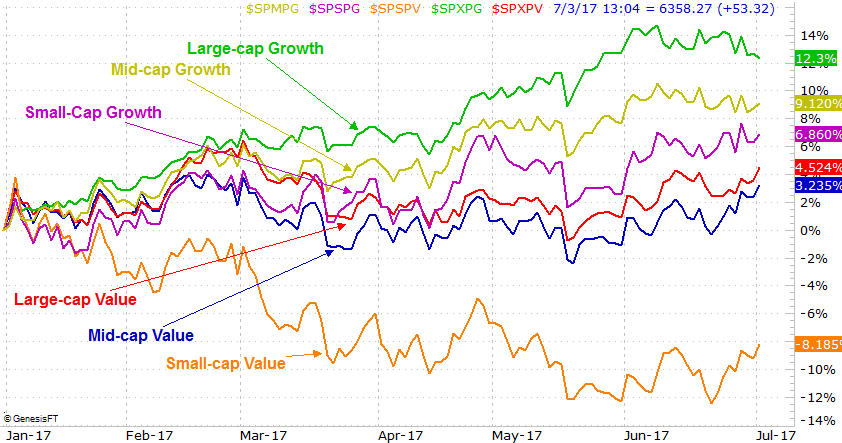

How do we know? Just be review of a simple visualization.

The performance-comparison chart below tells the story. After soaring in early November, small cap value names have seen nothing but profit-taking since early January. Conversely, large cap growth names have led the way on the heels of the aforementioned large-cap tech rally. Take a closer look at the chart, however. Since early June, large cap and mid cap growth stocks have peeled back, while all three value groups have woken up and only in the past week have tiptoed into new multi-week high territory. They're gaining at the expense of the previous winners.

Wedged in the middle of all of these performances is small cap growth, which is still going strong at a sustainable pace. It's a group that validates the idea that slow and steady wins the race.

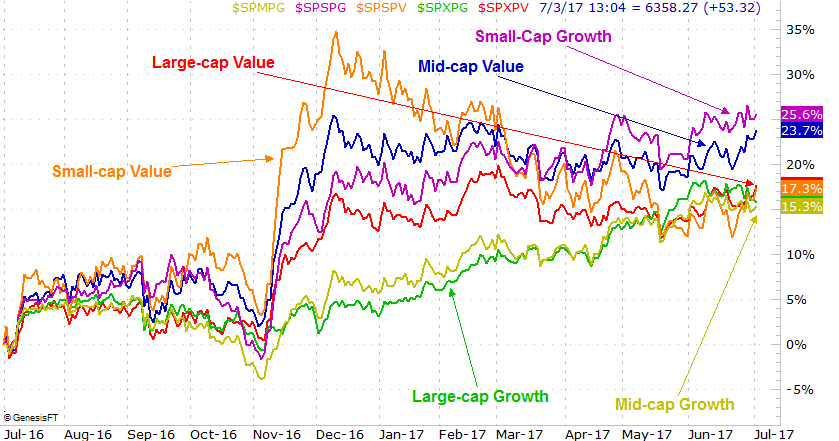

Underscoring the "slow and steady" theory is a zoomed out look at the same six slivers of the market, going back to the beginning of July of 2016. In this timeframe small cap growth is still outperforming all other groups. It's also in this time that the recent leadership -- until June -- of large cap and mid cap growth stocks made sense. Until December, they were notable laggards. This longer-term timeframe calls into question just how much we should expect large and mid cap growth names to peel back. Everything else was oddly overbought by December, so the year-to-date weakness can't be too much of a surprise. Indeed, from this perspective one could argue we should already be buying large cap growth names again, and avoiding value.

But, that's not the assessment here. This time around, as usual, we should respond to what the market is doing right now, and trade that way until we have clear evidence those trends aren't panning out. Otherwise we risk waiting too long to make a move.