5 Stock Picks For 2015

by Michael Fowlkes

With 2014 nearing its end, traders everywhere are starting to think ahead to the New Year. This year's stock market performance was not nearly as impressive as last year, but it has been positive, and the major indices are poised to close out the year near their highs.

Although the overall trend has been positive, it was not all smooth sailing through the year. The markets ran into selling pressure mid-summer and then again towards the end of the summer, however both times bulls rushed in pretty quickly to push the major indices higher. As a result, traders are optimistic regarding the future, but it clearly shows that the slightest bit of bad news will be enough to rattle the markets and drive stocks lower.

Taking all of this into consideration, I would advise staying in the market, but taking a more cautious approach to which stocks you hold moving forward. There are real concerns over slowing growth in China, economic hardships in Europe, and rising interest rates in the U.S.

Oil prices have been weak, and OPEC's recent decision to keep output unchanged is likely to keep oil prices relatively low for the foreseeable future. This will help certain sectors, most notably transportation stocks since they have such large fuel expenses, and retailers since consumers will have more disposable income to spend.

Consumer confidence is back to pre-recession levels, which is a major bullish indicator for the nation as we head into 2015. I am bullish on the markets as a whole, and in particular the following five stocks, which I will definitely own in 2015.

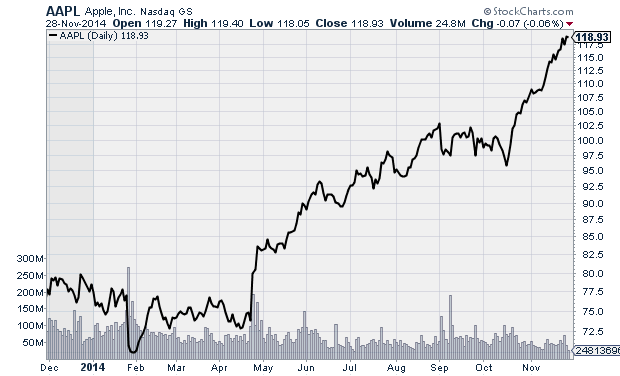

Apple (AAPL)

I find myself recommending Apple (AAPL) a lot, and I will once again mention AAPL as a stock that I will definitely own in 2015. The company has a lot going for it right now. Not only has the iPhone 6 launch been a massive success, I expect that holiday sales of the new smartphones will be huge. In addition to the iPhone's success, the company is getting ready to begin selling its highly anticipated Apple Watch, which has the potential to become a large, and vital, new revenue stream for the company. The company has already unveiled the device, and while critics and fans have varying opinions, there is little doubt that it will be a big hit among hardcore Apple fans. Whether it goes mainstream and hits a mass audience remains to be seen, and will depend greatly on the software community building a "killer app" that makes the device a must have. Regardless, it will find initial success, and should keep strength under the stock. The company also is trying to revolutionize digital payments with Apple Pay. If the service turns out to be a huge success it could create a tremendous revenue stream for the company, which will earn a fee on each transaction. Banks generate around $40 billion a year in transaction fees, and if Apple can tap even a very small amount of that market, it will keep the stock pushing higher.

AAPL Daily Chart

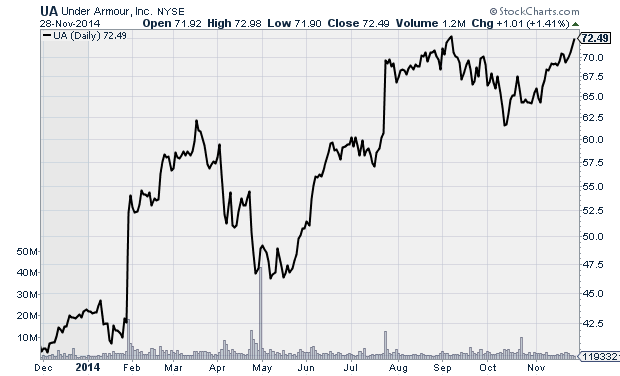

Under Armor (UA)

The retail sector in general should benefit from improved consumer sentiment, which is currently back to its pre-recession levels, but athletic retailers in particular appear well positioned moving forward. I really like Under Armor (UA) in this sector. This is primarily a result of the new fashion trend known as " athleisure ". The idea behind " athleisure" is that shoppers, most notably female shoppers, are opting to wear clothes that function both as athletic wear, and leisure wear. The trend is easy to spot. Walk into any shopping mall or grocery store and you will likely spot someone wearing yoga pants or a comfy sweatshirt. Not only are these clothes comfortable to wear, but they are now fashionably acceptable anywhere, not just the gym. This fashion shift has benefited all the major athletic retailers including Under Armor and Nike (NKE). Both companies have shown strength, but what really separates Under Armor is that the company has a lot of growth potential internationally, whereas Nike is already a global leader in athletic apparel and accessories. Looking to 2015, analysts have forecast Under Armor to grow earnings by 26%, and while the company has a high P/E ratio of 86, Wall Street appears willing to keep the stock near record levels in anticipation of the huge earnings growth that it believes will come in the future.

