Inside The Biotech Selloff

Another Bad Day in Biotech Stocks, Pace of Selling Accelerates

by: Adam Feuerstein

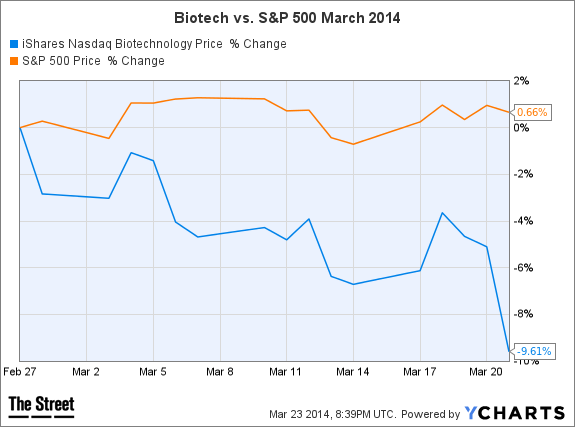

The Nasdaq Biotechnology Index (NBI) (IBB) is down 20 points, or around 8%, in the past 2 trading days. Let's take a look at where things stand.

The Nasdaq Biotechnology Index ended February up more than 16%, but remember, stocks were very weak on the last day of the month, leading to some questions about how the Biotech sector (XBI) would perform in March. Not so great, it turns out...

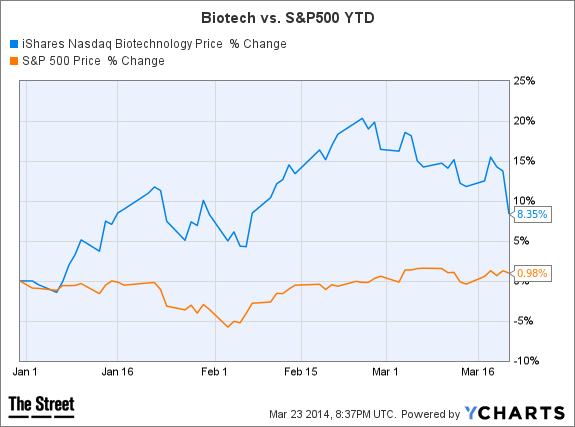

The biotech sector is still outperforming the broader market for the year, but the February gains are gone.

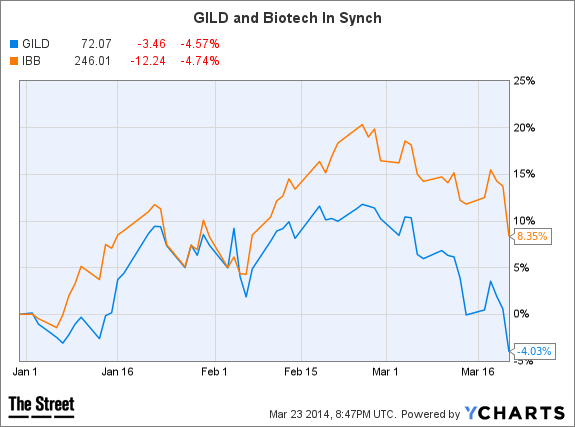

I thought this next chart was really interesting. It overlays the performance of Gilead Sciences (GILD) and the IBB: Almost perfect synchronization. This chart shows you how pushback against the $1,000-per-day price of Gilead's hepatitis C pill Sovaldi can spread fear across the entire biotech sector. [I checked the IBB against the other big-cap biotech stocks Celgene(CELG), Amgen (AMGN), Biogen Idec (BIIB) and Alexion Pharma (ALXN) but didn't see the same pattern.]

Where does the sector go from here? Do investors buy the dip or will we see more weakness? Obviously, I don't have an answer, no one does. But for those downplaying the significance of the Gilead-Sovaldi price controversy, I'd say remember that biotech stocks, like most sectors, trade not only on fundamentals but on sentiment and the confidence in future earnings potential.

Those arguing against a biotech bubble say price-to-earnings (P/E) ratios for biotech stocks are nowhere near historical highs. True, but if investors -- particularly generalists investors -- worry about the sustainability of drug pricing, then confidence in the future "E" of the P/E ratio falls. We call that "P/E compression" and it's not a good thing for stocks.

ISI Group drug analyst Mark Schoenebaum took to Twitter this weekend to make a similar point:

"I've remarked that drug pricing concerns could trigger end of #biotech run. That's why responsible observers need to take Fri seriously. On a micro level Fri's Waxman letter will lead to nothing. Question is what does it do to (generalist) sentiment/confidence."

J.P. Morgan analyst Geoff Meacham doesn't believe in the biotech bubble and is holding a conference call for investor clients Monday morning at 10:15 am EDT to offer reasons why the sector still has room to grow:

Meacham:

"We believe that the sector remains broadly attractive from a valuation/pipeline/growth perspective, particularly in large cap. Notably, the average 3-year revenue and EPS CAGR for the top 10 biotechs (market cap) is 4.5X and 3X that of the S&P500, yet the P/E/G on 2015-2016 forecasts for biotech is ~0.7 versus the S&P at ~1.4. Regarding the industry pipeline, product cycles are very long in biotech (>10 years) and dozens of major launches are occurring or are about to occur (Sovaldi, Tecfidera, Imbruvica, Pomalyst, Otezla, Eylea, Kalydeco, Xtandi, Linzess asfotase alfa, Vimizim, idelalisib, evolocumab, alirocumab, etc.). In addition, we estimate that at least 50+ compounds/label expansions that have some level of de-risking are largely unaccounted for in Street models. Admittedly, companies with earlier-stage pipelines that haven't been fully de-risked are being awarded a higher probability of clinical success, but drug development has become more efficient, particularly for orphan drugs. The recent concern on pricing for Gilead's Sovaldi has caused much anxiety; at the end of the day, the benefit/risk and cost/benefit profile remains quite striking and we doubt that the recent Congressional inquiry would lead to an "innovation tax" (i.e., forced material discounts)."

Courtesy of TheStreet.com