– Short interest for major ETFs is at a nearly five-year low –

By Ryan Vlastelica, MarketWatch [1]

The going has been good in the U.S. stock market, and investors, perhaps to their eventual regret, don’t seem to expect that to end soon.

Amid repeated records for the major indexes, historically low volatility, and a nearly unprecedented length of time since the S&P 500 has dipped even 5%—the kind of mild decline that is typically quite common—market participants have pulled back on any kind of security or strategy that could act as an offset against a market retreat, apparently viewing the current environment as one where insurance against losses is unnecessary.

“Protection is dead. People have been hedging for years and it hasn’t been profitable, so they’re throwing in the towel,” said Michael Matousek, head trader at U.S. Global Investors Inc., who added that his firm’s options desk had been seeing lower and lower demand. “Things are getting quieter and quieter over there; basically no one is buying protective puts.”

Put options are purchased when an investor thinks the price of an individual security will fall.

Another popular way to hedge a portfolio is to short exchange-traded funds that track a major part of the equity market. This strategy has essentially dried up amid the market’s uninterrupted bull rally.

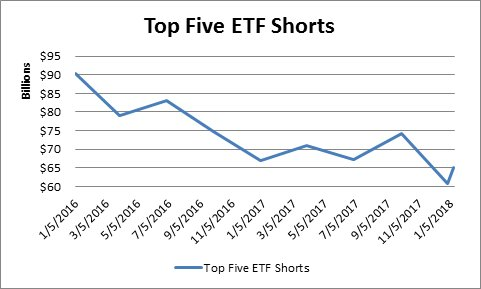

Ihor Dusaniwsky, managing director for predictive analytics at S3 Partners LLC, noted that short interest on the five most commonly shorted ETFs had dropped precipitously since the start of 2016, falling 28% to $65.1 billion. The last time short interest on these funds was this low was in April 2013.

[2]

[2]

Chart courtesy S3 Partners

“We are definitely seeing a pattern of less portfolio hedging,” he wrote in emailed comments to MarketWatch. “It looks like institutional investors are putting on smaller hedges, either due to a more positive market outlook or due to a severe drop in market volatility.” He added that hedge funds were also reducing their ETF hedges.

The five ETFs are: the SPDR S&P 500 ETF Trust which tracks the S&P 500; the iShares Russell 2000 ETF which tracks small-cap equities; the PowerShares QQQ Trust which tracks the components of the Nasdaq-100; the iShares MSCI Emerging Markets ETF; and the iShares iBoxx $ High Yield Corporate Bond ETF for “junk” bonds.

Over the past two weeks of December, the most recent period for which there is data, short interest for Nasdaq Global Market securities fell 6.1%, according to the exchange’s data. For the NYSE Group—which includes the New York Stock Exchange, NYSE Arca, and NYSE MKT—short interest fell 7.2% on a sequential basis, based on the most recent settlement data at the end of 2017.

On a similar note, inverse ETFs—which fall when the index they track rises, and vice-versa—have been seeing outflows of late. Roughly $280.6 million has been pulled from the ProShares Short S&P 500 ETF over the past month, bringing its assets to about $1.2 billion, its lowest level since May 2009.

The ProShares Short QQQ has had outflows of $55.9 million over the past month while the ProShares Short Dow30 which offers inverse exposure to the Dow Jones Industrial Average has had $14 million in outflows over the same period.

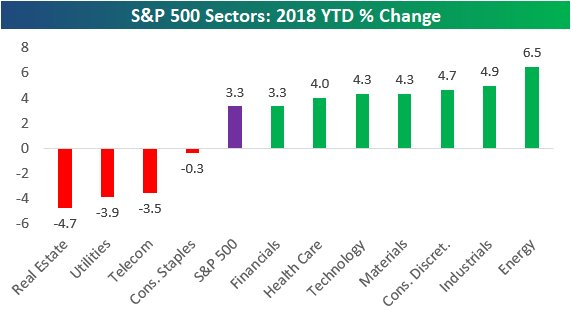

Even the more defensive parts of the equity market have been out of favor this year. Bespoke Investment Group tweeted that 2018 was a “perfect ‘risk on’ rally so far,” noting that “all the defensive sectors are down and all the cyclicals are up, with the broad S&P 500 right in the middle.”

[3]

[3]

Courtesy Bespoke Investment Group

Cyclical groups like energy and consumer discretionary are seen as being more tied to the pace of overall economic growth, whereas defensive industries like utilities and telecommunications tend to be favored in periods of economic uncertainty as they have more stable—if lower—levels of growth.

Defensive stocks are sometimes viewed as “bond proxies,” as they pay higher dividends than the overall market. (The yield for utility stocks is 3.47%, compared with 1.73% for the overall S&P) This issue has come into play in recent trading, as the yield on the 10-year Treasury rose to its highest level in nearly a year, which makes such stocks less attractive for this purpose.

These trends are occurring at a time when the global economy looks strong on a lot of metrics. Global stocks haven’t had a down month since October 2016, thanks to a world-wide improvement in corporate profits. In the U.S., 2017 earnings are seen growing at their fastest rate since 2011. Separately, the labor market and other economic indicators are at strong levels, with some data at records or multiyear highs, and inflation is low at a time when the Federal Reserve is only gradually raising interest rates.

These attributes have led to a level of market optimism that some investors contend is shading into euphoria. Retail investors, according to a recent Deutsche Bank analysis of consumer sentiment data, view the current environment as “the best time ever to invest in the market.” TD Ameritrade reported that its retail clients ended 2017 with record levels of market exposure.

Last month, Morgan Stanley wrote that cash balances for Charles Schwab clients reached their lowest level on record in the third quarter, opining that retail investors “can’t stay away” from stocks. Institutional investors, meanwhile, were “loading the boat on risk,” with “long/short net and gross leverage as high as we have ever seen it.”

The AAII investor sentiment survey recently hit a seven-year high, though it pulled back in the latest week.

“The underlying fundamentals are strong and the trend is still higher, but sentiment is excessive by historical standards, and in the past sentiment at these levels has represented a warning sign. It would be wise to pay attention,” said David Joy, chief market strategist at Ameriprise Financial. “We’ll have a correction at some point—when, who knows—and you’ll want to have downside protection when it happens.”

U.S. Global’s Matousek struck a similar note of caution: “When confidence builds to this kind of euphoric point, the market has a way of humbling you.”

From MarketWatch [1]