On Thursday, our Options Shark trading advisory [1] locked in a 57% gain on some Bed, Bath & Beyond (BBBY) puts… one of several nice winning trades the BigTrends team has made of late. Though we issue far more trading ideas than we could ever review — as a learning tool — this is one worth going back and taking a closer look at. There's a lot to be learned from it.

First and foremost, the Bad, Bath & Beyond put trade is a fine example of how one can meaningfully use gamma in their option trading.

Most option traders are familiar with the so-called Greeks like delta and theta. The former is how much the value of an option changes with every $1.00 change in the price of the underlying stock or index, while the latter is just a measure of how much value an option loses any given day just due to the passage of time.

Those are important tools to be sure, but just as important even if more difficult to get a grip on is gamma, which is a measure of how much a certain option's delta will change as the price of the underlying stock changes. Ideally, you'd want to buy an option with a relatively high gamma in hopes that your delta rises rapidly as the trade progresses. That is to say, you want to buy options that become even more responsive — the delta increases — as the trade moves in your favor.

The catch: Generally speaking, you usually don't see an option with a high gamma and also the higher delta you'd want, as the two tend to go hand in hand. With some careful searching though, you can find an option with a relatively high gamma and a relatively high delta that's positioned to gain in value with a just a fairly modest favorable move from the underlying stock. The Bed Bath & Beyond August Monthly (08/18) 32.5 puts (BBBY 170818P32.5) fit the bill perfectly on Monday.

The only effective way to illustrate this idea is by showing you the key Greeks for all the put options available to us at the time [we already planned on buying two-week options, but that was a matter determined by the chart signal rather than the Greeks]. Here's a look at our choices as of Monday.

[2]

[2]

