Weekly Market Outlook - The Trend Is Your Friend

Despite the tepid start to the trading week last week, the bullish finished strong, taking all the major indices above some major technical resistance lines.

Granted, Friday's bullish move was more than a little overheated, with the opening gaps leaving the market vulnerable to a pullback that may well serve to start a corrective move. But, it's interesting that the market was able to muster that much bullish interest on what was (frankly) less than truly bullish prompt.

We'll talk about the risks and rewards of the current situation below, right after a quick wrap-up of last week's and this week's major economic numbers.

Economic Data

It wasn't an especially busy week last week in terms of economic news, but it was a significant week for real estate data.

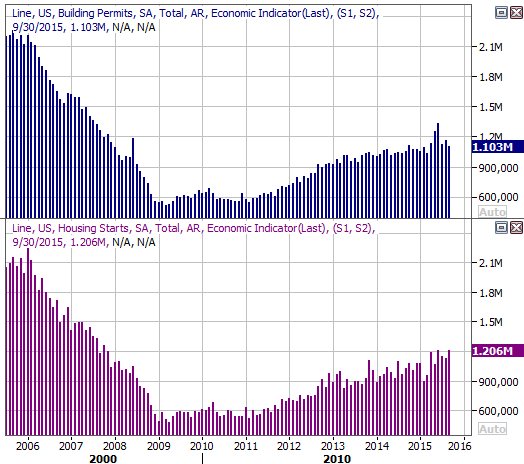

The flurry of housing news started on Monday with the NAHB Housing Market Index, which advanced to 64 from September's score of 61. But, the party got started in earnest on Tuesday with September's housing starts and building permits. Though permits fell from a pace of 1.1161 million units to 1.103 million, starts ramped up from August's pace of 1.132 million to 1.206 million... almost a multi-year record high. Regardless, both pieces of data continue to climb in a healthy manner.

Housing Starts and Building Permits Chart

Source: Thomas Reuters

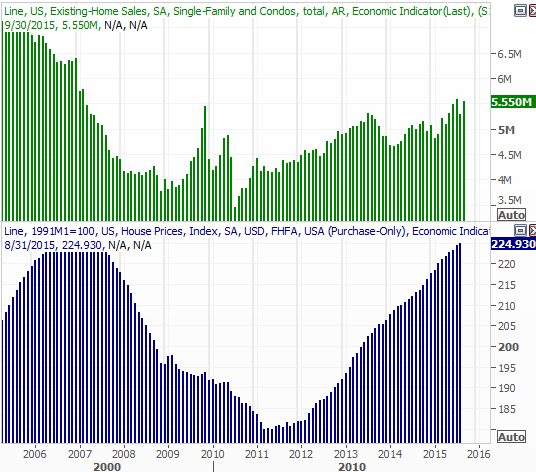

On Thursday we got updated FHFA Housing Price Index and existing home sales figures, both of which also pointed to an increasingly strong real estate market. The FHFA Housing Price Index said home prices were up 0.3% for the month, and up 5.5% compared to August-2014's numbers. And, existing home sales were cranked up to an annual pace of 5.5 million houses... the second highest pace since 2007 (when the number was falling).

Those two uptrends also say the housing market is solid.

Existing Home Sales and FHFA Housing Price Index Chart

Source: Thomas Reuters

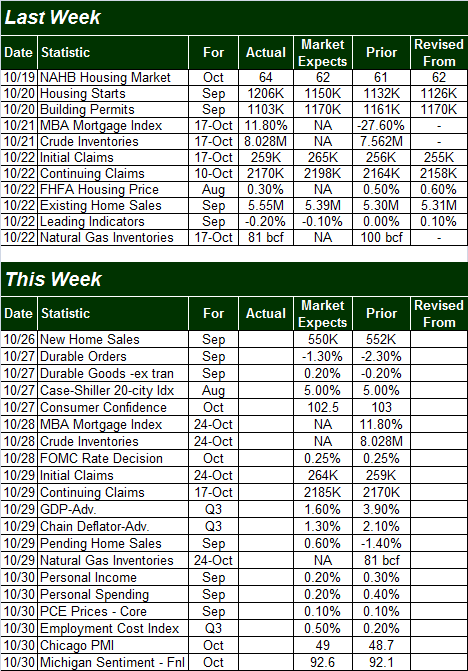

Everything else is on the following grid:

Economic Calendar

Source: Briefing.com

This week is obviously going to be quite a bit busier, kicking off with new home sales on Monday. If last week's real estate data is any indication (and it is), that number should at least be respectable if not encouraging.

The highlight of the week, though, is going to be Wednesday's word from the Federal Reserve. Though it's not an official rate-change decision meeting, the possibility is always on the table in case of emergencies. But, given the wave of numbers that imply economic weakening rather than strengthening - like the fact that ECB President Mario Draghi is talking about stimulus - we don't have much reason to worry this is the month we'll see a rate hike in the U.S.

