Though there's certainly not a shortage of bulls out there pounding the table about stocks, there's also more than a handful of doubters that say the market has been too hot for its own good — a pullback from here is inevitable.

The debate begs the question though… how overbought is too much, and where does the, oh, say the S&P 500 stand right now compared to where it might normally be at this point? As it turns out, the year-to-date performance, though decidedly bullish, isn't unusual or impossible to add to.

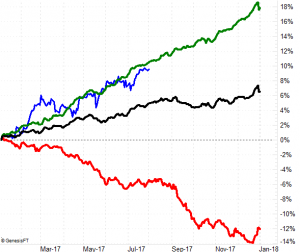

The graphic below tells the story. The blue line (the one that doesn't extend all the way to the right side of the graph) is where the S&P 500 is as of right now, up 9.5% since the end of the year. That's above the normal gain the index might dish out in the average year (black), which is usually a 5.3% gain at this time. But, as you can also see, some year were very, very bad. That's what the red line at the bottom plots… the average performance path of the S&P 500 when it posts a loss for the full year.

[1]

[1]

The green line above all the other lines on the chart is the average performance track for the index when it makes a gain for the full year. As you can see, there's nothing all that unusual about this year's performance to-date, assuming we're still in a bull market that will leave the index higher at the end of the year than where it started it.

Obviously past performance is no guarantee of future results. On the other hand, inasmuch as the data looks at the entire multi-decade performance of the S&P 500, it would be naive to at least not respect the historical tendencies.

The flipside: While the market may not be technically overextended, that doesn't inherently mean the rally is fundamentally supported.

As of the most recent look, the S&P 500 is trading at a trailing P/E of 21.3 and a forward-looking P/E of 18.1. Both are abnormally high, though investors are willing to pay a premium as a sort of bet on Trump, and a bet in his tax plan in particular. The only real potential risk in that mindset — though it's not an insignificant one — is simply that stock prices already reflect tax reform, and as such won't necessarily edge any higher should that legislative action happen. Indeed, there's the risk of a "sell the news" mentality taking over.

We can't think or trade presumptively though — only preparedly. In other words, with bullish winds still technically blowing, we'll have to look in that direction until we have clear evidence we can't afford to do so.