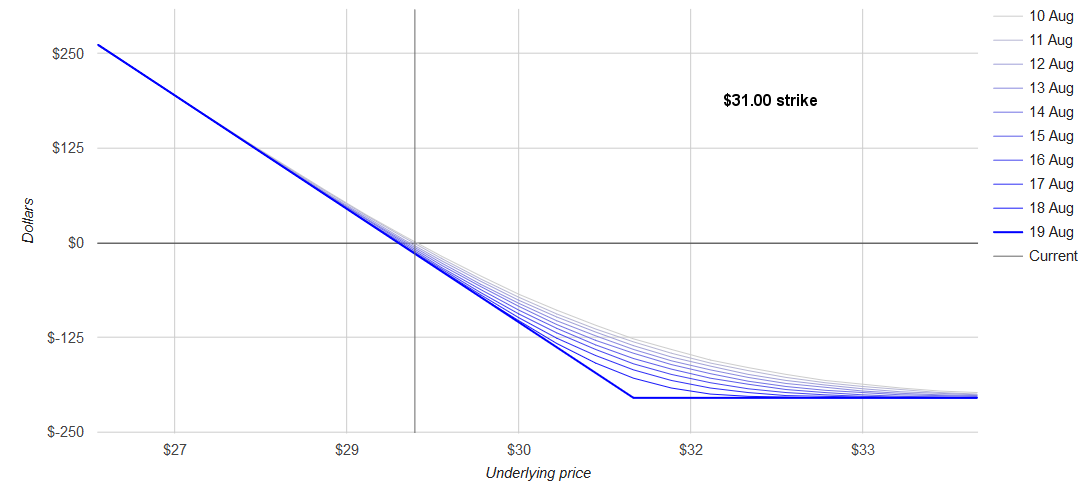

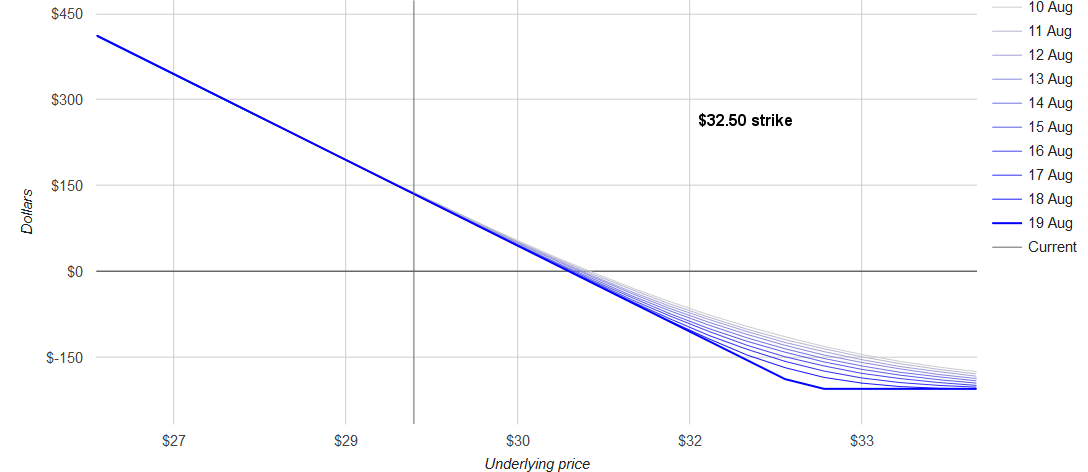

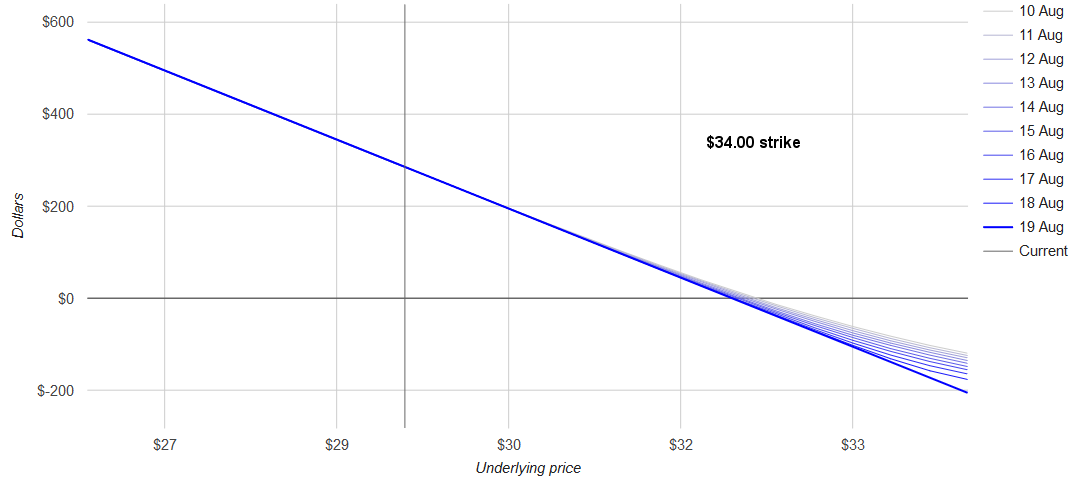

Obviously there were options with higher gammas or higher deltas, but they came at a rather steep price or were too risky. From a risk/reward perspective, the 32.50 puts made the most sense for us, considering all the other factors we had to consider. We know this because we visualized all the likely scenarios for each of the options in question. We won't show them all to you, but we will give you the profit-and-loss graph for the 31.0 puts, the 32.50 puts we bought, and the 34.0 puts. The graphical representations illustrate how rapidly or slowly the value of those options change relative to the movement of BBBY itself.

[3]

[3]

[4]

[4]

[5]

[5]

The $34 puts were the safest, but offered limited upside. The $31 puts offered more upside, but were riskier. The happy medium was the $32.50 strike, where the profit and loss scenarios (all the blue lines) for each price and each date were not too far away from one another, but also not too far apart. And that's where gamma is quietly, secretly factored in….

Profit and loss possibilities like the ones shown above are often seen as a function of delta and theta, and rightfully so. Just as important in this case, though, was gamma. Here's where gamma values were three days after entering the trade, when we were making an exit of the Bed, Bath & Beyond puts.

[2]

The gamma on the 32.50 puts has essentially fallen to zero, but only because the delta on those puts has reached its maximum level, gaining a dollar in per-contract value for every dollar BBBY loses in value. There's no room for delta to get any better. That's what we wanted.

With that as the backdrop, one point has to be made – while a gamma value of 0.119 seems like a low value for an option Greek, that's actually pretty high by gamma standards… at least for options that aren't too risky to bother buying. It's also worth noting that changes in gamma may already be built into any profit and loss calculators like the one we used to make our P&L charts above; you may be using gamma without even knowing it.

If it all still seems too esoteric to use, (1) you're not alone, and (2) don't worry about it.

Gamma isn't an easy idea to incorporate into your thinking when picking options. It's also not always easy to find the information or build a pricing model around it. A few paper/hypothetical trades will help you get a grip in the idea. Just bear in mind that you'd prefer a higher gamma value than lower gamma value for the outright purchase of calls and puts; spreads may be a different story. Higher gammas work particularly well for our Options Shark service where the holding periods are a few days and the signals we use are looking for relatively small moves…. where gamma can mean the most.

If you'd like to learn more about gamma, and learn by doing, the Options Shark trading advisory is a perfect chance to learn while you earn. The trades recommended by our Options Shark service use our proprietary interpretation of the %R indicator as well as Price Headley's acceleration bands, ferreting out the trade-worthy moves most others overlook. Go here [1] to learn more about and sign up for the Options Shark newsletter.