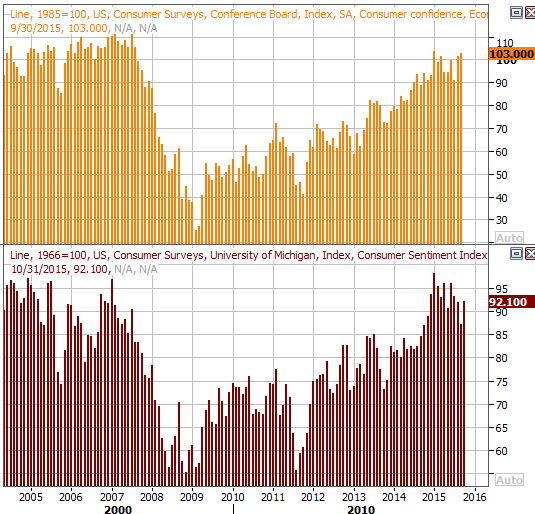

Though it's a bit off the radar, this week will also be a big one for consumer sentiment. On Tuesday we'll hear the Conference Board's consumer confidence level for October, and on Friday we'll get the final reading of this month's Michigan Sentiment Index. Though choppy, both are in broad uptrends. It may be worth keeping a close eye on the Michigan Sentiment Index, however, as it's been acting a little toppy, toying with the development of a downtrend.

Consumer Sentiment Chart

Source: Thomas Reuters

Stock Market Index Analysis

Like it or not, the market broke out last week, and cleared some key technical hurdles in the process. Even more than that, it confirmed the breakout effort via a handful of indicators. Though hardly an ideal rally effort (and one that should be viewed with extreme cautions), as they say, it is what it is.

For the S&P 500 (SPX) (SPY), "what it is" is a thrust above the 200-day moving average line (green) thanks to Friday's gain. That may be the grandmother of all technical bullish clues. More than that, however, the bullishness seen on Thursday and Friday was on above average volume, but not dangerously high volume (volume surges often occur at market tops). Take a look.

S&P 500 & VIX Daily Chart

Chart created with TradeStation

Last week we talked about the fact that we had yet to get a Percent R confirmation of bullishness. In the meantime, we DID get it. As you can also see highlighted in the chart, the Percent R line did pull back last week, but didn't fall back under the 80 threshold before moving higher again at the same time the S&P 500 itself made a new high. That's a bullish confirmation.

The daily chart of the NASDAQ Composite (COMP) looks similar, though in some ways, not quite as healthy. For instance, the composite left a rather big gap behind on Friday, and it's rather clear the NASDAQ's upper Bollinger band is doing its best to act as a ceiling. Bollinger bands have prompted reversals more often than not this year, and while it's possible this bullish thrust could be different than most of the recent ones and instead gently push the upper Bollinger band upward rather than pull back from it, we have no evidence this is going to happen yet.

NASDAQ Composite & VXN Daily Chart

Chart created with TradeStation

We also don't yet have a bullish Percent R confirmation for the NASDAQ Composite, though we're in a good position to make one. And for what it's worth, the BigTrends TrendScore for stocks as of Friday's close was a bullish 88.8 (out of 100).

The one thing to watch that may be more telling than the market indices themselves this week are the volatility indices... the Nasdaq Volatility Index (VXN) and CBOE Volatility Index (VIX) (VXX). Both are right above key support levels and though each is on a course to move below those floors this week, traders should watch out for potential support at those lines... 13.7 for the VXN and 12.2 for the VIX. Unexpected support there could lead to a surprising reversal for stocks. Until then though, the trend is your friend.

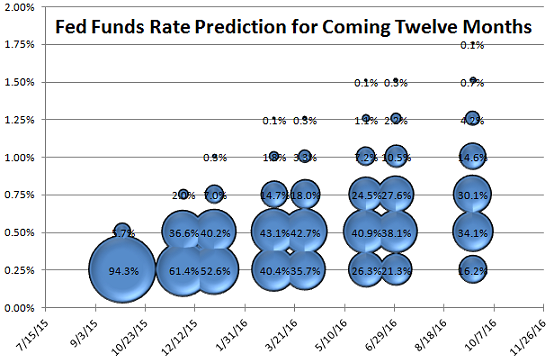

Fed Funds Rate Outlook

It's been a while since we updated the Fed Funds rate prediction chart (based on the way Fed Funds futures are priced, and their open interest). But, with changes to the economic landscape forcing the Federal Reserve to rethink the need for such a maneuver, a refreshed look is merited.

Long story made short, the first likely rate hike in years has been pushed back to March of next year, and even then it's a "just barely" scenario; traders are saying there's a 43.1% chance the Fed Funds rate will be at 0.5% then, with a 40.4% chance it'll still be at 0.25% at that time. The odds for a 0.5% rate don't reaching convicting levels until June of next year, where they should stay at least through September... with a small outside possibility of reaching 0.75% by September.

Fed Funds Outlook and Odds Chart

Source: CME Group

Although they're just odds based on Fed Funds futures activity and pricing, traders are collectively right more often than they may believe is possible. [Try a web search for "jelly bean, wisdom of crowds" to understand why they're so good as a group.] This includes the prediction of future interest rates.

Trade Well,

Price Headley

BigTrends.com

1-800-244-8736