Buybacks May Be A Large Portion Of Current Market Buying Pressure

With Everyone Selling Stocks, Who Is Buying? Goldman Explains

by ZeroHedge

There has been some confusion in recent weeks about one unexplained aspect of the rising market: just who is buying?

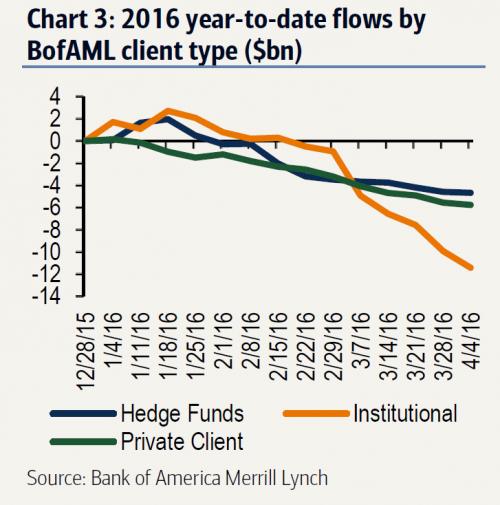

The reason for the confusion is not only the previously documented buyer strike by the smart money (hedge funds, institutions and private clients), which as we reported a few days have sold stocks for 11 consecutive weeks.

Then last night, citing the latest EPFR data, BofA reported that retail equity investors are now also "risk-off" following $6.2 billion in equity outflows from all regions.

So retail is selling, insiders are selling… who is buying?

Here is the answer courtesy of Goldman's David Kostin:

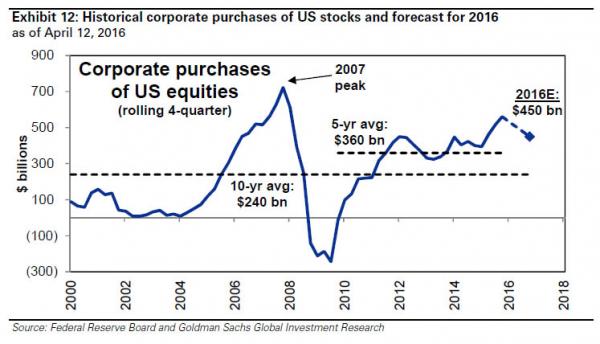

Corporations purchased $561 billion of US equities during 2015, 40% higher than during 2014 ($401 billion) and the second highest level since at least 1952 ($721 billion in 2007). Managements remained committed to share repurchases (net of issuance) last year amidst modest US GDP growth of 2.4% and extended valuations. Outside of the Great Recession, corporates have been the primary source of US equity demand.

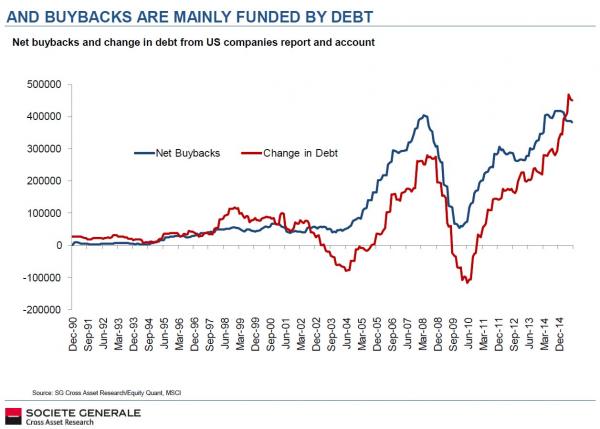

We already know that in a world of declining cash flows, the primary source of funds to facilitated this behavior was debt issuance. In fact, as SocGen showed in a stunning chart last year, the only reason for the increase of net debt in the 21st century has been to fund buybacks.

That explains who bought. But what about who is buying and who will keep on buying? The answer: even more corporate buybacks.

Buybacks will remain the key source of equity inflow in 2016

We expect corporations will purchase $450 billion of US equities in 2016 and will remain the largest source of US equity demand. With the US economy expected to grow at a modest 2% pace and cash balances at high levels, firms are likely to continue to pursue buybacks as a means of generating shareholder value. We forecast S&P 500 EPS will rise by 9% to $110 this year from $100 in 2015 (see US Equity Views, March 14, 2016), which should also benefit allocation to buybacks.

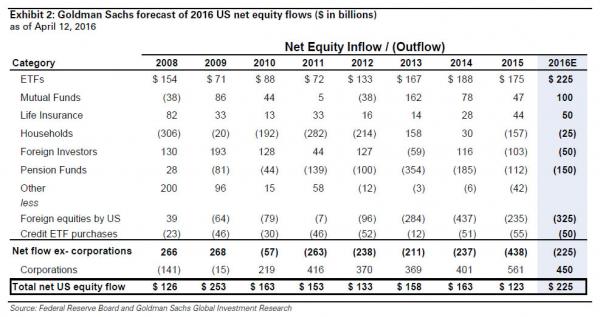

This means that without corporate buybacks, suddenly the S&P has a gaping $225 billion shortfall in net equity flow to fill. Which is also why it is so critical for the Fed to make sure that there are no disruptions to the bond market: should the issuance train slow down, and if corporations can't raise the much needed half a trillion in debt proceeds which will be used to buyback stock, a big problem emerges.

It also explains why the ECB last month scrambled to backstop investment grade corporate bond issuance for the first time: in effect Draghi gave his blessing to Europe's companies to raise debt and to use every last EUR of proceeds to buyback their own stock.

We expect something similar to be unveiled in the US soon.

Courtesy of philstockworld.com