Market forces are playing the biggest role in the dollar/yuan exchange rate

By Avi Gilburt and Mike Golembesky, MarketWatch [1]

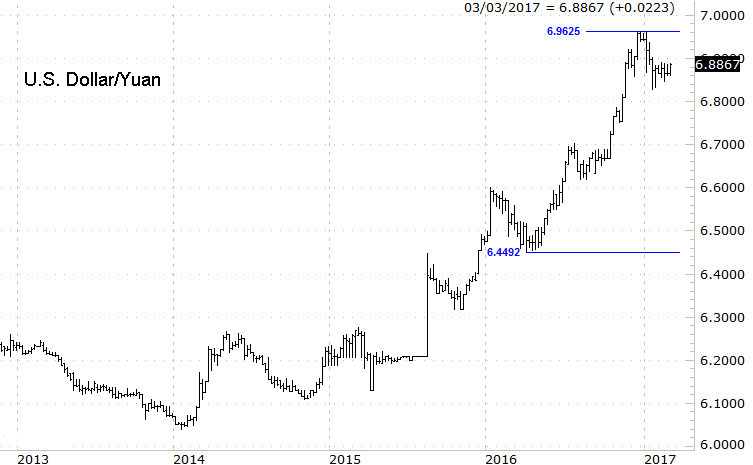

Last year at around this time, the exchange rate on the U.S. dollar/Chinese yuan was at 6.44 yuan to 1 dollar. As of this writing, the exchange rate has risen to just over 6.87 yuan to 1 dollar. That’s a decline of close to 7% for the yuan.

Moreover, the move was almost in a straight line, with few retracements since the March 2016 local bottom at 6.44. This price action came as no surprise to us at ElliottWaveTrader.net, as the path of the yuan has followed the prediction that we had laid out in the second of a series of articles, the last one published a year ago this month

[2]

[2]

We had first written about the price of the yuan in August 2015. For those who may remember, this was shortly after the yuan suffered a sharp depreciation over two days. At the time, the pundits were proclaiming that China was intentionally devaluing its currency to help bolster a slowing economy.

That, of course, made for a great headline, as who wouldn’t want to read about a plan by the “evil” Chinese government to instigate a currency war against Western powers. Unfortunately, the pundits overlooked the facts that debunked their entire premise, and instead went with the story that would be sure to get more attention.

The simple fact of the matter was that the Chinese government was not behind the devaluation of the yuan. The real driver was the greater market forces or, more simply put, market sentiment. This was clearly evident by looking at the massive liquidation that had been occurring in China’s foreign currency reserves.

Eventually the financial pundits accepted the fact that the People’s Bank of China was indeed attempting to bolster a market-weakened yuan and was not the cause behind the currency’s fall. We noted that in our third article: “[I]t now seems that after dumping $760 billion of their foreign-currency reserves, the pundits have finally accepted that, in fact, China is not actively trying to devalue their currency, but is attempting to do just opposite and support it by using their foreign exchange reserves to purchase more yuan.”

China has continued to throw more of its foreign exchange reserves at the yuan, as those reserves are now $1 trillion below their $4 trillion high in 2014. This continued expenditure has done little to stop the market from pushing the yuan lower.

Looking back at all three of the articles we’ve written on the Chinese yuan, you will notice that the price of the dollar/yuan has followed the path that we had laid out exceptionally well. The most recent high in February of this year came quite close to the larger degree 38.2 retrace of the very long term move down off of the highs that were struck all the way back in the early 2000s. So, although we still may have another high to go prior to seeing a multi-year top in the dollar/yuan, we should be getting very close to having a fairly significant top in place.

After the dollar/yuan does make a more significant top, it is quite probable that we will see a prolonged and very sloppy corrective wave structure that could take us well into the 2020s before a larger degree bottom is seen. As the buyers and sellers of the yuan will likely be quite equal at this time, we may very well see a period of little to no direct intervention by the People’s Bank of China. So, while the “manipulation” is still likely occurring as of this writing, we may be approaching the point, for the first time in several decades, where there truly is no “manipulation” by China in the price of its currency. This, of course, is not by choice but simply because the greater forces of the market are leaving China with no other choice.

Courtesy of MarketWatch [3]