Not that the Federal Reserve hadn't already made up its mind about a rate-hike later today, but to the extent any last minute data is capable of altering that choice, this week's inflation and retail sales data won't give Fed Chairperson Janet Yellen any pause… and neither data set was particularly, unusually strong. Indeed, both data sets were tepid by comparison. They did advance as expected though, and that's enough to keep the green light lit up on the Fed's impending announcement.

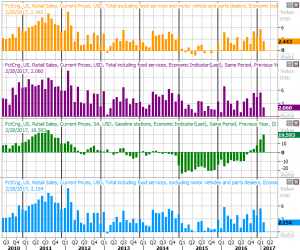

On Wednesday morning, last month's retail sales numbers were unveiled. On a month-to-month basis they were up 0.2% with or without automobiles factored in, versus only a 0.1% rise expected for both. One a more meaningful year-over-year basis, retail spending was up 2.1% overall, and higher by 2.4% without taking restaurants and automobiles into account. Retail sales at gas stations — which includes spending on gasoline — jumped 19.6%, spurring much of last month's overall increase.

[1]

[1]

Still, the data suggests we saw something of a slow-down last month. It just wasn't enough of a slow-down to put the brakes on any of the Federal Reserve's plans to drive interest rates higher.

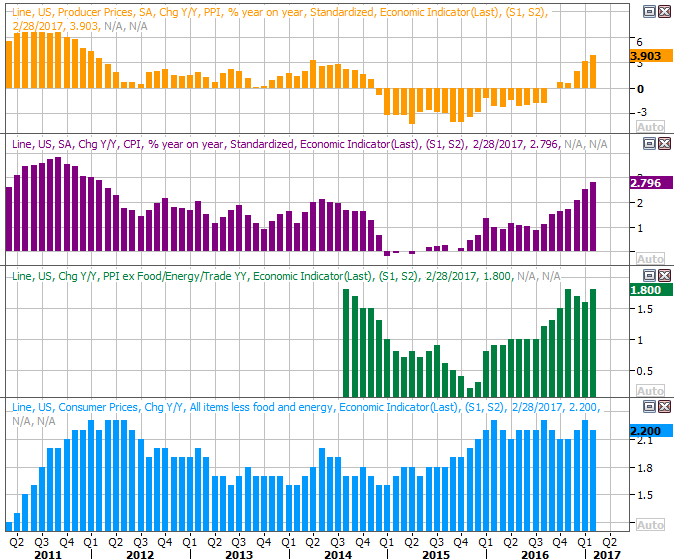

As for inflation, the month-to-month change was moderate. For consumers, prices grew 0.1% overall, and 0.2% when stripping out the volatile costs of food and gasoline. Both were in line with expectations. For producers (factories and assemblers or packagers), costs were up 0.3% on a core as well as a non-core basis. Economists were expecting a 0.1% increase on a broad basis, and a 0.2% rise without food and energy costs factored in.

As was the case with retail sales, the year-over-year inflation figure means more, and we're seeing plenty of it in that timeframe. The annualized producer inflation rate stands at 3.9% overall, and 1.8% on a core basis. The consumer inflation rate is now 2.8%, and is 2.2% when removing the effects of food and gas cost changes. In all cases, that's enough to impose a rate hike. In all cases though, the trend is more concerning — or should be, anyway — to Yellen than the current levels. This rise has to be nipped in the bud, sooner than later.

[2]

[2]

Nothing is ever etched in stone, of course. It's entirely possible the Fed could opt to hold rates steady; for better or worse the tail wags the dog rather than the dog wagging the tail in the modern politically-driven economy. On the face of things though, the Fed just got the last thumbs up it may have needed to put another rate hike in place. Assuming that doesn't cool inflation or retail spending in the aftermath, we're still due for two more rate hikes after today's before 2017 is over.