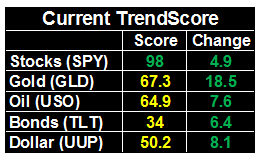

Weekly Market Outlook - Running on Fumes (But Still Running)

The Trump train continues to chug along, with last week's forward progress inspired by renewed chatter of impending tax cuts. The timeframe and details remain unclear, but the mere promise of tax relief was enough to inspire a strong finish to the week. The S&P 500's close of 2316.1 was 0.8% higher than the prior week's closing value.

The Trump train continues to chug along, with last week's forward progress inspired by renewed chatter of impending tax cuts. The timeframe and details remain unclear, but the mere promise of tax relief was enough to inspire a strong finish to the week. The S&P 500's close of 2316.1 was 0.8% higher than the prior week's closing value.

There's a flipside, of course. One of them is the distinct possibility that it could be months before any tax overhaul is put in place. Another is the reality that corporate earnings growth still isn't that impressive yet, even if the President is pro-business. That potential 'in the meantime' letdown makes this relentless rally vulnerable. Never even mind the fact that February is generally a weak one for the market.

We'll hash it all out below, as always, but first, let's wade through last week's and this week's economic news.

Economic Data

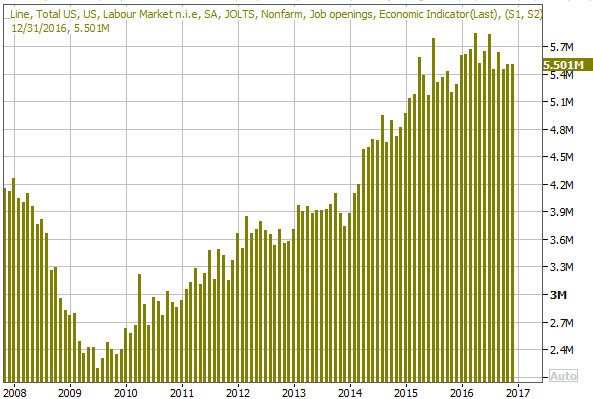

Last week was one of the most anemic weeks we'll see all year, in terms of economic information . Even the most interesting item we had on the dancecard -- JOLTS (job-opening and labor turnover survey) -- is barely worth examining. But, because it matters to some degree, we'll point out that January's JOLTS figure fell from 5.505 million to 5.501 million. That reading extends a modest lull, though is still a rather strong reading in the grand scheme of things.

JOLTS (Job-opening and Labor Turnover Survey) Charts

Source: Thomson Reuters

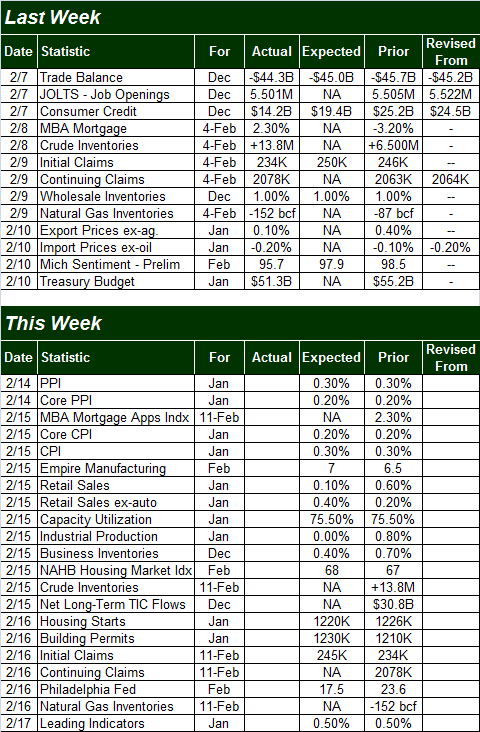

Everything else is on the grid.

Economic Calendar

Source: Briefing.com

This week's busy schedule more than makes up for last week's lull.