UA Daily Chart

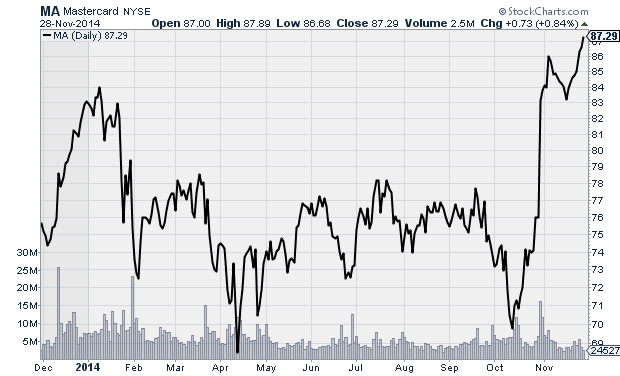

MasterCard (MA)

Payment processor MasterCard (MA) is yet another play on the strength in consumer confidence. Strong consumer confidence is going to lead to higher retail sales, and MasterCard will handle a large share of those transactions. After being stuck in a sideways pattern for the majority of the year, MA shares accelerated at the end of October following a better-than-expected third-quarter report, in which the company topped estimates on both the top and bottom lines. Looking ahead to next year, analysts have forecast 17% earnings growth, which will help keep the stock moving the right direction.

MA Daily Chart

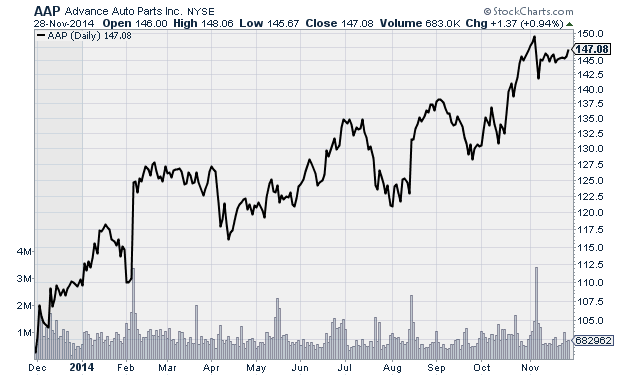

Advance Auto Parts (AAP)

The auto industry enjoyed another strong year in 2014, and analysts expect an even better year in 2015. The rise in new car sales will definitely pressure auto parts retailers, as do-it-yourself car owners will find less need to repair their vehicles, but I remain bullish on the sector. The average age of cars on the roads is still at a record high, at 11.4 years, so there is still going to be plenty of demand for auto parts to keep these vehicles road-worthy. While rising auto sales will impact parts sales, Advance Auto Parts (AAP) has done a good job of ensuring it maintains its piece of the pie. The company acquired General Parts International Inc. in January, which helped increase the its market share in North America and strengthened its position in both existing and new product lines. As a result, the company enjoyed 17% earnings growth in the third-quarter, with same-store sales up 1.5%. Total sales were up a remarkable 51%. Next year the company is forecast to grow earnings by 13%, which will keep strength under the stock.

AAP Daily Chart

Kellogg (K)

Breakfast food maker Kellogg (K) is a solid company in any market, and next year stands to be another good year for the stock. Rising consumer confidence means that shoppers are more likely to buy brand-name merchandise, and Kellogg has some of the more popular brands in the food sector. It's stable of brands include JIF, Fruit Loops, Rice Krispies, Eggo, and of course Kellogg's. The company is only expected to grow earnings by 4% next year, but given the stock's current valuation, there is still plenty of upside potential. The stock's P/E is currently just 13.7, which is well below the industry average of 19.6. A further reason to hold K stock is that the company is a solid dividend play. It currently has a dividend yield of 2.96%, and has increased its dividend each of the last nine years. It has a payout ratio of 50.3%, which is slightly higher than I like to see, but not so high as to prevent another dividend increase in 2015. All signs point to another up year for Kellogg stock.

K Daily Chart

Courtesy of MarketIntelligenceCenter.com