Can Stocks Actually Justify Their Lofty Valuations?

Is the market fairly valued at a trailing P/E of 21.74? That's a matter up to individual investors to decide for themselves. Though many say the trailing valuation isn't rational, the forward-looking P/E of 17.7 make stock's "worth it" in light of the fact that interest rates are so oddly low at this time. Besides, at the pace earnings are projected to grow over the course of the coming year and a half, stocks deserve their premium.

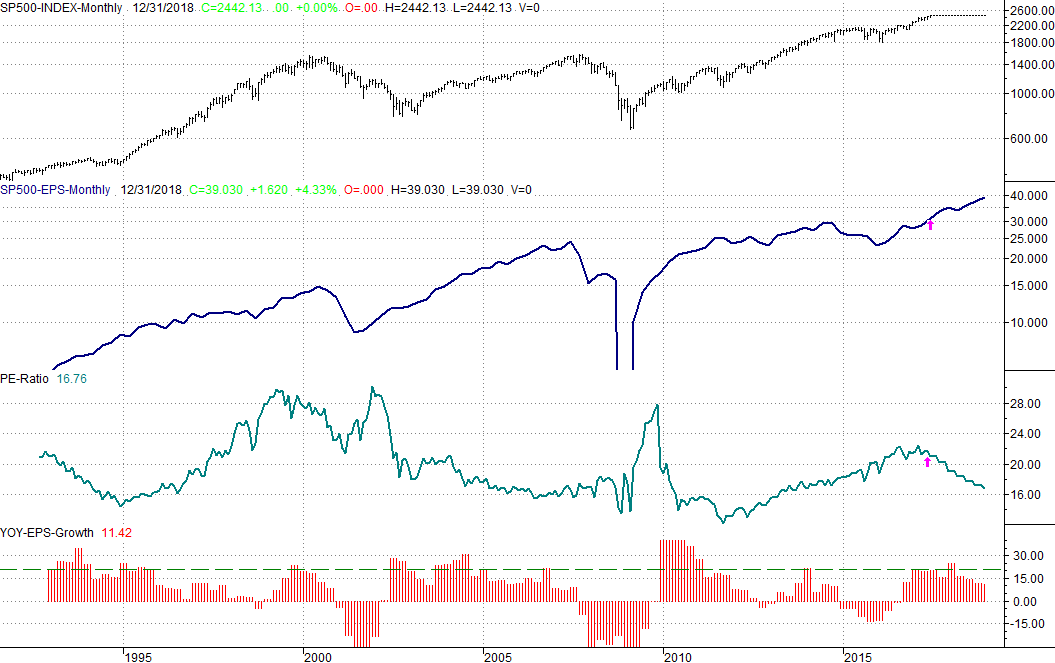

As is usually the case, a picture says a thousand words. So, to help traders at least get a firm grip on the "worth it or not?" question at this time, we've plotted along with a monthly chart of the S&P 500 its trailing per-share and projected per-share profits, its trailing and projected P/E ratio, and its trailing and projected year-over-year earnings growth pace.

The pink arrows mark where we are as of June, 2017.

Truth be told, it's a little difficult to ascertain where the S&P 500's trailing P/E should be. Never mind the mental adjustment that has to be made to factor in the era of low interest rates. Over the course of the past two decades, we've rarely seen a normal environment. Earnings have always been rising or falling, and the market's typical P/E level has been a moving target.

Still, what we can more or less determine is that in late-stage bull markets like we saw between 2005 and 2007, the S&P 500's P/E ranged between 16 and 18. That's the most comparable scenario to our present situation, though interest rates were sky-high then.

Broadly speaking, the market is overvalued, though that doesn't necessarily mean a pullback is in the cards right away; investors have a knack for doing the inexplicable from time to time.

Perhaps the most noteworthy aspect of the chart below isn't the valuation metric, but instead, the projected pace of earnings growth for the rest of 2017 and all the way into the end of 2018. Though not downright heroic on a year-over-year basis, the raw earnings projections is out of character -- bullishly -- compared to is historical pace. The pros are calling for a parabolic rise in marketwide earnings, even without explaining exactly why they think the next year and a half will drive growth at a clip better than we saw in 2005,and even in the late-90's.

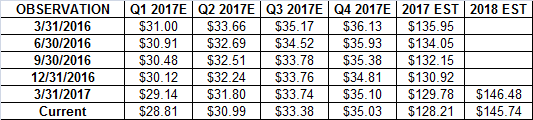

To that end, take a look at the table below, which logs how these projected earnings estimates change over time. Over the course of the past several economic cycles, the tendency is for them to be ratcheted down as the time for measuring them approaches.

In other words, if traders are only justifying the trailing P/E of 21.7 because of the forward-looking one of 17.7, there's a wake-up call in the works -- the S&P 500 probably isn't going to reach those lofty targets.

Again, that doesn't inherently mean stocks are doomed to tumble now. Stocks have been overbought and overvalued for some time now, and it hasn't mattered yet. As long as traders collectively want the market to move higher and are willing to overlook the risk of faulty earnings projections, stocks will trek higher. The market will eventually reflect actual results rather than wishes though, meaning this piper is going to have to be paid sometime.