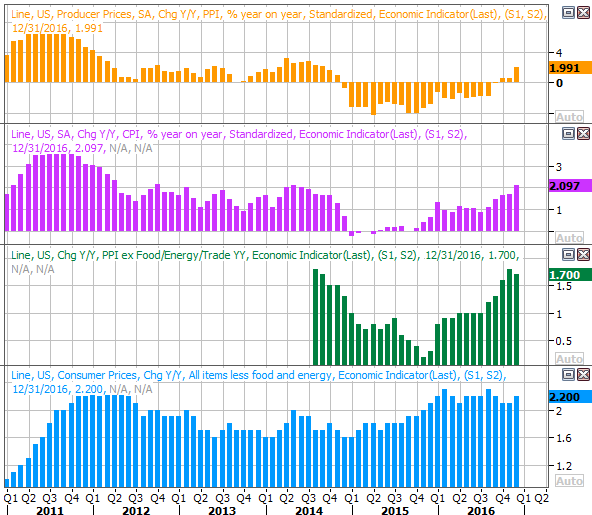

The party starts on Tuesday, with last month's producer price inflation data, and is followed up on Tuesday with January's consumer inflation data. You may recall inflation has been creeping higher for a while, but really took off last month. Economists think we'll see similarly-strong price increases for January.

Producer and Consumer Inflation (Annualized) Charts

Source: Thomson Reuters

The Federal Reserve held off on a rate hike last month, despite voicing its aim to put two or three in place this year. Another strong inflation reading this time around, and the FOMC may be forced to act the next chance it gets in the middle of March.

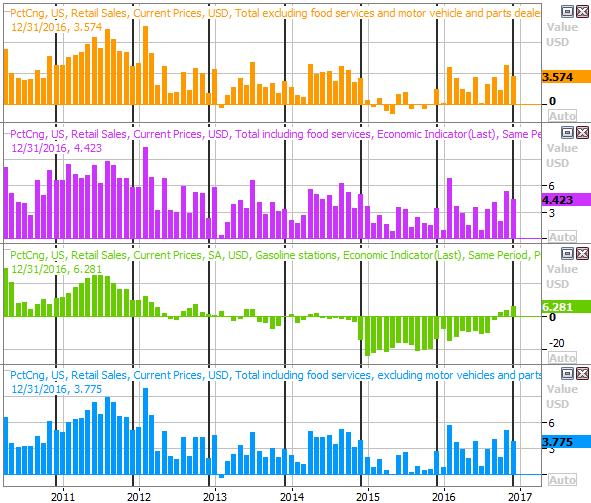

Also on Wednesday we'll hear February's retail sales figures. Though auto sales are expected to drag the overall growth rate down, taking automobiles out of the equation, economists expect 0.4%. That figure will be much higher on an annualized basis (which is a far more meaningful measure). Consumers have been doing their part to get and keep the economy moving.

Retail Sales Growth (Annualized) Charts

Source: Thomson Reuters

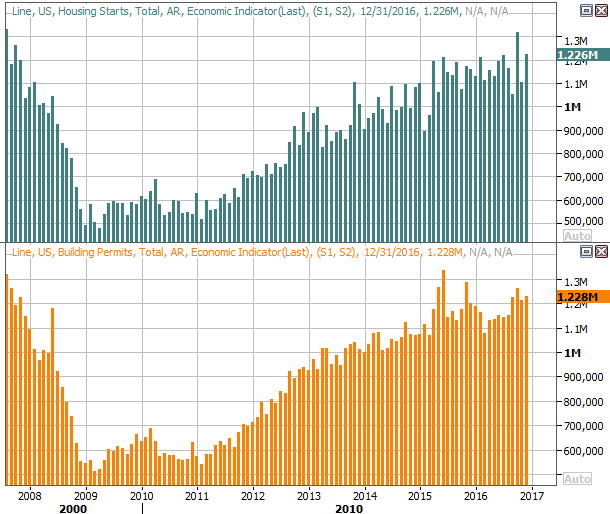

Finally, on Thursday look for last month's housing starts and building permits data. They've both been trending higher for some time now, but a close look at the chart of both below loosely implies the growth of both could be slowing. This report has some potential to move the market, either way.

