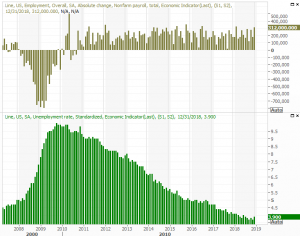

The December jobs report was great, as measured by the raw number of payrolls created last month. All told, the 312,000 new jobs added in December was the best tally since February, and the second-best progress seen since mid-2016.

If instead your yardstick is the unemployment rate, the picture isn't quite as encouraging. Despite the huge number of newly-created payrolls, the unemployment rate ticked up from 3.7% to 3.9%, even shocking most experts.

Yet, overall, the report is being viewed as a resounding victory. What gives?

It's an employment report that most definitely merits a closer look at the details that generally get skipped on the first Friday of every month, as they usually don't add much perspective to the matter. This is a case though, in our current and unusual situation, where the proverbial 'rest of the story' rectifies the mixed message.

Yes, job growth was incredible, but the unemployment rate pushed higher anyway.

[1]

[1]

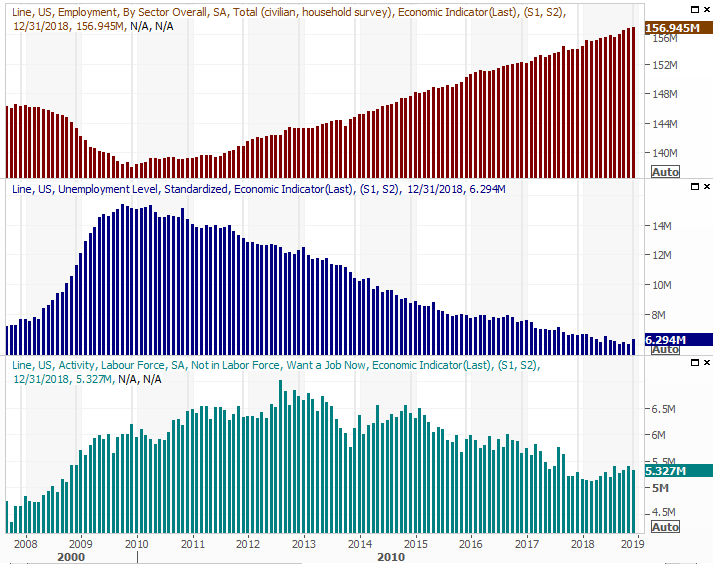

That basic data is rounded out (and partially explained) by a cursory look at the underlying numbers. That is, how many people are working, how many people in the U.S. are officially unemployed, and how many people in the United States aren't technically counted as being unemployed – because they're not receiving unemployment benefits – but want a job anyway? As of the end of last month, a record-breaking 156.95 million U.S. residents have jobs, and the number of unofficially-unemployed people actually fell from 5.4 million to 5.33 million. But, the number of people who've been recently displaced from the workforce actually ticked up, from 6.0 million to 6.3 million.

[2]

[2]

It's this last group – the 6.3 million people receiving official unemployment benefits – that explains the increased unemployment rate… almost. The 312,000 new jobs were largely filled by people who weren't officially unemployed, or who had only recently joined (or re-joined) the work force. The unemployment rate, however, is calculated by dividing the 6.3 million unemployed people by the total number of people actively in the workforce… working or not. That number got a whole lot bigger last month.

That's not a guess either.

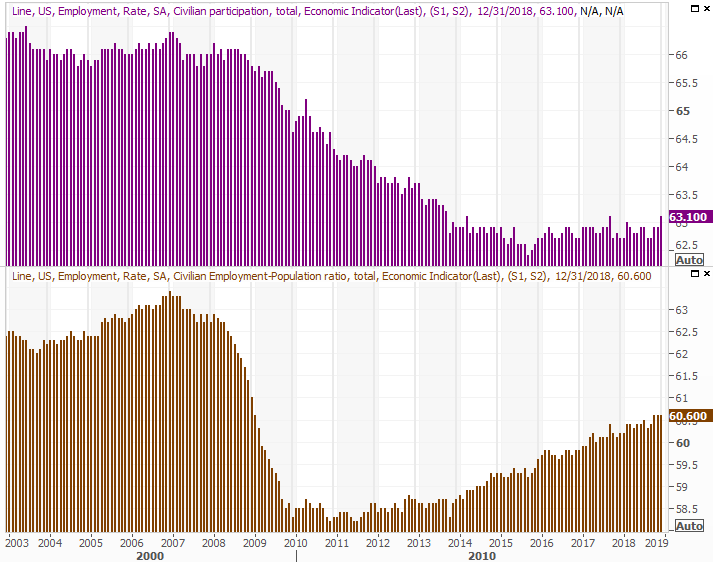

The final piece of the puzzle is a measurement of how much of the U.S. population is in the workforce, though not necessarily working, and how much of the population is employed. The latter figure is 60.6%, the same as November's and October's measure. The former, however, jumped from 62.9% in November to a multi-year high tie of 63.1% in December. That is to say, 63.1% of the nation's population either has a job, or legitimately wants one.

[3]

[3]

The underpinnings for the noteworthy surge in the labor force participation rate are never entirely clear. Hope is one reason – reasonable hope that a job can be attained at all draws people off the sidelines. To that end, the fact that employment among people only with a high-school education is at multi-decade highs, and paychecks are getting larger even for inexperienced workers. That's luring people into the workplace that may never have thought about seeking employment.

Another reason the size of the nation's labor pool can expand is a wave of college graduations, which can displace workers that may already have jobs. That's not likely a major source of the labor pool's growth this time around though, as even December's graduates wouldn't start to disrupt other job-seekers until this month.

Regardless of the reason(s), clearly the workforce as a percentage of the population is growing again, and most of them are finding employment.

Finally, and just as important, wages continue to improve. Hourly pay rates were up 3.2% year-over-year, moving further into record-high territory and matching the highest year-over-year growth since the economy came out of the subprime mortgage meltdown. While wage growth is generally 'good,' this is a pace that points to uncomfortable inflation that the Fed may want to keep in check sooner than later.

The length of the average workweek, however, didn't shrink in response. It edged up just a bit.

The $64,000 question is, does the strong job market and the subsequent increase in pay point to brewing hawkishness from the Federal Reserve that poses a risk to economic expansion? Probably not. Although anything is possible, most matters remain in something of a sweet spot where growth is robust, but not dangerous. The current annualized consumer inflation rate stands at a modest 2.2%, with or without food and energy costs factored in. And, the inflation rate has actually been edging lower rather than higher since July. The Fed doesn't have to think or act too aggressively here.

All in all, it's another good jobs report. Indeed, we'd give it an A- it may not seem like it deserves on the surface. It gets extra credit for balancing out the worrisome parts with data that's actually as it should be. That is, most people who want jobs are getting them, and people who didn't exactly want jobs are starting to want them.

The slight uptick in the total number of unemployed people is apt to be a temporary headwind prompted by inconveniently timed layoffs. The job market should soak that excess up quickly enough.