Housing Starts and Building Permits Charts

Source: Thomson Reuters

Index Analysis

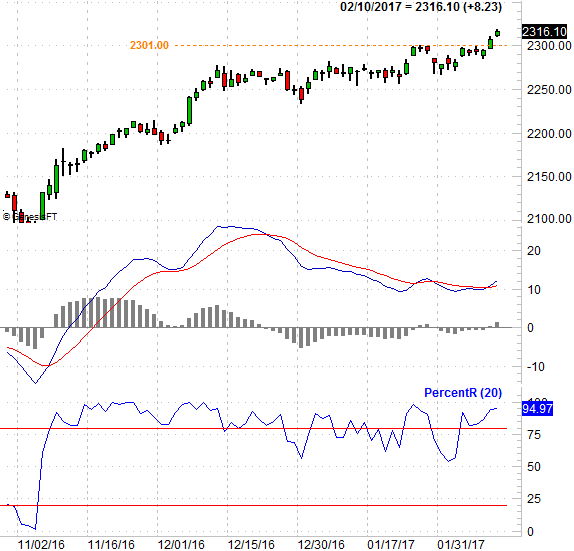

With just a quick look, the market looks full steam ahead. Most of the indices (and all of the large cap indices) have punched through their key technical ceilings and hit new record highs on Friday. That includes the S&P 500, which hit a new high of 2319.23 on the last trading day of last week. That advance also pushed the index above its upper 20-day Bollinger band. The VIX is also right on the cusp of a break below a key floor at 10.20, where its lower Bollinger band is currently found.

S&P 500 Daily Chart

Chart created with TradeStation

Indeed, the most recent leg of the rally has induced a confirmed PercentR buy signal, and given as a bullish MACD cross as well.

S&P 500 Daily Chart, With PercentR and MACD

Chart created with TradeStation

By all accounts, things are bullish -- even the BigTrends TrendScore for stocks is at a very healthy 98.0. Yet, traders would be wise to be wary here.

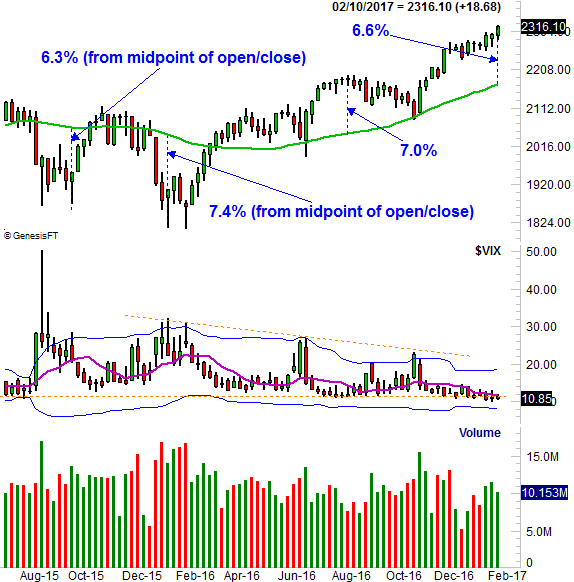

It's not a very conventional way of looking at things, nor is it any less flawed than other methodologies. But, when we zoom out to a weekly chart of the S&P 500 we can get a very clear -- and quantifiable -- view of just how far the S&P 500 has traveled just since November.

Assuming the 200-day moving average line is a baseline of sorts, and assuming the index can only travel so far away from it before being reeled in (a function of time and speed), the S&P 500 is roughly at its maximum sustainable distance from its 200-day average line. It's now right at 7.0% above its 200-day moving average line (green), which by the way was how far above that line the index got in August before being pulled back to the 200-day line.

S&P 500 Weekly Chart

Chart created with TradeStation

The reel-in works both directions too, reining in a couple of selloffs in 2015.

It's also on the weekly chart we can see another flaw with this rally... it lacks volume. Not only is the buying volume not growing as it should be if the rally is to continue, the effort is losing volume on the way up. This rally is not especially well supported. That, coupled with unusually high complacency, leaves this market more vulnerable than it might seem on the surface.

The line in the sand for the S&P 500 is 2260, give or take. That's where the 50-day moving average line and the lower Bollinger band currently lie. It's also where the S&P 500 found a floor several times in January. And pullback that doesn't break that support can't be called more than just a little volatility.

Still, it's difficult to imagine tacking on a lot more gains here. As of the latest tally, the S&P 500 is valued at a trailing P/E of 21.3. The forward-looking estimates suggest the index is trading at a projected P/E of 17.7. That's still unusually high though, and the S&P 500's constituents rarely actually meet their lofty targets.

We'll take a closer look at Q4 earnings results next week. They're relatively better, but a few red flags are waving.